Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRW-TTT: Batched Serving for Request-Owned Test-Time Training State

May 27, 2026Test-time training (TTT) adapts an LLM during generation by reading and updating request-owned state, such as fast weights, low-rank deltas, or streaming learner state. This breaks batched LLM serving, which assumes shared static weights: serial execution is correct but slow, while naive batching can corrupt request state. We formulate this problem as read-write TTT serving and present RW-TTT , which tags each decode step with its owner, version, and READ/WRITE effect, batches only compatible phases, and commits updates only to the owner. On one GPU with eight fast-weight InPlace-TTT streams, RW-TTT reaches 274.61 aggregate tok/s, 9.31x over sequential serving and 3.44x over per-stream replicas under the same memory budget. It preserves behavior on RULER, a long-context benchmark, and passes owner/version checks.

Sparse Causal Discovery with Generative Intervention for Unsupervised Graph Domain Adaptation

Jul 10, 2025Unsupervised Graph Domain Adaptation (UGDA) leverages labeled source domain graphs to achieve effective performance in unlabeled target domains despite distribution shifts. However, existing methods often yield suboptimal results due to the entanglement of causal-spurious features and the failure of global alignment strategies. We propose SLOGAN (Sparse Causal Discovery with Generative Intervention), a novel approach that achieves stable graph representation transfer through sparse causal modeling and dynamic intervention mechanisms. Specifically, SLOGAN first constructs a sparse causal graph structure, leveraging mutual information bottleneck constraints to disentangle sparse, stable causal features while compressing domain-dependent spurious correlations through variational inference. To address residual spurious correlations, we innovatively design a generative intervention mechanism that breaks local spurious couplings through cross-domain feature recombination while maintaining causal feature semantic consistency via covariance constraints. Furthermore, to mitigate error accumulation in target domain pseudo-labels, we introduce a category-adaptive dynamic calibration strategy, ensuring stable discriminative learning. Extensive experiments on multiple real-world datasets demonstrate that SLOGAN significantly outperforms existing baselines.

Surgery-R1: Advancing Surgical-VQLA with Reasoning Multimodal Large Language Model via Reinforcement Learning

Jun 24, 2025In recent years, significant progress has been made in the field of surgical scene understanding, particularly in the task of Visual Question Localized-Answering in robotic surgery (Surgical-VQLA). However, existing Surgical-VQLA models lack deep reasoning capabilities and interpretability in surgical scenes, which limits their reliability and potential for development in clinical applications. To address this issue, inspired by the development of Reasoning Multimodal Large Language Models (MLLMs), we first build the Surgery-R1-54k dataset, including paired data for Visual-QA, Grounding-QA, and Chain-of-Thought (CoT). Then, we propose the first Reasoning MLLM for Surgical-VQLA (Surgery-R1). In our Surgery-R1, we design a two-stage fine-tuning mechanism to enable the basic MLLM with complex reasoning abilities by utilizing supervised fine-tuning (SFT) and reinforcement fine-tuning (RFT). Furthermore, for an efficient and high-quality rule-based reward system in our RFT, we design a Multimodal Coherence reward mechanism to mitigate positional illusions that may arise in surgical scenarios. Experiment results demonstrate that Surgery-R1 outperforms other existing state-of-the-art (SOTA) models in the Surgical-VQLA task and widely-used MLLMs, while also validating its reasoning capabilities and the effectiveness of our approach. The code and dataset will be organized in https://github.com/FiFi-HAO467/Surgery-R1.

