Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeParameterized Physics-informed Neural Networks for Parameterized PDEs

Aug 18, 2024

Complex physical systems are often described by partial differential equations (PDEs) that depend on parameters such as the Reynolds number in fluid mechanics. In applications such as design optimization or uncertainty quantification, solutions of those PDEs need to be evaluated at numerous points in the parameter space. While physics-informed neural networks (PINNs) have emerged as a new strong competitor as a surrogate, their usage in this scenario remains underexplored due to the inherent need for repetitive and time-consuming training. In this paper, we address this problem by proposing a novel extension, parameterized physics-informed neural networks (P$^2$INNs). P$^2$INNs enable modeling the solutions of parameterized PDEs via explicitly encoding a latent representation of PDE parameters. With the extensive empirical evaluation, we demonstrate that P$^2$INNs outperform the baselines both in accuracy and parameter efficiency on benchmark 1D and 2D parameterized PDEs and are also effective in overcoming the known "failure modes".

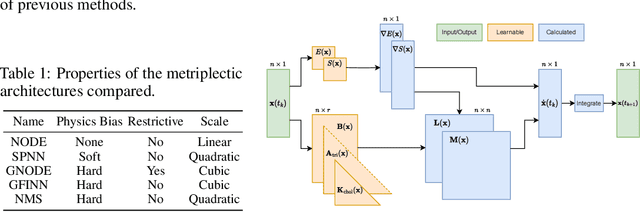

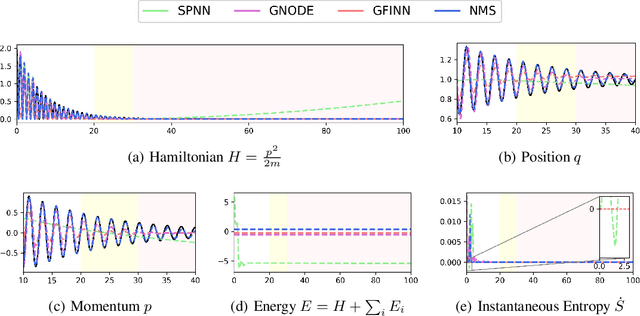

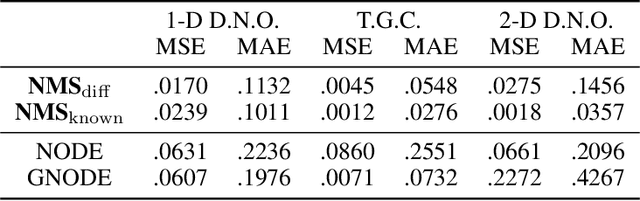

Efficiently Parameterized Neural Metriplectic Systems

May 28, 2024

Metriplectic systems are learned from data in a way that scales quadratically in both the size of the state and the rank of the metriplectic data. Besides being provably energy conserving and entropy stable, the proposed approach comes with approximation results demonstrating its ability to accurately learn metriplectic dynamics from data as well as an error estimate indicating its potential for generalization to unseen timescales when approximation error is low. Examples are provided which illustrate performance in the presence of both full state information as well as when entropic variables are unknown, confirming that the proposed approach exhibits superior accuracy and scalability without compromising on model expressivity.

Long-term Time Series Forecasting based on Decomposition and Neural Ordinary Differential Equations

Nov 10, 2023

Long-term time series forecasting (LTSF) is a challenging task that has been investigated in various domains such as finance investment, health care, traffic, and weather forecasting. In recent years, Linear-based LTSF models showed better performance, pointing out the problem of Transformer-based approaches causing temporal information loss. However, Linear-based approach has also limitations that the model is too simple to comprehensively exploit the characteristics of the dataset. To solve these limitations, we propose LTSF-DNODE, which applies a model based on linear ordinary differential equations (ODEs) and a time series decomposition method according to data statistical characteristics. We show that LTSF-DNODE outperforms the baselines on various real-world datasets. In addition, for each dataset, we explore the impacts of regularization in the neural ordinary differential equation (NODE) framework.

