Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEfficiently Generating Correlated Sample Paths from Multi-step Time Series Foundation Models

Oct 02, 2025

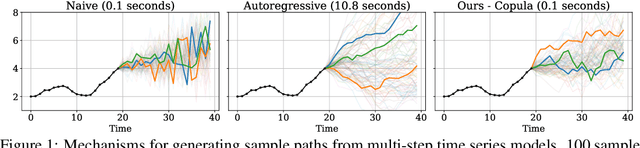

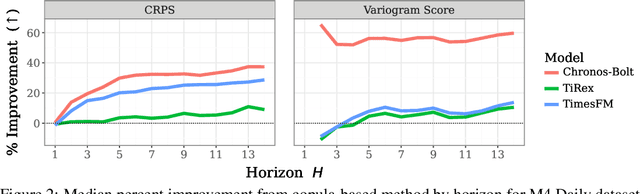

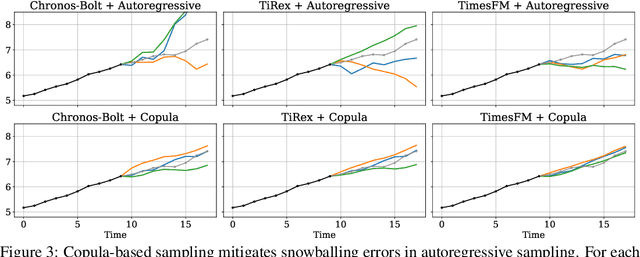

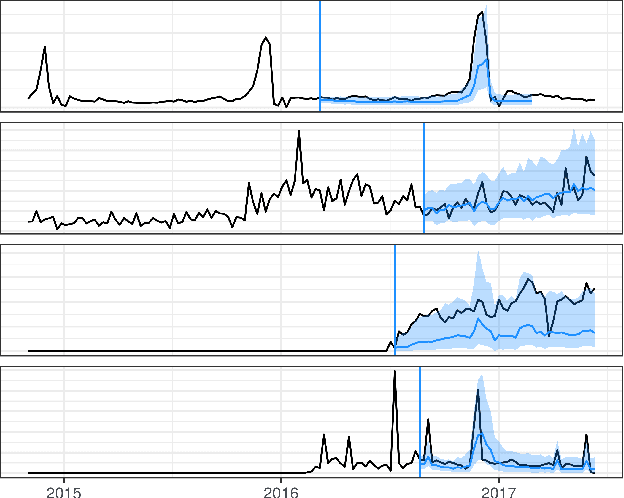

Many time series applications require access to multi-step forecast trajectories in the form of sample paths. Recently, time series foundation models have leveraged multi-step lookahead predictions to improve the quality and efficiency of multi-step forecasts. However, these models only predict independent marginal distributions for each time step, rather than a full joint predictive distribution. To generate forecast sample paths with realistic correlation structures, one typically resorts to autoregressive sampling, which can be extremely expensive. In this paper, we present a copula-based approach to efficiently generate accurate, correlated sample paths from existing multi-step time series foundation models in one forward pass. Our copula-based approach generates correlated sample paths orders of magnitude faster than autoregressive sampling, and it yields improved sample path quality by mitigating the snowballing error phenomenon.

Using Pre-trained LLMs for Multivariate Time Series Forecasting

Jan 10, 2025

Pre-trained Large Language Models (LLMs) encapsulate large amounts of knowledge and take enormous amounts of compute to train. We make use of this resource, together with the observation that LLMs are able to transfer knowledge and performance from one domain or even modality to another seemingly-unrelated area, to help with multivariate demand time series forecasting. Attention in transformer-based methods requires something worth attending to -- more than just samples of a time-series. We explore different methods to map multivariate input time series into the LLM token embedding space. In particular, our novel multivariate patching strategy to embed time series features into decoder-only pre-trained Transformers produces results competitive with state-of-the-art time series forecasting models. We also use recently-developed weight-based diagnostics to validate our findings.

Chronos: Learning the Language of Time Series

Mar 12, 2024We introduce Chronos, a simple yet effective framework for pretrained probabilistic time series models. Chronos tokenizes time series values using scaling and quantization into a fixed vocabulary and trains existing transformer-based language model architectures on these tokenized time series via the cross-entropy loss. We pretrained Chronos models based on the T5 family (ranging from 20M to 710M parameters) on a large collection of publicly available datasets, complemented by a synthetic dataset that we generated via Gaussian processes to improve generalization. In a comprehensive benchmark consisting of 42 datasets, and comprising both classical local models and deep learning methods, we show that Chronos models: (a) significantly outperform other methods on datasets that were part of the training corpus; and (b) have comparable and occasionally superior zero-shot performance on new datasets, relative to methods that were trained specifically on them. Our results demonstrate that Chronos models can leverage time series data from diverse domains to improve zero-shot accuracy on unseen forecasting tasks, positioning pretrained models as a viable tool to greatly simplify forecasting pipelines.

