Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCP Loss: Channel-wise Perceptual Loss for Time Series Forecasting

Jan 25, 2026Multi-channel time-series data, prevalent across diverse applications, is characterized by significant heterogeneity in its different channels. However, existing forecasting models are typically guided by channel-agnostic loss functions like MSE, which apply a uniform metric across all channels. This often leads to fail to capture channel-specific dynamics such as sharp fluctuations or trend shifts. To address this, we propose a Channel-wise Perceptual Loss (CP Loss). Its core idea is to learn a unique perceptual space for each channel that is adapted to its characteristics, and to compute the loss within this space. Specifically, we first design a learnable channel-wise filter that decomposes the raw signal into disentangled multi-scale representations, which form the basis of our perceptual space. Crucially, the filter is optimized jointly with the main forecasting model, ensuring that the learned perceptual space is explicitly oriented towards the prediction task. Finally, losses are calculated within these perception spaces to optimize the model. Code is available at https://github.com/zyh16143998882/CP_Loss.

Bridging Past and Future: Distribution-Aware Alignment for Time Series Forecasting

Sep 17, 2025Representation learning techniques like contrastive learning have long been explored in time series forecasting, mirroring their success in computer vision and natural language processing. Yet recent state-of-the-art (SOTA) forecasters seldom adopt these representation approaches because they have shown little performance advantage. We challenge this view and demonstrate that explicit representation alignment can supply critical information that bridges the distributional gap between input histories and future targets. To this end, we introduce TimeAlign, a lightweight, plug-and-play framework that learns auxiliary features via a simple reconstruction task and feeds them back to any base forecaster. Extensive experiments across eight benchmarks verify its superior performance. Further studies indicate that the gains arises primarily from correcting frequency mismatches between historical inputs and future outputs. We also provide a theoretical justification for the effectiveness of TimeAlign in increasing the mutual information between learned representations and predicted targets. As it is architecture-agnostic and incurs negligible overhead, TimeAlign can serve as a general alignment module for modern deep learning time-series forecasting systems. The code is available at https://github.com/TROUBADOUR000/TimeAlign.

Logic-of-Thought: Empowering Large Language Models with Logic Programs for Solving Puzzles in Natural Language

May 22, 2025Solving puzzles in natural language poses a long-standing challenge in AI. While large language models (LLMs) have recently shown impressive capabilities in a variety of tasks, they continue to struggle with complex puzzles that demand precise reasoning and exhaustive search. In this paper, we propose Logic-of-Thought (Logot), a novel framework that bridges LLMs with logic programming to address this problem. Our method leverages LLMs to translate puzzle rules and states into answer set programs (ASPs), the solution of which are then accurately and efficiently inferred by an ASP interpreter. This hybrid approach combines the natural language understanding of LLMs with the precise reasoning capabilities of logic programs. We evaluate our method on various grid puzzles and dynamic puzzles involving actions, demonstrating near-perfect accuracy across all tasks. Our code and data are available at: https://github.com/naiqili/Logic-of-Thought.

Efficient Differentiable Approximation of Generalized Low-rank Regularization

May 21, 2025Low-rank regularization (LRR) has been widely applied in various machine learning tasks, but the associated optimization is challenging. Directly optimizing the rank function under constraints is NP-hard in general. To overcome this difficulty, various relaxations of the rank function were studied. However, optimization of these relaxed LRRs typically depends on singular value decomposition, which is a time-consuming and nondifferentiable operator that cannot be optimized with gradient-based techniques. To address these challenges, in this paper we propose an efficient differentiable approximation of the generalized LRR. The considered LRR form subsumes many popular choices like the nuclear norm, the Schatten-$p$ norm, and various nonconvex relaxations. Our method enables LRR terms to be appended to loss functions in a plug-and-play fashion, and the GPU-friendly operations enable efficient and convenient implementation. Furthermore, convergence analysis is presented, which rigorously shows that both the bias and the variance of our rank estimator rapidly reduce with increased sample size and iteration steps. In the experimental study, the proposed method is applied to various tasks, which demonstrates its versatility and efficiency. Code is available at https://github.com/naiqili/EDLRR.

Embodied Escaping: End-to-End Reinforcement Learning for Robot Navigation in Narrow Environment

Mar 05, 2025

Autonomous navigation is a fundamental task for robot vacuum cleaners in indoor environments. Since their core function is to clean entire areas, robots inevitably encounter dead zones in cluttered and narrow scenarios. Existing planning methods often fail to escape due to complex environmental constraints, high-dimensional search spaces, and high difficulty maneuvers. To address these challenges, this paper proposes an embodied escaping model that leverages reinforcement learning-based policy with an efficient action mask for dead zone escaping. To alleviate the issue of the sparse reward in training, we introduce a hybrid training policy that improves learning efficiency. In handling redundant and ineffective action options, we design a novel action representation to reshape the discrete action space with a uniform turning radius. Furthermore, we develop an action mask strategy to select valid action quickly, balancing precision and efficiency. In real-world experiments, our robot is equipped with a Lidar, IMU, and two-wheel encoders. Extensive quantitative and qualitative experiments across varying difficulty levels demonstrate that our robot can consistently escape from challenging dead zones. Moreover, our approach significantly outperforms compared path planning and reinforcement learning methods in terms of success rate and collision avoidance.