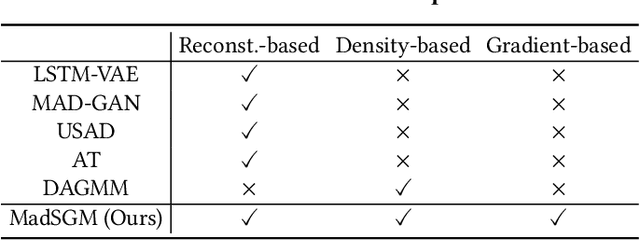

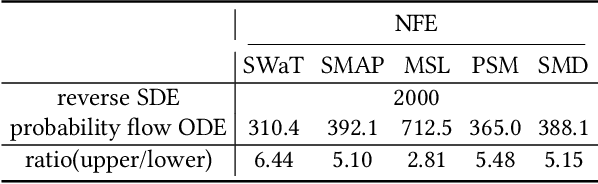

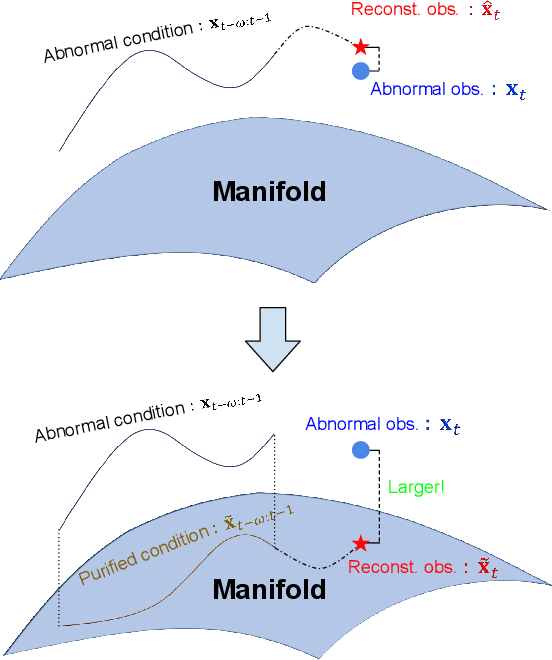

MadSGM: Multivariate Anomaly Detection with Score-based Generative Models

Aug 29, 2023

The time-series anomaly detection is one of the most fundamental tasks for time-series. Unlike the time-series forecasting and classification, the time-series anomaly detection typically requires unsupervised (or self-supervised) training since collecting and labeling anomalous observations are difficult. In addition, most existing methods resort to limited forms of anomaly measurements and therefore, it is not clear whether they are optimal in all circumstances. To this end, we present a multivariate time-series anomaly detector based on score-based generative models, called MadSGM, which considers the broadest ever set of anomaly measurement factors: i) reconstruction-based, ii) density-based, and iii) gradient-based anomaly measurements. We also design a conditional score network and its denoising score matching loss for the time-series anomaly detection. Experiments on five real-world benchmark datasets illustrate that MadSGM achieves the most robust and accurate predictions.