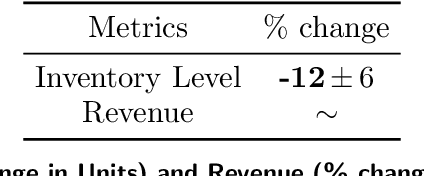

Learning an Inventory Control Policy with General Inventory Arrival Dynamics

Oct 26, 2023

In this paper we address the problem of learning and backtesting inventory control policies in the presence of general arrival dynamics -- which we term as a quantity-over-time arrivals model (QOT). We also allow for order quantities to be modified as a post-processing step to meet vendor constraints such as order minimum and batch size constraints -- a common practice in real supply chains. To the best of our knowledge this is the first work to handle either arbitrary arrival dynamics or an arbitrary downstream post-processing of order quantities. Building upon recent work (Madeka et al., 2022) we similarly formulate the periodic review inventory control problem as an exogenous decision process, where most of the state is outside the control of the agent. Madeka et al. (2022) show how to construct a simulator that replays historic data to solve this class of problem. In our case, we incorporate a deep generative model for the arrivals process as part of the history replay. By formulating the problem as an exogenous decision process, we can apply results from Madeka et al. (2022) to obtain a reduction to supervised learning. Finally, we show via simulation studies that this approach yields statistically significant improvements in profitability over production baselines. Using data from an ongoing real-world A/B test, we show that Gen-QOT generalizes well to off-policy data.

