Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAnalytical Results for Two Exponential Family Distributions in Hierarchical Dirichlet Processes

Feb 13, 2026The Hierarchical Dirichlet Process (HDP) provides a flexible Bayesian nonparametric framework for modeling grouped data with a shared yet unbounded collection of mixture components. While existing applications of the HDP predominantly focus on the Dirichlet-multinomial conjugate structure, the framework itself is considerably more general and, in principle, accommodates a broad class of conjugate prior-likelihood pairs. In particular, exponential family distributions offer a unified and analytically tractable modeling paradigm that encompasses many commonly used distributions. In this paper, we investigate analytic results for two important members of the exponential family within the HDP framework: the Poisson distribution and the normal distribution. We derive explicit closed-form expressions for the corresponding Gamma-Poisson and Normal-Gamma-Normal conjugate pairs under the hierarchical Dirichlet process construction. Detailed derivations and proofs are provided to clarify the underlying mathematical structure and to demonstrate how conjugacy can be systematically exploited in hierarchical nonparametric models. Our work extends the applicability of the HDP beyond the Dirichlet-multinomial setting and furnishes practical analytic results for researchers employing hierarchical Bayesian nonparametrics.

ProcGen3D: Learning Neural Procedural Graph Representations for Image-to-3D Reconstruction

Nov 10, 2025We introduce ProcGen3D, a new approach for 3D content creation by generating procedural graph abstractions of 3D objects, which can then be decoded into rich, complex 3D assets. Inspired by the prevalent use of procedural generators in production 3D applications, we propose a sequentialized, graph-based procedural graph representation for 3D assets. We use this to learn to approximate the landscape of a procedural generator for image-based 3D reconstruction. We employ edge-based tokenization to encode the procedural graphs, and train a transformer prior to predict the next token conditioned on an input RGB image. Crucially, to enable better alignment of our generated outputs to an input image, we incorporate Monte Carlo Tree Search (MCTS) guided sampling into our generation process, steering output procedural graphs towards more image-faithful reconstructions. Our approach is applicable across a variety of objects that can be synthesized with procedural generators. Extensive experiments on cacti, trees, and bridges show that our neural procedural graph generation outperforms both state-of-the-art generative 3D methods and domain-specific modeling techniques. Furthermore, this enables improved generalization on real-world input images, despite training only on synthetic data.

Logic-of-Thought: Empowering Large Language Models with Logic Programs for Solving Puzzles in Natural Language

May 22, 2025Solving puzzles in natural language poses a long-standing challenge in AI. While large language models (LLMs) have recently shown impressive capabilities in a variety of tasks, they continue to struggle with complex puzzles that demand precise reasoning and exhaustive search. In this paper, we propose Logic-of-Thought (Logot), a novel framework that bridges LLMs with logic programming to address this problem. Our method leverages LLMs to translate puzzle rules and states into answer set programs (ASPs), the solution of which are then accurately and efficiently inferred by an ASP interpreter. This hybrid approach combines the natural language understanding of LLMs with the precise reasoning capabilities of logic programs. We evaluate our method on various grid puzzles and dynamic puzzles involving actions, demonstrating near-perfect accuracy across all tasks. Our code and data are available at: https://github.com/naiqili/Logic-of-Thought.

Efficient Differentiable Approximation of Generalized Low-rank Regularization

May 21, 2025Low-rank regularization (LRR) has been widely applied in various machine learning tasks, but the associated optimization is challenging. Directly optimizing the rank function under constraints is NP-hard in general. To overcome this difficulty, various relaxations of the rank function were studied. However, optimization of these relaxed LRRs typically depends on singular value decomposition, which is a time-consuming and nondifferentiable operator that cannot be optimized with gradient-based techniques. To address these challenges, in this paper we propose an efficient differentiable approximation of the generalized LRR. The considered LRR form subsumes many popular choices like the nuclear norm, the Schatten-$p$ norm, and various nonconvex relaxations. Our method enables LRR terms to be appended to loss functions in a plug-and-play fashion, and the GPU-friendly operations enable efficient and convenient implementation. Furthermore, convergence analysis is presented, which rigorously shows that both the bias and the variance of our rank estimator rapidly reduce with increased sample size and iteration steps. In the experimental study, the proposed method is applied to various tasks, which demonstrates its versatility and efficiency. Code is available at https://github.com/naiqili/EDLRR.

