Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

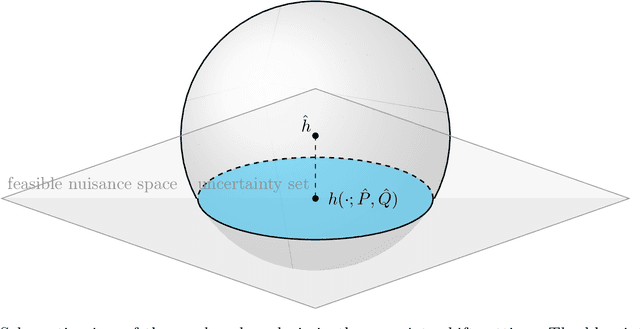

Add to EdgeAdaptive Estimation and Inference in Conditional Moment Models via the Discrepancy Principle

Mar 02, 2026We study adaptive estimation and inference in ill-posed linear inverse problems defined by conditional moment restrictions. Existing regularized estimators such as Regularized DeepIV (RDIV) require prior knowledge of the smoothness of the nuisance function, typically encoded by a beta source condition to tune their regularization parameters. In practice, this smoothness is unknown, and misspecified hyperparameters can lead to suboptimal convergence or instability. We introduce a discrepancy-principle-based framework for adaptive hyperparameter selection that automatically balances bias and variance without relying on the unknown smoothness parameter. Our framework applies to both RDIV (Li et al. [2024]) and the Tikhonov Regularized Adversarial Estimator (TRAE) (Bennett et al. [2023a]) and achieves the same rates in both weak and strong metrics. Building on this, we construct a fully adaptive doubly robust estimator for linear functionals that attains the optimal rate of the better-conditioned primal or dual problem, providing a practical, theoretically grounded approach for adaptive inference in ill-posed econometric models.

CausalReasoningBenchmark: A Real-World Benchmark for Disentangled Evaluation of Causal Identification and Estimation

Feb 24, 2026Many benchmarks for automated causal inference evaluate a system's performance based on a single numerical output, such as an Average Treatment Effect (ATE). This approach conflates two distinct steps in causal analysis: identification-formulating a valid research design under stated assumptions-and estimation-implementing that design numerically on finite data. We introduce CausalReasoningBenchmark, a benchmark of 173 queries across 138 real-world datasets, curated from 85 peer-reviewed research papers and four widely-used causal-inference textbooks. For each query a system must produce (i) a structured identification specification that names the strategy, the treatment, outcome, and control variables, and all design-specific elements, and (ii) a point estimate with a standard error. By scoring these two components separately, our benchmark enables granular diagnosis: it distinguishes failures in causal reasoning from errors in numerical execution. Baseline results with a state-of-the-art LLM show that, while the model correctly identifies the high-level strategy in 84 % of cases, full identification-specification correctness drops to only 30 %, revealing that the bottleneck lies in the nuanced details of research design rather than in computation. CausalReasoningBenchmark is publicly available on Hugging Face and is designed to foster the development of more robust automated causal-inference systems.

Prescriptive Scaling Reveals the Evolution of Language Model Capabilities

Feb 17, 2026For deploying foundation models, practitioners increasingly need prescriptive scaling laws: given a pre training compute budget, what downstream accuracy is attainable with contemporary post training practice, and how stable is that mapping as the field evolves? Using large scale observational evaluations with 5k observational and 2k newly sampled data on model performance, we estimate capability boundaries, high conditional quantiles of benchmark scores as a function of log pre training FLOPs, via smoothed quantile regression with a monotone, saturating sigmoid parameterization. We validate the temporal reliability by fitting on earlier model generations and evaluating on later releases. Across various tasks, the estimated boundaries are mostly stable, with the exception of math reasoning that exhibits a consistently advancing boundary over time. We then extend our approach to analyze task dependent saturation and to probe contamination related shifts on math reasoning tasks. Finally, we introduce an efficient algorithm that recovers near full data frontiers using roughly 20% of evaluation budget. Together, our work releases the Proteus 2k, the latest model performance evaluation dataset, and introduces a practical methodology for translating compute budgets into reliable performance expectations and for monitoring when capability boundaries shift across time.