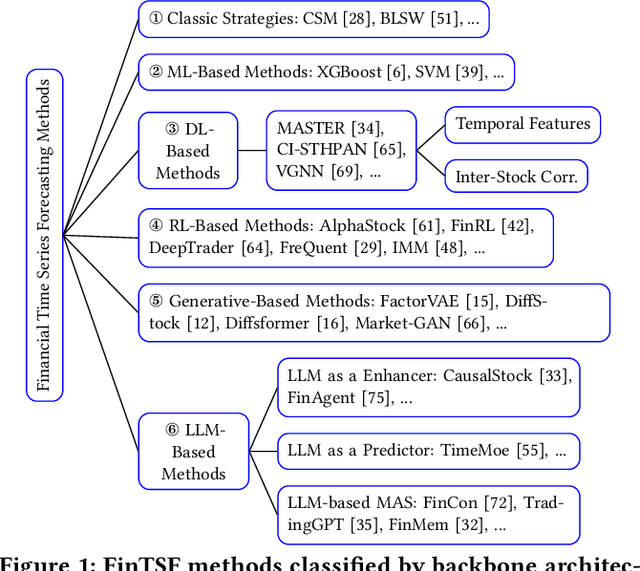

FinTSB: A Comprehensive and Practical Benchmark for Financial Time Series Forecasting

Feb 26, 2025

Financial time series (FinTS) record the behavior of human-brain-augmented decision-making, capturing valuable historical information that can be leveraged for profitable investment strategies. Not surprisingly, this area has attracted considerable attention from researchers, who have proposed a wide range of methods based on various backbones. However, the evaluation of the area often exhibits three systemic limitations: 1. Failure to account for the full spectrum of stock movement patterns observed in dynamic financial markets. (Diversity Gap), 2. The absence of unified assessment protocols undermines the validity of cross-study performance comparisons. (Standardization Deficit), and 3. Neglect of critical market structure factors, resulting in inflated performance metrics that lack practical applicability. (Real-World Mismatch). Addressing these limitations, we propose FinTSB, a comprehensive and practical benchmark for financial time series forecasting (FinTSF). To increase the variety, we categorize movement patterns into four specific parts, tokenize and pre-process the data, and assess the data quality based on some sequence characteristics. To eliminate biases due to different evaluation settings, we standardize the metrics across three dimensions and build a user-friendly, lightweight pipeline incorporating methods from various backbones. To accurately simulate real-world trading scenarios and facilitate practical implementation, we extensively model various regulatory constraints, including transaction fees, among others. Finally, we conduct extensive experiments on FinTSB, highlighting key insights to guide model selection under varying market conditions. Overall, FinTSB provides researchers with a novel and comprehensive platform for improving and evaluating FinTSF methods. The code is available at https://github.com/TongjiFinLab/FinTSBenchmark.

Mitigating Time Discretization Challenges with WeatherODE: A Sandwich Physics-Driven Neural ODE for Weather Forecasting

Oct 09, 2024In the field of weather forecasting, traditional models often grapple with discretization errors and time-dependent source discrepancies, which limit their predictive performance. In this paper, we present WeatherODE, a novel one-stage, physics-driven ordinary differential equation (ODE) model designed to enhance weather forecasting accuracy. By leveraging wave equation theory and integrating a time-dependent source model, WeatherODE effectively addresses the challenges associated with time-discretization error and dynamic atmospheric processes. Moreover, we design a CNN-ViT-CNN sandwich structure, facilitating efficient learning dynamics tailored for distinct yet interrelated tasks with varying optimization biases in advection equation estimation. Through rigorous experiments, WeatherODE demonstrates superior performance in both global and regional weather forecasting tasks, outperforming recent state-of-the-art approaches by significant margins of over 40.0\% and 31.8\% in root mean square error (RMSE), respectively. The source code is available at \url{https://github.com/DAMO-DI-ML/WeatherODE}.

