Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMethods for Acquiring and Incorporating Knowledge into Stock Price Prediction: A Survey

Paper and Code

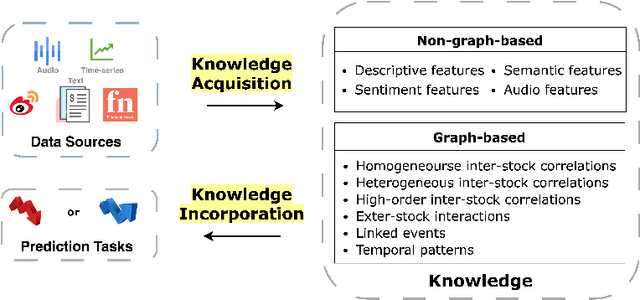

Predicting stock prices presents a challenging research problem due to the inherent volatility and non-linear nature of the stock market. In recent years, knowledge-enhanced stock price prediction methods have shown groundbreaking results by utilizing external knowledge to understand the stock market. Despite the importance of these methods, there is a scarcity of scholarly works that systematically synthesize previous studies from the perspective of external knowledge types. Specifically, the external knowledge can be modeled in different data structures, which we group into non-graph-based formats and graph-based formats: 1) non-graph-based knowledge captures contextual information and multimedia descriptions specifically associated with an individual stock; 2) graph-based knowledge captures interconnected and interdependent information in the stock market. This survey paper aims to provide a systematic and comprehensive description of methods for acquiring external knowledge from various unstructured data sources and then incorporating it into stock price prediction models. We also explore fusion methods for combining external knowledge with historical price features. Moreover, this paper includes a compilation of relevant datasets and delves into potential future research directions in this domain.