Statistical Inference and Learning for Shapley Additive Explanations (SHAP)

Feb 11, 2026The SHAP (short for Shapley additive explanation) framework has become an essential tool for attributing importance to variables in predictive tasks. In model-agnostic settings, SHAP uses the concept of Shapley values from cooperative game theory to fairly allocate credit to the features in a vector $X$ based on their contribution to an outcome $Y$. While the explanations offered by SHAP are local by nature, learners often need global measures of feature importance in order to improve model explainability and perform feature selection. The most common approach for converting these local explanations into global ones is to compute either the mean absolute SHAP or mean squared SHAP. However, despite their ubiquity, there do not exist approaches for performing statistical inference on these quantities. In this paper, we take a semi-parametric approach for calibrating confidence in estimates of the $p$th powers of Shapley additive explanations. We show that, by treating the SHAP curve as a nuisance function that must be estimated from data, one can reliably construct asymptotically normal estimates of the $p$th powers of SHAP. When $p \geq 2$, we show a de-biased estimator that combines U-statistics with Neyman orthogonal scores for functionals of nested regressions is asymptotically normal. When $1 \leq p < 2$ (and the hence target parameter is not twice differentiable), we construct de-biased U-statistics for a smoothed alternative. In particular, we show how to carefully tune the temperature parameter of the smoothing function in order to obtain inference for the true, unsmoothed $p$th power. We complement these results by presenting a Neyman orthogonal loss that can be used to learn the SHAP curve via empirical risk minimization and discussing excess risk guarantees for commonly used function classes.

Sharp Structure-Agnostic Lower Bounds for General Functional Estimation

Dec 19, 2025

The design of efficient nonparametric estimators has long been a central problem in statistics, machine learning, and decision making. Classical optimal procedures often rely on strong structural assumptions, which can be misspecified in practice and complicate deployment. This limitation has sparked growing interest in structure-agnostic approaches -- methods that debias black-box nuisance estimates without imposing structural priors. Understanding the fundamental limits of these methods is therefore crucial. This paper provides a systematic investigation of the optimal error rates achievable by structure-agnostic estimators. We first show that, for estimating the average treatment effect (ATE), a central parameter in causal inference, doubly robust learning attains optimal structure-agnostic error rates. We then extend our analysis to a general class of functionals that depend on unknown nuisance functions and establish the structure-agnostic optimality of debiased/double machine learning (DML). We distinguish two regimes -- one where double robustness is attainable and one where it is not -- leading to different optimal rates for first-order debiasing, and show that DML is optimal in both regimes. Finally, we instantiate our general lower bounds by deriving explicit optimal rates that recover existing results and extend to additional estimands of interest. Our results provide theoretical validation for widely used first-order debiasing methods and guidance for practitioners seeking optimal approaches in the absence of structural assumptions. This paper generalizes and subsumes the ATE lower bound established in \citet{jin2024structure} by the same authors.

Inference on Optimal Policy Values and Other Irregular Functionals via Smoothing

Jul 15, 2025Constructing confidence intervals for the value of an optimal treatment policy is an important problem in causal inference. Insight into the optimal policy value can guide the development of reward-maximizing, individualized treatment regimes. However, because the functional that defines the optimal value is non-differentiable, standard semi-parametric approaches for performing inference fail to be directly applicable. Existing approaches for handling this non-differentiability fall roughly into two camps. In one camp are estimators based on constructing smooth approximations of the optimal value. These approaches are computationally lightweight, but typically place unrealistic parametric assumptions on outcome regressions. In another camp are approaches that directly de-bias the non-smooth objective. These approaches don't place parametric assumptions on nuisance functions, but they either require the computation of intractably-many nuisance estimates, assume unrealistic $L^\infty$ nuisance convergence rates, or make strong margin assumptions that prohibit non-response to a treatment. In this paper, we revisit the problem of constructing smooth approximations of non-differentiable functionals. By carefully controlling first-order bias and second-order remainders, we show that a softmax smoothing-based estimator can be used to estimate parameters that are specified as a maximum of scores involving nuisance components. In particular, this includes the value of the optimal treatment policy as a special case. Our estimator obtains $\sqrt{n}$ convergence rates, avoids parametric restrictions/unrealistic margin assumptions, and is often statistically efficient.