TimeBridge: Non-Stationarity Matters for Long-term Time Series Forecasting

Oct 06, 2024

Non-stationarity poses significant challenges for multivariate time series forecasting due to the inherent short-term fluctuations and long-term trends that can lead to spurious regressions or obscure essential long-term relationships. Most existing methods either eliminate or retain non-stationarity without adequately addressing its distinct impacts on short-term and long-term modeling. Eliminating non-stationarity is essential for avoiding spurious regressions and capturing local dependencies in short-term modeling, while preserving it is crucial for revealing long-term cointegration across variates. In this paper, we propose TimeBridge, a novel framework designed to bridge the gap between non-stationarity and dependency modeling in long-term time series forecasting. By segmenting input series into smaller patches, TimeBridge applies Integrated Attention to mitigate short-term non-stationarity and capture stable dependencies within each variate, while Cointegrated Attention preserves non-stationarity to model long-term cointegration across variates. Extensive experiments show that TimeBridge consistently achieves state-of-the-art performance in both short-term and long-term forecasting. Additionally, TimeBridge demonstrates exceptional performance in financial forecasting on the CSI 500 and S&P 500 indices, further validating its robustness and effectiveness. Code is available at \url{https://github.com/Hank0626/TimeBridge}.

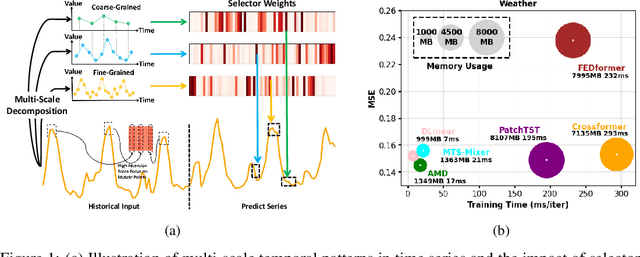

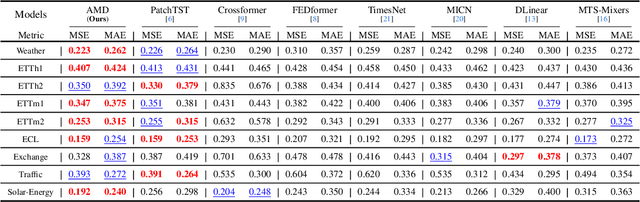

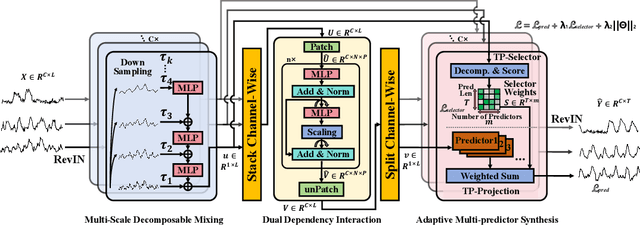

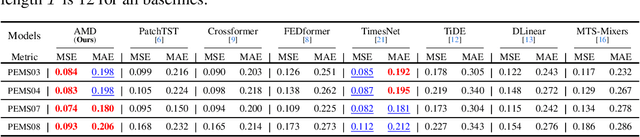

Adaptive Multi-Scale Decomposition Framework for Time Series Forecasting

Jun 06, 2024

Transformer-based and MLP-based methods have emerged as leading approaches in time series forecasting (TSF). While Transformer-based methods excel in capturing long-range dependencies, they suffer from high computational complexities and tend to overfit. Conversely, MLP-based methods offer computational efficiency and adeptness in modeling temporal dynamics, but they struggle with capturing complex temporal patterns effectively. To address these challenges, we propose a novel MLP-based Adaptive Multi-Scale Decomposition (AMD) framework for TSF. Our framework decomposes time series into distinct temporal patterns at multiple scales, leveraging the Multi-Scale Decomposable Mixing (MDM) block to dissect and aggregate these patterns in a residual manner. Complemented by the Dual Dependency Interaction (DDI) block and the Adaptive Multi-predictor Synthesis (AMS) block, our approach effectively models both temporal and channel dependencies and utilizes autocorrelation to refine multi-scale data integration. Comprehensive experiments demonstrate that our AMD framework not only overcomes the limitations of existing methods but also consistently achieves state-of-the-art performance in both long-term and short-term forecasting tasks across various datasets, showcasing superior efficiency. Code is available at \url{https://github.com/TROUBADOUR000/AMD}

Taming Pre-trained LLMs for Generalised Time Series Forecasting via Cross-modal Knowledge Distillation

Mar 12, 2024Multivariate time series forecasting has recently gained great success with the rapid growth of deep learning models. However, existing approaches usually train models from scratch using limited temporal data, preventing their generalization. Recently, with the surge of the Large Language Models (LLMs), several works have attempted to introduce LLMs into time series forecasting. Despite promising results, these methods directly take time series as the input to LLMs, ignoring the inherent modality gap between temporal and text data. In this work, we propose a novel Large Language Models and time series alignment framework, dubbed LLaTA, to fully unleash the potentials of LLMs in the time series forecasting challenge. Based on cross-modal knowledge distillation, the proposed method exploits both input-agnostic static knowledge and input-dependent dynamic knowledge in pre-trained LLMs. In this way, it empowers the forecasting model with favorable performance as well as strong generalization abilities. Extensive experiments demonstrate the proposed method establishes a new state of the art for both long- and short-term forecasting. Code is available at \url{https://github.com/Hank0626/LLaTA}.