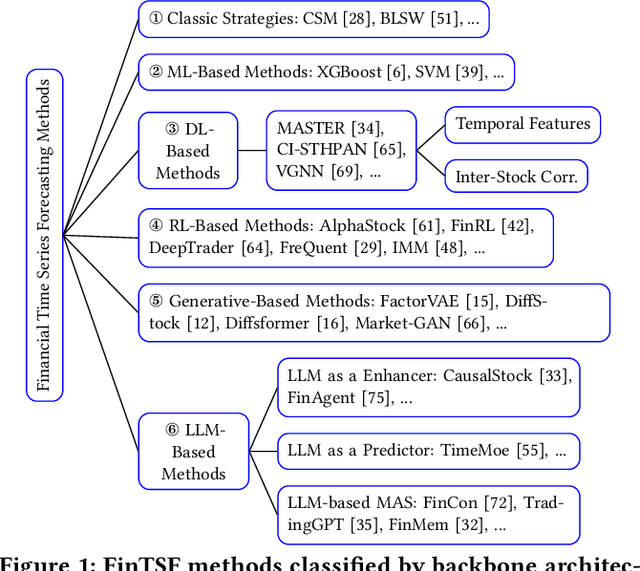

FinTSB: A Comprehensive and Practical Benchmark for Financial Time Series Forecasting

Feb 26, 2025

Financial time series (FinTS) record the behavior of human-brain-augmented decision-making, capturing valuable historical information that can be leveraged for profitable investment strategies. Not surprisingly, this area has attracted considerable attention from researchers, who have proposed a wide range of methods based on various backbones. However, the evaluation of the area often exhibits three systemic limitations: 1. Failure to account for the full spectrum of stock movement patterns observed in dynamic financial markets. (Diversity Gap), 2. The absence of unified assessment protocols undermines the validity of cross-study performance comparisons. (Standardization Deficit), and 3. Neglect of critical market structure factors, resulting in inflated performance metrics that lack practical applicability. (Real-World Mismatch). Addressing these limitations, we propose FinTSB, a comprehensive and practical benchmark for financial time series forecasting (FinTSF). To increase the variety, we categorize movement patterns into four specific parts, tokenize and pre-process the data, and assess the data quality based on some sequence characteristics. To eliminate biases due to different evaluation settings, we standardize the metrics across three dimensions and build a user-friendly, lightweight pipeline incorporating methods from various backbones. To accurately simulate real-world trading scenarios and facilitate practical implementation, we extensively model various regulatory constraints, including transaction fees, among others. Finally, we conduct extensive experiments on FinTSB, highlighting key insights to guide model selection under varying market conditions. Overall, FinTSB provides researchers with a novel and comprehensive platform for improving and evaluating FinTSF methods. The code is available at https://github.com/TongjiFinLab/FinTSBenchmark.

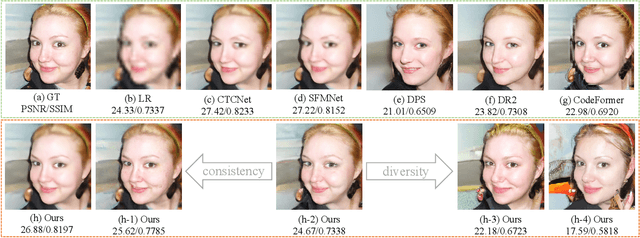

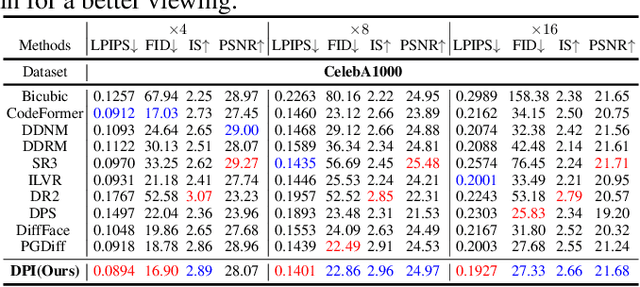

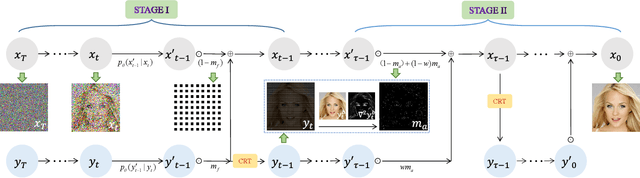

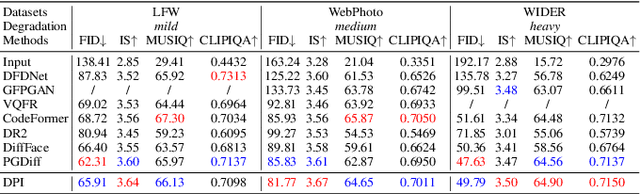

Diffusion Prior Interpolation for Flexibility Real-World Face Super-Resolution

Dec 21, 2024

Diffusion models represent the state-of-the-art in generative modeling. Due to their high training costs, many works leverage pre-trained diffusion models' powerful representations for downstream tasks, such as face super-resolution (FSR), through fine-tuning or prior-based methods. However, relying solely on priors without supervised training makes it challenging to meet the pixel-level accuracy requirements of discrimination task. Although prior-based methods can achieve high fidelity and high-quality results, ensuring consistency remains a significant challenge. In this paper, we propose a masking strategy with strong and weak constraints and iterative refinement for real-world FSR, termed Diffusion Prior Interpolation (DPI). We introduce conditions and constraints on consistency by masking different sampling stages based on the structural characteristics of the face. Furthermore, we propose a condition Corrector (CRT) to establish a reciprocal posterior sampling process, enhancing FSR performance by mutual refinement of conditions and samples. DPI can balance consistency and diversity and can be seamlessly integrated into pre-trained models. In extensive experiments conducted on synthetic and real datasets, along with consistency validation in face recognition, DPI demonstrates superiority over SOTA FSR methods. The code is available at \url{https://github.com/JerryYann/DPI}.