It's Hard to Be Normal: The Impact of Noise on Structure-agnostic Estimation

Jul 03, 2025Structure-agnostic causal inference studies how well one can estimate a treatment effect given black-box machine learning estimates of nuisance functions (like the impact of confounders on treatment and outcomes). Here, we find that the answer depends in a surprising way on the distribution of the treatment noise. Focusing on the partially linear model of \citet{robinson1988root}, we first show that the widely adopted double machine learning (DML) estimator is minimax rate-optimal for Gaussian treatment noise, resolving an open problem of \citet{mackey2018orthogonal}. Meanwhile, for independent non-Gaussian treatment noise, we show that DML is always suboptimal by constructing new practical procedures with higher-order robustness to nuisance errors. These \emph{ACE} procedures use structure-agnostic cumulant estimators to achieve $r$-th order insensitivity to nuisance errors whenever the $(r+1)$-st treatment cumulant is non-zero. We complement these core results with novel minimax guarantees for binary treatments in the partially linear model. Finally, using synthetic demand estimation experiments, we demonstrate the practical benefits of our higher-order robust estimators.

Discovering Hierarchical Latent Capabilities of Language Models via Causal Representation Learning

Jun 12, 2025Faithful evaluation of language model capabilities is crucial for deriving actionable insights that can inform model development. However, rigorous causal evaluations in this domain face significant methodological challenges, including complex confounding effects and prohibitive computational costs associated with extensive retraining. To tackle these challenges, we propose a causal representation learning framework wherein observed benchmark performance is modeled as a linear transformation of a few latent capability factors. Crucially, these latent factors are identified as causally interrelated after appropriately controlling for the base model as a common confounder. Applying this approach to a comprehensive dataset encompassing over 1500 models evaluated across six benchmarks from the Open LLM Leaderboard, we identify a concise three-node linear causal structure that reliably explains the observed performance variations. Further interpretation of this causal structure provides substantial scientific insights beyond simple numerical rankings: specifically, we reveal a clear causal direction starting from general problem-solving capabilities, advancing through instruction-following proficiency, and culminating in mathematical reasoning ability. Our results underscore the essential role of carefully controlling base model variations during evaluation, a step critical to accurately uncovering the underlying causal relationships among latent model capabilities.

Preference Learning with Response Time

May 28, 2025This paper investigates the integration of response time data into human preference learning frameworks for more effective reward model elicitation. While binary preference data has become fundamental in fine-tuning foundation models, generative AI systems, and other large-scale models, the valuable temporal information inherent in user decision-making remains largely unexploited. We propose novel methodologies to incorporate response time information alongside binary choice data, leveraging the Evidence Accumulation Drift Diffusion (EZ) model, under which response time is informative of the preference strength. We develop Neyman-orthogonal loss functions that achieve oracle convergence rates for reward model learning, matching the theoretical optimal rates that would be attained if the expected response times for each query were known a priori. Our theoretical analysis demonstrates that for linear reward functions, conventional preference learning suffers from error rates that scale exponentially with reward magnitude. In contrast, our response time-augmented approach reduces this to polynomial scaling, representing a significant improvement in sample efficiency. We extend these guarantees to non-parametric reward function spaces, establishing convergence properties for more complex, realistic reward models. Our extensive experiments validate our theoretical findings in the context of preference learning over images.

A Meta-learner for Heterogeneous Effects in Difference-in-Differences

Feb 07, 2025We address the problem of estimating heterogeneous treatment effects in panel data, adopting the popular Difference-in-Differences (DiD) framework under the conditional parallel trends assumption. We propose a novel doubly robust meta-learner for the Conditional Average Treatment Effect on the Treated (CATT), reducing the estimation to a convex risk minimization problem involving a set of auxiliary models. Our framework allows for the flexible estimation of the CATT, when conditioning on any subset of variables of interest using generic machine learning. Leveraging Neyman orthogonality, our proposed approach is robust to estimation errors in the auxiliary models. As a generalization to our main result, we develop a meta-learning approach for the estimation of general conditional functionals under covariate shift. We also provide an extension to the instrumented DiD setting with non-compliance. Empirical results demonstrate the superiority of our approach over existing baselines.