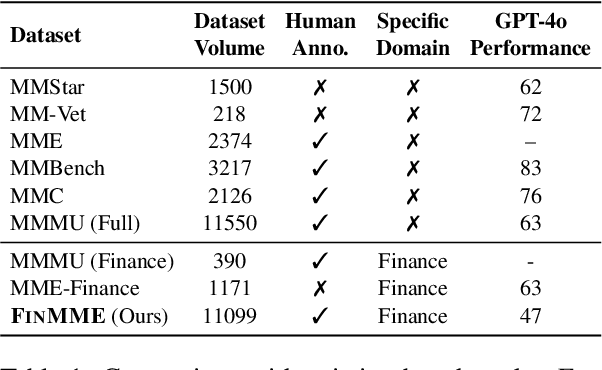

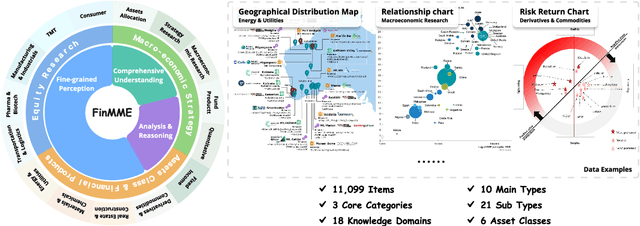

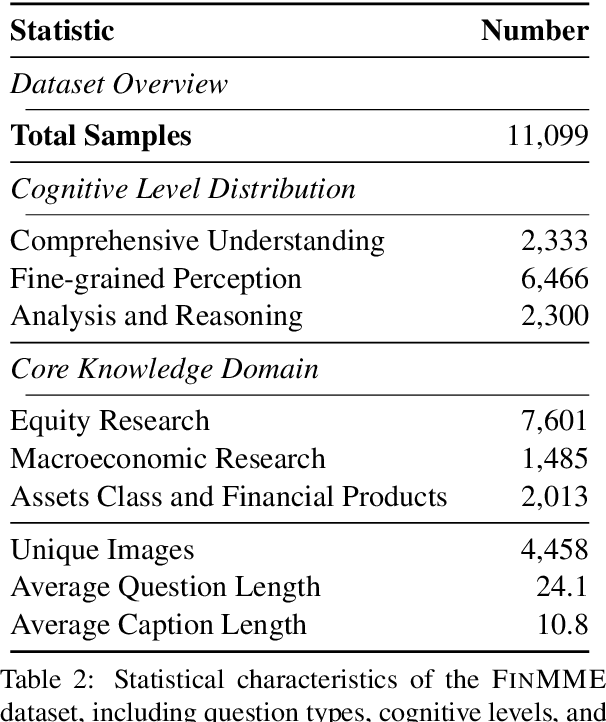

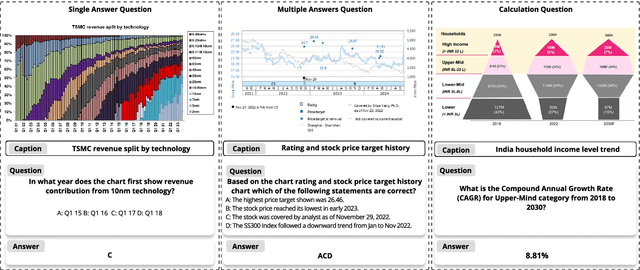

FinMME: Benchmark Dataset for Financial Multi-Modal Reasoning Evaluation

May 30, 2025

Multimodal Large Language Models (MLLMs) have experienced rapid development in recent years. However, in the financial domain, there is a notable lack of effective and specialized multimodal evaluation datasets. To advance the development of MLLMs in the finance domain, we introduce FinMME, encompassing more than 11,000 high-quality financial research samples across 18 financial domains and 6 asset classes, featuring 10 major chart types and 21 subtypes. We ensure data quality through 20 annotators and carefully designed validation mechanisms. Additionally, we develop FinScore, an evaluation system incorporating hallucination penalties and multi-dimensional capability assessment to provide an unbiased evaluation. Extensive experimental results demonstrate that even state-of-the-art models like GPT-4o exhibit unsatisfactory performance on FinMME, highlighting its challenging nature. The benchmark exhibits high robustness with prediction variations under different prompts remaining below 1%, demonstrating superior reliability compared to existing datasets. Our dataset and evaluation protocol are available at https://huggingface.co/datasets/luojunyu/FinMME and https://github.com/luo-junyu/FinMME.

Automate Strategy Finding with LLM in Quant investment

Sep 10, 2024

Despite significant progress in deep learning for financial trading, existing models often face instability and high uncertainty, hindering their practical application. Leveraging advancements in Large Language Models (LLMs) and multi-agent architectures, we propose a novel framework for quantitative stock investment in portfolio management and alpha mining. Our framework addresses these issues by integrating LLMs to generate diversified alphas and employing a multi-agent approach to dynamically evaluate market conditions. This paper proposes a framework where large language models (LLMs) mine alpha factors from multimodal financial data, ensuring a comprehensive understanding of market dynamics. The first module extracts predictive signals by integrating numerical data, research papers, and visual charts. The second module uses ensemble learning to construct a diverse pool of trading agents with varying risk preferences, enhancing strategy performance through a broader market analysis. In the third module, a dynamic weight-gating mechanism selects and assigns weights to the most relevant agents based on real-time market conditions, enabling the creation of an adaptive and context-aware composite alpha formula. Extensive experiments on the Chinese stock markets demonstrate that this framework significantly outperforms state-of-the-art baselines across multiple financial metrics. The results underscore the efficacy of combining LLM-generated alphas with a multi-agent architecture to achieve superior trading performance and stability. This work highlights the potential of AI-driven approaches in enhancing quantitative investment strategies and sets a new benchmark for integrating advanced machine learning techniques in financial trading can also be applied on diverse markets.