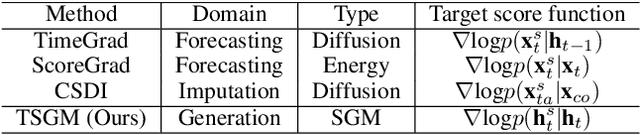

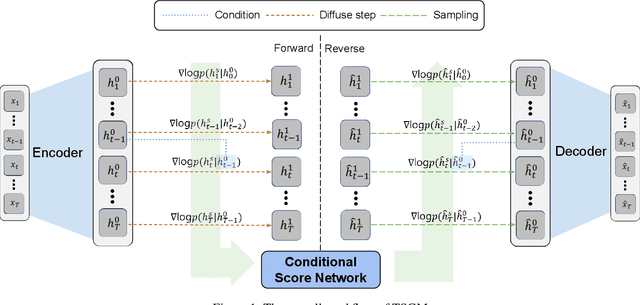

Regular Time-series Generation using SGM

Jan 20, 2023

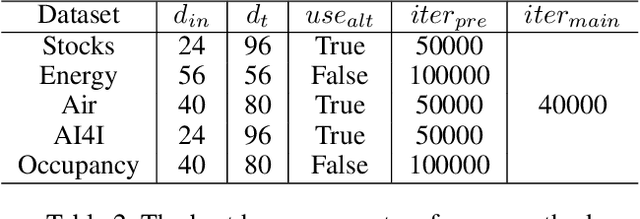

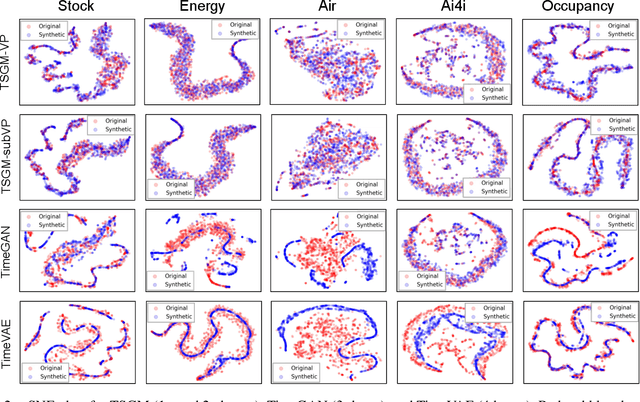

Score-based generative models (SGMs) are generative models that are in the spotlight these days. Time-series frequently occurs in our daily life, e.g., stock data, climate data, and so on. Especially, time-series forecasting and classification are popular research topics in the field of machine learning. SGMs are also known for outperforming other generative models. As a result, we apply SGMs to synthesize time-series data by learning conditional score functions. We propose a conditional score network for the time-series generation domain. Furthermore, we also derive the loss function between the score matching and the denoising score matching in the time-series generation domain. Finally, we achieve state-of-the-art results on real-world datasets in terms of sampling diversity and quality.

Time Series Forecasting with Hypernetworks Generating Parameters in Advance

Nov 22, 2022

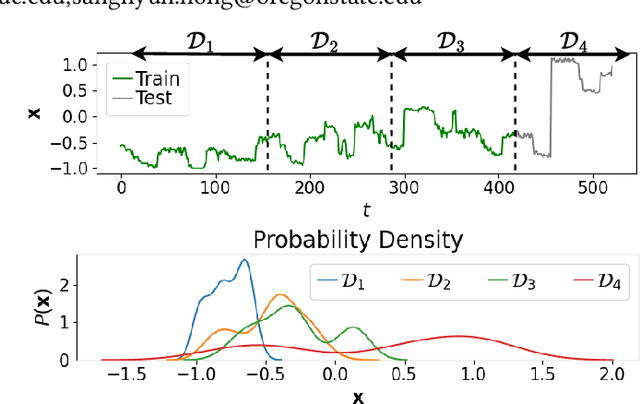

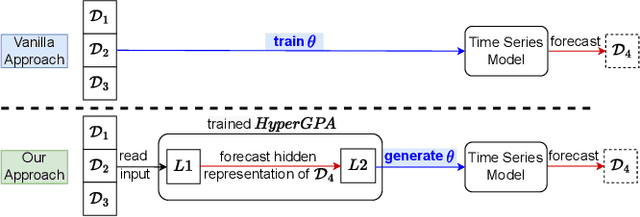

Forecasting future outcomes from recent time series data is not easy, especially when the future data are different from the past (i.e. time series are under temporal drifts). Existing approaches show limited performances under data drifts, and we identify the main reason: It takes time for a model to collect sufficient training data and adjust its parameters for complicated temporal patterns whenever the underlying dynamics change. To address this issue, we study a new approach; instead of adjusting model parameters (by continuously re-training a model on new data), we build a hypernetwork that generates other target models' parameters expected to perform well on the future data. Therefore, we can adjust the model parameters beforehand (if the hypernetwork is correct). We conduct extensive experiments with 6 target models, 6 baselines, and 4 datasets, and show that our HyperGPA outperforms other baselines.