Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOnline Linear Programming with Replenishment

Jan 21, 2026We study an online linear programming (OLP) model in which inventory is not provided upfront but instead arrives gradually through an exogenous stochastic replenishment process. This replenishment-based formulation captures operational settings, such as e-commerce fulfillment, perishable supply chains, and renewable-powered systems, where resources are accumulated gradually and initial inventories are small or zero. The introduction of dispersed, uncertain replenishment fundamentally alters the structure of classical OLPs, creating persistent stockout risk and eliminating advance knowledge of the total budget. We develop new algorithms and regret analyses for three major distributional regimes studied in the OLP literature: bounded distributions, finite-support distributions, and continuous-support distributions with a non-degeneracy condition. For bounded distributions, we design an algorithm that achieves $\widetilde{\mathcal{O}}(\sqrt{T})$ regret. For finite-support distributions with a non-degenerate induced LP, we obtain $\mathcal{O}(\log T)$ regret, and we establish an $Ω(\sqrt{T})$ lower bound for degenerate instances, demonstrating a sharp separation from the classical setting where $\mathcal{O}(1)$ regret is achievable. For continuous-support, non-degenerate distributions, we develop a two-stage accumulate-then-convert algorithm that achieves $\mathcal{O}(\log^2 T)$ regret, comparable to the $\mathcal{O}(\log T)$ regret in classical OLPs. Together, these results provide a near-complete characterization of the optimal regret achievable in OLP with replenishment. Finally, we empirically evaluate our algorithms and demonstrate their advantages over natural adaptations of classical OLP methods in the replenishment setting.

A Survey of Scientific Large Language Models: From Data Foundations to Agent Frontiers

Aug 28, 2025

Scientific Large Language Models (Sci-LLMs) are transforming how knowledge is represented, integrated, and applied in scientific research, yet their progress is shaped by the complex nature of scientific data. This survey presents a comprehensive, data-centric synthesis that reframes the development of Sci-LLMs as a co-evolution between models and their underlying data substrate. We formulate a unified taxonomy of scientific data and a hierarchical model of scientific knowledge, emphasizing the multimodal, cross-scale, and domain-specific challenges that differentiate scientific corpora from general natural language processing datasets. We systematically review recent Sci-LLMs, from general-purpose foundations to specialized models across diverse scientific disciplines, alongside an extensive analysis of over 270 pre-/post-training datasets, showing why Sci-LLMs pose distinct demands -- heterogeneous, multi-scale, uncertainty-laden corpora that require representations preserving domain invariance and enabling cross-modal reasoning. On evaluation, we examine over 190 benchmark datasets and trace a shift from static exams toward process- and discovery-oriented assessments with advanced evaluation protocols. These data-centric analyses highlight persistent issues in scientific data development and discuss emerging solutions involving semi-automated annotation pipelines and expert validation. Finally, we outline a paradigm shift toward closed-loop systems where autonomous agents based on Sci-LLMs actively experiment, validate, and contribute to a living, evolving knowledge base. Collectively, this work provides a roadmap for building trustworthy, continually evolving artificial intelligence (AI) systems that function as a true partner in accelerating scientific discovery.

SeedBench: A Multi-task Benchmark for Evaluating Large Language Models in Seed Science

May 19, 2025Seed science is essential for modern agriculture, directly influencing crop yields and global food security. However, challenges such as interdisciplinary complexity and high costs with limited returns hinder progress, leading to a shortage of experts and insufficient technological support. While large language models (LLMs) have shown promise across various fields, their application in seed science remains limited due to the scarcity of digital resources, complex gene-trait relationships, and the lack of standardized benchmarks. To address this gap, we introduce SeedBench -- the first multi-task benchmark specifically designed for seed science. Developed in collaboration with domain experts, SeedBench focuses on seed breeding and simulates key aspects of modern breeding processes. We conduct a comprehensive evaluation of 26 leading LLMs, encompassing proprietary, open-source, and domain-specific fine-tuned models. Our findings not only highlight the substantial gaps between the power of LLMs and the real-world seed science problems, but also make a foundational step for research on LLMs for seed design.