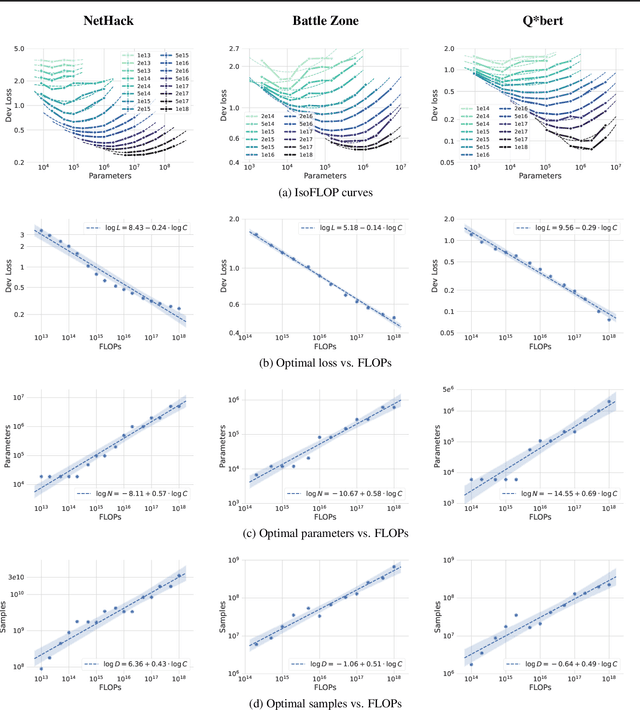

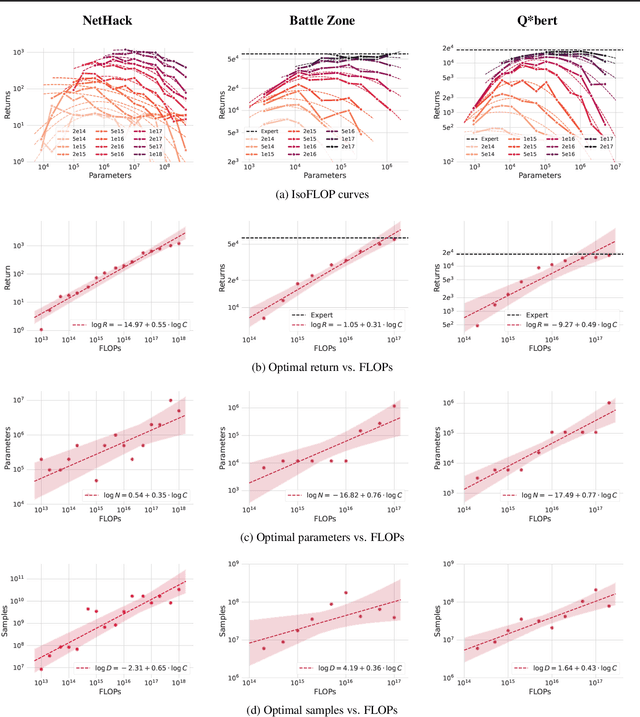

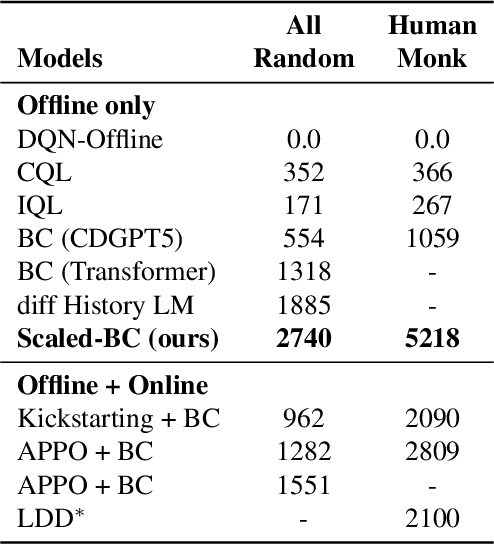

Scaling Laws for Imitation Learning in NetHack

Jul 18, 2023

Imitation Learning (IL) is one of the most widely used methods in machine learning. Yet, while powerful, many works find it is often not able to fully recover the underlying expert behavior. However, none of these works deeply investigate the role of scaling up the model and data size. Inspired by recent work in Natural Language Processing (NLP) where "scaling up" has resulted in increasingly more capable LLMs, we investigate whether carefully scaling up model and data size can bring similar improvements in the imitation learning setting. To demonstrate our findings, we focus on the game of NetHack, a challenging environment featuring procedural generation, stochasticity, long-term dependencies, and partial observability. We find IL loss and mean return scale smoothly with the compute budget and are strongly correlated, resulting in power laws for training compute-optimal IL agents with respect to model size and number of samples. We forecast and train several NetHack agents with IL and find they outperform prior state-of-the-art by at least 2x in all settings. Our work both demonstrates the scaling behavior of imitation learning in a challenging domain, as well as the viability of scaling up current approaches for increasingly capable agents in NetHack, a game that remains elusively hard for current AI systems.

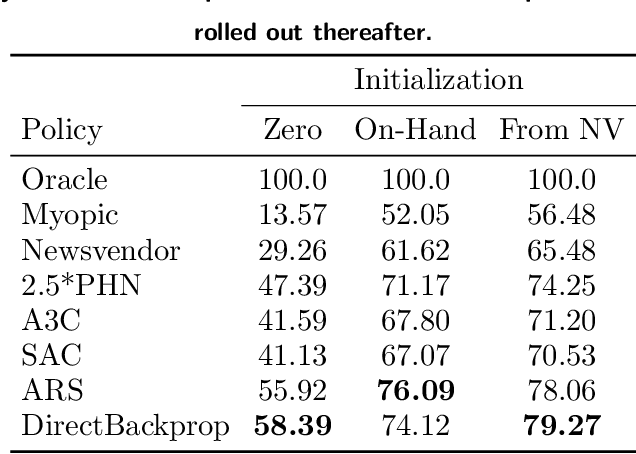

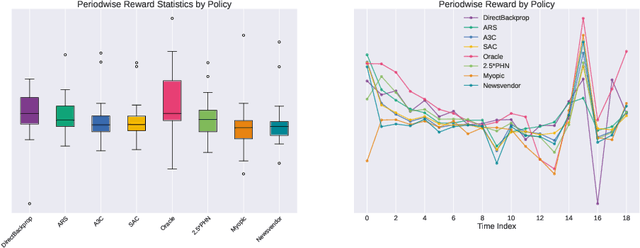

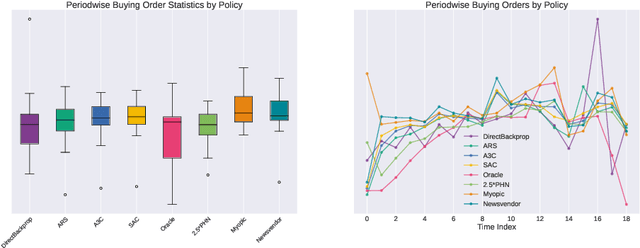

Deep Inventory Management

Oct 06, 2022

We present a Deep Reinforcement Learning approach to solving a periodic review inventory control system with stochastic vendor lead times, lost sales, correlated demand, and price matching. While this dynamic program has historically been considered intractable, we show that several policy learning approaches are competitive with or outperform classical baseline approaches. In order to train these algorithms, we develop novel techniques to convert historical data into a simulator. We also present a model-based reinforcement learning procedure (Direct Backprop) to solve the dynamic periodic review inventory control problem by constructing a differentiable simulator. Under a variety of metrics Direct Backprop outperforms model-free RL and newsvendor baselines, in both simulations and real-world deployments.