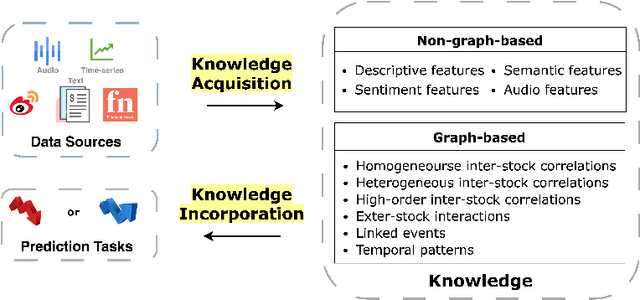

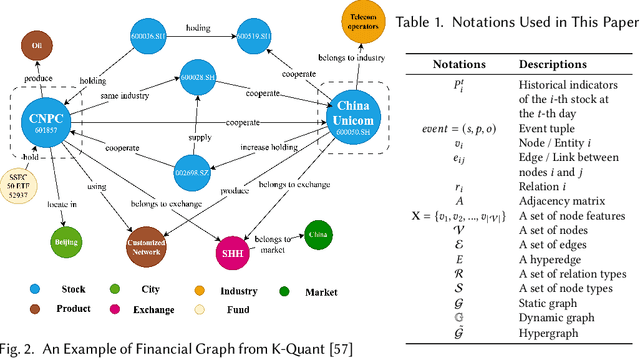

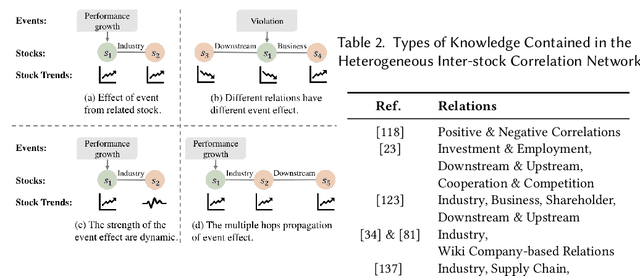

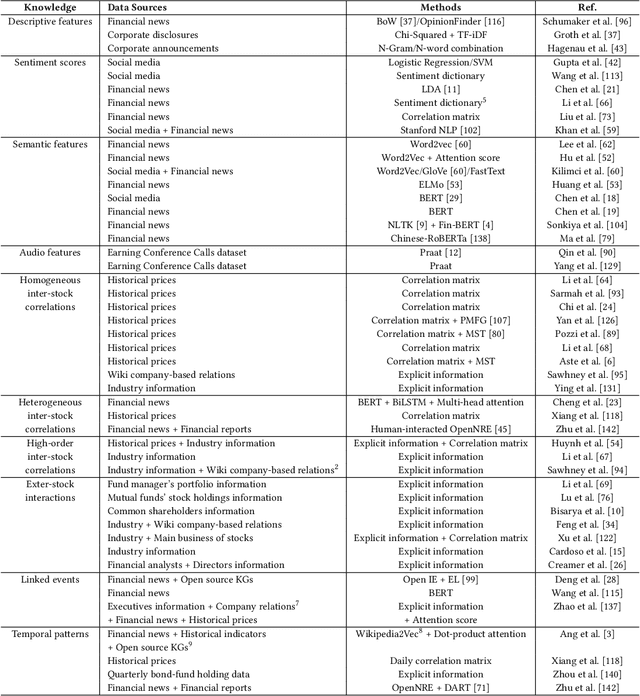

Methods for Acquiring and Incorporating Knowledge into Stock Price Prediction: A Survey

Aug 09, 2023

Predicting stock prices presents a challenging research problem due to the inherent volatility and non-linear nature of the stock market. In recent years, knowledge-enhanced stock price prediction methods have shown groundbreaking results by utilizing external knowledge to understand the stock market. Despite the importance of these methods, there is a scarcity of scholarly works that systematically synthesize previous studies from the perspective of external knowledge types. Specifically, the external knowledge can be modeled in different data structures, which we group into non-graph-based formats and graph-based formats: 1) non-graph-based knowledge captures contextual information and multimedia descriptions specifically associated with an individual stock; 2) graph-based knowledge captures interconnected and interdependent information in the stock market. This survey paper aims to provide a systematic and comprehensive description of methods for acquiring external knowledge from various unstructured data sources and then incorporating it into stock price prediction models. We also explore fusion methods for combining external knowledge with historical price features. Moreover, this paper includes a compilation of relevant datasets and delves into potential future research directions in this domain.