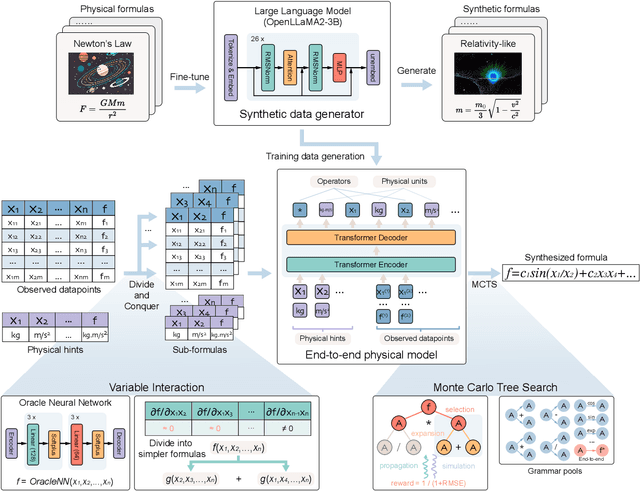

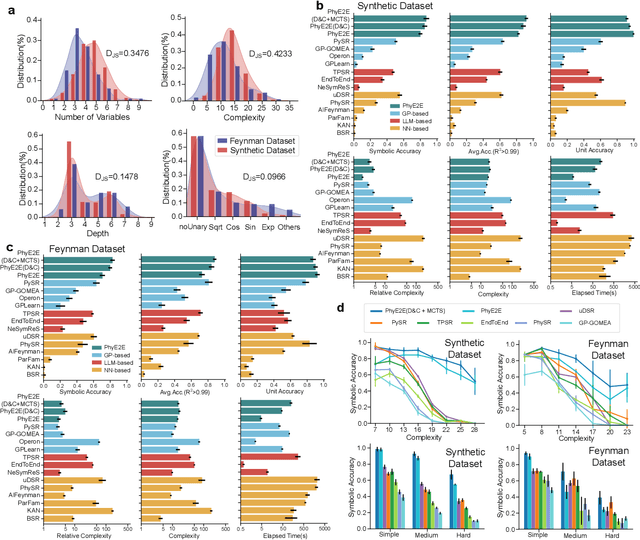

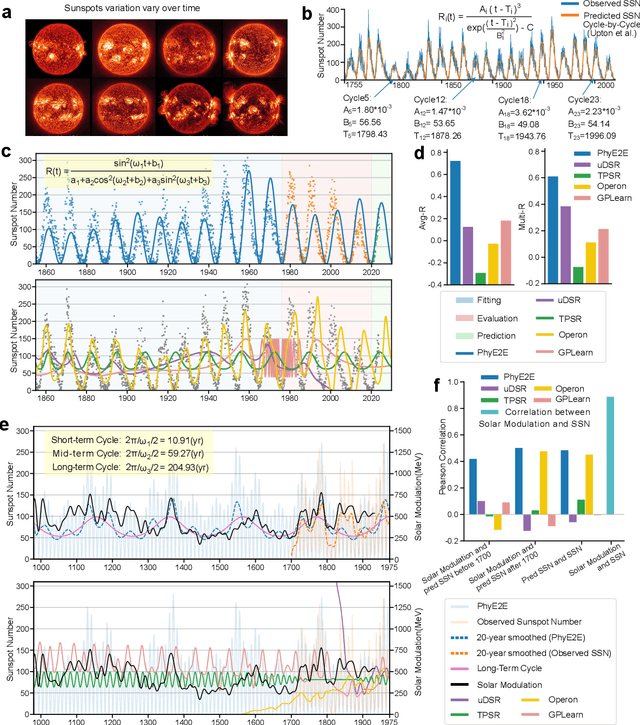

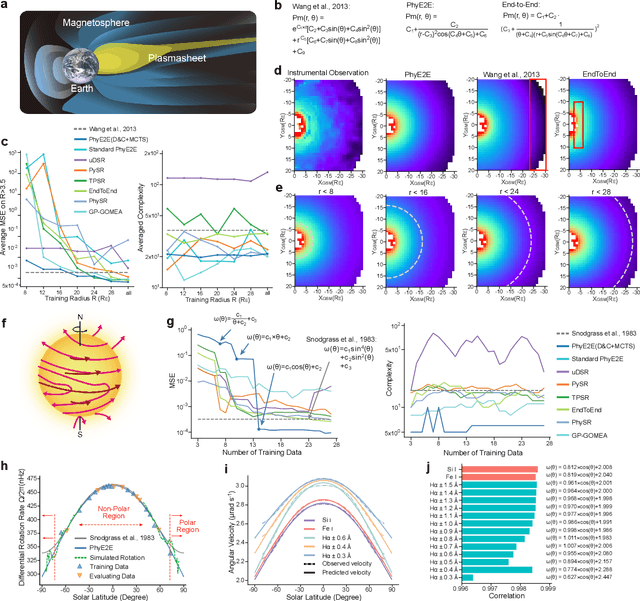

A Neural Symbolic Model for Space Physics

Mar 11, 2025

In this study, we unveil a new AI model, termed PhyE2E, to discover physical formulas through symbolic regression. PhyE2E simplifies symbolic regression by decomposing it into sub-problems using the second-order derivatives of an oracle neural network, and employs a transformer model to translate data into symbolic formulas in an end-to-end manner. The resulting formulas are refined through Monte-Carlo Tree Search and Genetic Programming. We leverage a large language model to synthesize extensive symbolic expressions resembling real physics, and train the model to recover these formulas directly from data. A comprehensive evaluation reveals that PhyE2E outperforms existing state-of-the-art approaches, delivering superior symbolic accuracy, precision in data fitting, and consistency in physical units. We deployed PhyE2E to five applications in space physics, including the prediction of sunspot numbers, solar rotational angular velocity, emission line contribution functions, near-Earth plasma pressure, and lunar-tide plasma signals. The physical formulas generated by AI demonstrate a high degree of accuracy in fitting the experimental data from satellites and astronomical telescopes. We have successfully upgraded the formula proposed by NASA in 1993 regarding solar activity, and for the first time, provided the explanations for the long cycle of solar activity in an explicit form. We also found that the decay of near-Earth plasma pressure is proportional to r^2 to Earth, where subsequent mathematical derivations are consistent with satellite data from another independent study. Moreover, we found physical formulas that can describe the relationships between emission lines in the extreme ultraviolet spectrum of the Sun, temperatures, electron densities, and magnetic fields. The formula obtained is consistent with the properties that physicists had previously hypothesized it should possess.