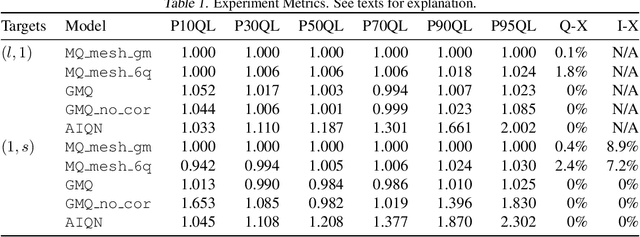

Deep Generative Quantile-Copula Models for Probabilistic Forecasting

Jul 24, 2019

We introduce a new category of multivariate conditional generative models and demonstrate its performance and versatility in probabilistic time series forecasting and simulation. Specifically, the output of quantile regression networks is expanded from a set of fixed quantiles to the whole Quantile Function by a univariate mapping from a latent uniform distribution to the target distribution. Then the multivariate case is solved by learning such quantile functions for each dimension's marginal distribution, followed by estimating a conditional Copula to associate these latent uniform random variables. The quantile functions and copula, together defining the joint predictive distribution, can be parameterized by a single implicit generative Deep Neural Network.

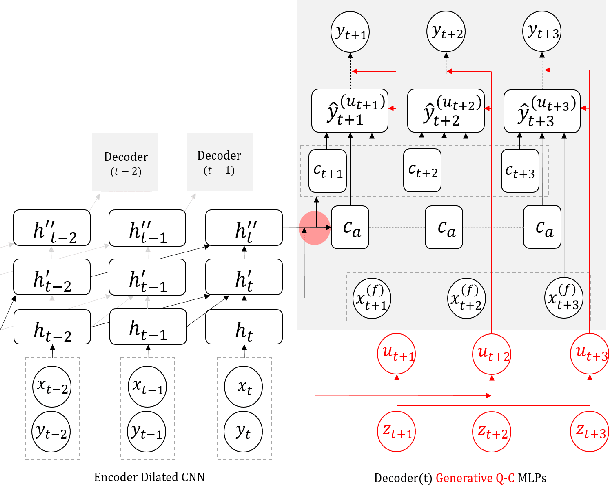

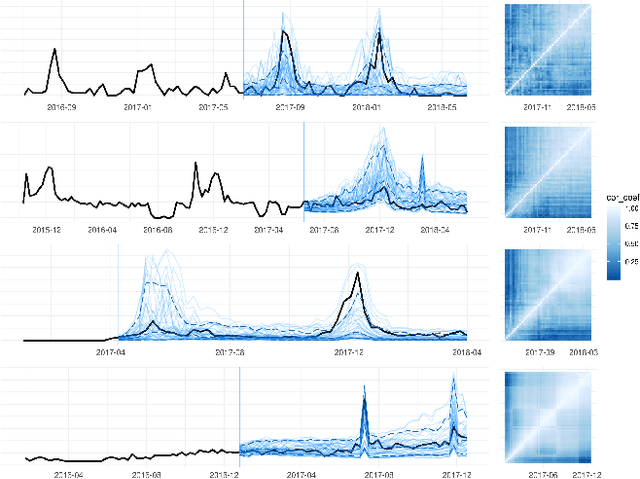

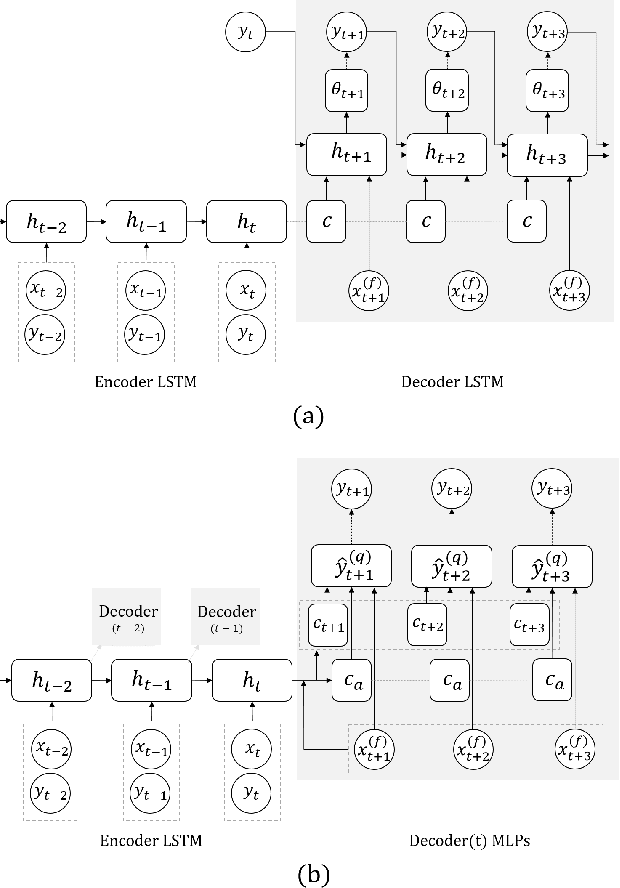