DNF: Unconditional 4D Generation with Dictionary-based Neural Fields

Dec 06, 2024

While remarkable success has been achieved through diffusion-based 3D generative models for shapes, 4D generative modeling remains challenging due to the complexity of object deformations over time. We propose DNF, a new 4D representation for unconditional generative modeling that efficiently models deformable shapes with disentangled shape and motion while capturing high-fidelity details in the deforming objects. To achieve this, we propose a dictionary learning approach to disentangle 4D motion from shape as neural fields. Both shape and motion are represented as learned latent spaces, where each deformable shape is represented by its shape and motion global latent codes, shape-specific coefficient vectors, and shared dictionary information. This captures both shape-specific detail and global shared information in the learned dictionary. Our dictionary-based representation well balances fidelity, contiguity and compression -- combined with a transformer-based diffusion model, our method is able to generate effective, high-fidelity 4D animations.

TimeBridge: Non-Stationarity Matters for Long-term Time Series Forecasting

Oct 06, 2024

Non-stationarity poses significant challenges for multivariate time series forecasting due to the inherent short-term fluctuations and long-term trends that can lead to spurious regressions or obscure essential long-term relationships. Most existing methods either eliminate or retain non-stationarity without adequately addressing its distinct impacts on short-term and long-term modeling. Eliminating non-stationarity is essential for avoiding spurious regressions and capturing local dependencies in short-term modeling, while preserving it is crucial for revealing long-term cointegration across variates. In this paper, we propose TimeBridge, a novel framework designed to bridge the gap between non-stationarity and dependency modeling in long-term time series forecasting. By segmenting input series into smaller patches, TimeBridge applies Integrated Attention to mitigate short-term non-stationarity and capture stable dependencies within each variate, while Cointegrated Attention preserves non-stationarity to model long-term cointegration across variates. Extensive experiments show that TimeBridge consistently achieves state-of-the-art performance in both short-term and long-term forecasting. Additionally, TimeBridge demonstrates exceptional performance in financial forecasting on the CSI 500 and S&P 500 indices, further validating its robustness and effectiveness. Code is available at \url{https://github.com/Hank0626/TimeBridge}.

LCM: Locally Constrained Compact Point Cloud Model for Masked Point Modeling

May 27, 2024

The pre-trained point cloud model based on Masked Point Modeling (MPM) has exhibited substantial improvements across various tasks. However, these models heavily rely on the Transformer, leading to quadratic complexity and limited decoder, hindering their practice application. To address this limitation, we first conduct a comprehensive analysis of existing Transformer-based MPM, emphasizing the idea that redundancy reduction is crucial for point cloud analysis. To this end, we propose a Locally constrained Compact point cloud Model (LCM) consisting of a locally constrained compact encoder and a locally constrained Mamba-based decoder. Our encoder replaces self-attention with our local aggregation layers to achieve an elegant balance between performance and efficiency. Considering the varying information density between masked and unmasked patches in the decoder inputs of MPM, we introduce a locally constrained Mamba-based decoder. This decoder ensures linear complexity while maximizing the perception of point cloud geometry information from unmasked patches with higher information density. Extensive experimental results show that our compact model significantly surpasses existing Transformer-based models in both performance and efficiency, especially our LCM-based Point-MAE model, compared to the Transformer-based model, achieved an improvement of 2.24%, 0.87%, and 0.94% in performance on the three variants of ScanObjectNN while reducing parameters by 88% and computation by 73%.

Taming Pre-trained LLMs for Generalised Time Series Forecasting via Cross-modal Knowledge Distillation

Mar 12, 2024Multivariate time series forecasting has recently gained great success with the rapid growth of deep learning models. However, existing approaches usually train models from scratch using limited temporal data, preventing their generalization. Recently, with the surge of the Large Language Models (LLMs), several works have attempted to introduce LLMs into time series forecasting. Despite promising results, these methods directly take time series as the input to LLMs, ignoring the inherent modality gap between temporal and text data. In this work, we propose a novel Large Language Models and time series alignment framework, dubbed LLaTA, to fully unleash the potentials of LLMs in the time series forecasting challenge. Based on cross-modal knowledge distillation, the proposed method exploits both input-agnostic static knowledge and input-dependent dynamic knowledge in pre-trained LLMs. In this way, it empowers the forecasting model with favorable performance as well as strong generalization abilities. Extensive experiments demonstrate the proposed method establishes a new state of the art for both long- and short-term forecasting. Code is available at \url{https://github.com/Hank0626/LLaTA}.