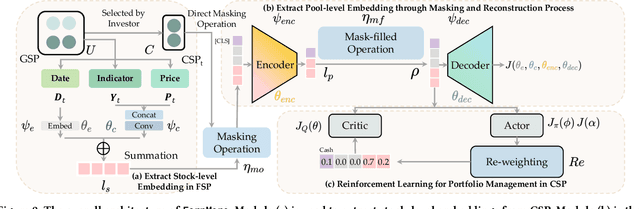

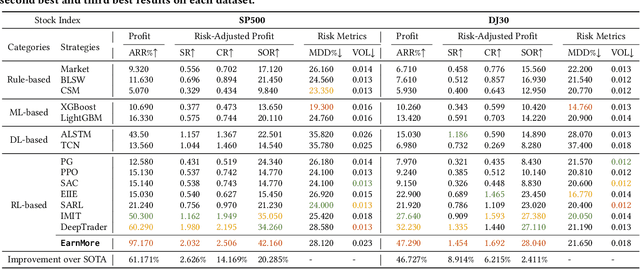

Reinforcement Learning with Maskable Stock Representation for Portfolio Management in Customizable Stock Pools

Nov 21, 2023

Portfolio management (PM) is a fundamental financial trading task, which explores the optimal periodical reallocation of capitals into different stocks to pursue long-term profits. Reinforcement learning (RL) has recently shown its potential to train profitable agents for PM through interacting with financial markets. However, existing work mostly focuses on fixed stock pools, which is inconsistent with investors' practical demand. Specifically, the target stock pool of different investors varies dramatically due to their discrepancy on market states and individual investors may temporally adjust stocks they desire to trade (e.g., adding one popular stocks), which lead to customizable stock pools (CSPs). Existing RL methods require to retrain RL agents even with a tiny change of the stock pool, which leads to high computational cost and unstable performance. To tackle this challenge, we propose EarnMore, a rEinforcement leARNing framework with Maskable stOck REpresentation to handle PM with CSPs through one-shot training in a global stock pool (GSP). Specifically, we first introduce a mechanism to mask out the representation of the stocks outside the target pool. Second, we learn meaningful stock representations through a self-supervised masking and reconstruction process. Third, a re-weighting mechanism is designed to make the portfolio concentrate on favorable stocks and neglect the stocks outside the target pool. Through extensive experiments on 8 subset stock pools of the US stock market, we demonstrate that EarnMore significantly outperforms 14 state-of-the-art baselines in terms of 6 popular financial metrics with over 40% improvement on profit.