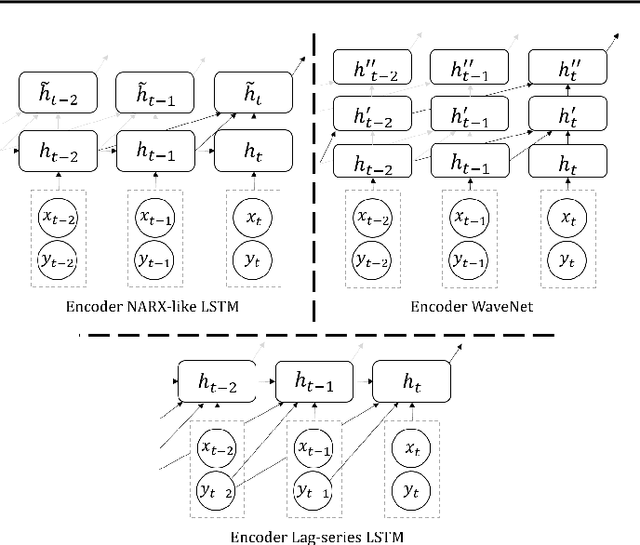

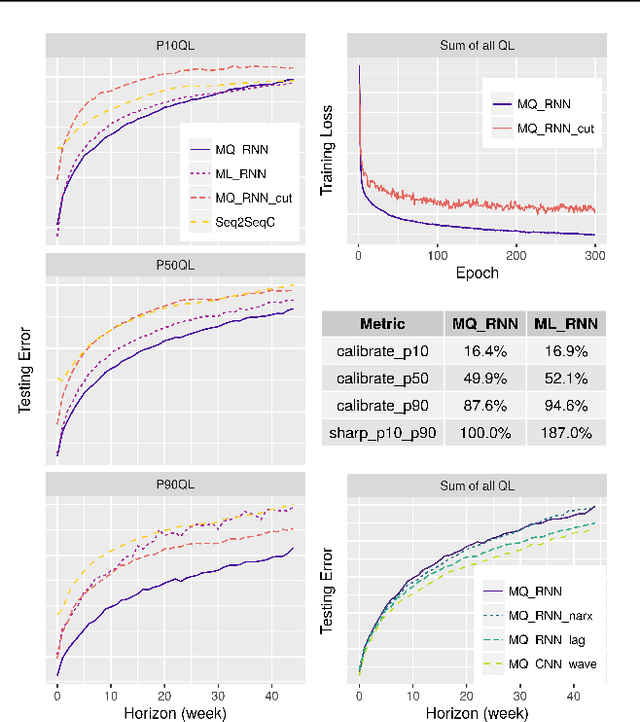

A Multi-Horizon Quantile Recurrent Forecaster

Jun 28, 2018

We propose a framework for general probabilistic multi-step time series regression. Specifically, we exploit the expressiveness and temporal nature of Sequence-to-Sequence Neural Networks (e.g. recurrent and convolutional structures), the nonparametric nature of Quantile Regression and the efficiency of Direct Multi-Horizon Forecasting. A new training scheme, *forking-sequences*, is designed for sequential nets to boost stability and performance. We show that the approach accommodates both temporal and static covariates, learning across multiple related series, shifting seasonality, future planned event spikes and cold-starts in real life large-scale forecasting. The performance of the framework is demonstrated in an application to predict the future demand of items sold on Amazon.com, and in a public probabilistic forecasting competition to predict electricity price and load.