Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLLM for Large-Scale Optimization Model Auto-Formulation: A Lightweight Few-Shot Learning Approach

Jan 14, 2026Large-scale optimization is a key backbone of modern business decision-making. However, building these models is often labor-intensive and time-consuming. We address this by proposing LEAN-LLM-OPT, a LightwEight AgeNtic workflow construction framework for LLM-assisted large-scale OPTimization auto-formulation. LEAN-LLM-OPT takes as input a problem description together with associated datasets and orchestrates a team of LLM agents to produce an optimization formulation. Specifically, upon receiving a query, two upstream LLM agents dynamically construct a workflow that specifies, step-by-step, how optimization models for similar problems can be formulated. A downstream LLM agent then follows this workflow to generate the final output. Leveraging LLMs' text-processing capabilities and common modeling practices, the workflow decomposes the modeling task into a sequence of structured sub-tasks and offloads mechanical data-handling operations to auxiliary tools. This design alleviates the downstream agent's burden related to planning and data handling, allowing it to focus on the most challenging components that cannot be readily standardized. Extensive simulations show that LEAN-LLM-OPT, instantiated with GPT-4.1 and the open source gpt-oss-20B, achieves strong performance on large-scale optimization modeling tasks and is competitive with state-of-the-art approaches. In addition, in a Singapore Airlines choice-based revenue management use case, LEAN-LLM-OPT demonstrates practical value by achieving leading performance across a range of scenarios. Along the way, we introduce Large-Scale-OR and Air-NRM, the first comprehensive benchmarks for large-scale optimization auto-formulation. The code and data of this work is available at https://github.com/CoraLiang01/lean-llm-opt.

Contextual Online Pricing with (Biased) Offline Data

Jul 03, 2025We study contextual online pricing with biased offline data. For the scalar price elasticity case, we identify the instance-dependent quantity $\delta^2$ that measures how far the offline data lies from the (unknown) online optimum. We show that the time length $T$, bias bound $V$, size $N$ and dispersion $\lambda_{\min}(\hat{\Sigma})$ of the offline data, and $\delta^2$ jointly determine the statistical complexity. An Optimism-in-the-Face-of-Uncertainty (OFU) policy achieves a minimax-optimal, instance-dependent regret bound $\tilde{\mathcal{O}}\big(d\sqrt{T} \wedge (V^2T + \frac{dT}{\lambda_{\min}(\hat{\Sigma}) + (N \wedge T) \delta^2})\big)$. For general price elasticity, we establish a worst-case, minimax-optimal rate $\tilde{\mathcal{O}}\big(d\sqrt{T} \wedge (V^2T + \frac{dT }{\lambda_{\min}(\hat{\Sigma})})\big)$ and provide a generalized OFU algorithm that attains it. When the bias bound $V$ is unknown, we design a robust variant that always guarantees sub-linear regret and strictly improves on purely online methods whenever the exact bias is small. These results deliver the first tight regret guarantees for contextual pricing in the presence of biased offline data. Our techniques also transfer verbatim to stochastic linear bandits with biased offline data, yielding analogous bounds.

MERIT: A Merchant Incentive Ranking Model for Hotel Search & Ranking

Jun 10, 2025Online Travel Platforms (OTPs) have been working on improving their hotel Search & Ranking (S&R) systems that facilitate efficient matching between consumers and hotels. Existing OTPs focus almost exclusively on improving platform revenue. In this work, we take a first step in incorporating hotel merchants' objectives into the design of hotel S&R systems to achieve an incentive loop: the OTP tilts impressions and better-ranked positions to merchants with high quality, and in return, the merchants provide better service to consumers. Three critical design challenges need to be resolved to achieve this incentive loop: Matthew Effect in the consumer feedback-loop, unclear relation between hotel quality and performance, and conflicts between short-term and long-term revenue. To address these challenges, we propose MERIT, a MERchant IncenTive ranking model, which can simultaneously take the interests of merchants and consumers into account. We define a new Merchant Competitiveness Index (MCI) to represent hotel merchant quality and propose a new Merchant Tower to model the relation between MCI and ranking scores. Also, we design a monotonic structure for Merchant Tower to provide a clear relation between hotel quality and performance. Finally, we propose a Multi-objective Stratified Pairwise Loss, which can mitigate the conflicts between OTP's short-term and long-term revenue. The offline experiment results indicate that MERIT outperforms these methods in optimizing the demands of consumers and merchants. Furthermore, we conduct an online A/B test and obtain an improvement of 3.02% for the MCI score.

Reward Learning From Preference With Ties

Oct 05, 2024

Reward learning plays a pivotal role in Reinforcement Learning from Human Feedback (RLHF), ensuring the alignment of language models. The Bradley-Terry (BT) model stands as the prevalent choice for capturing human preferences from datasets containing pairs of chosen and rejected responses. In preference modeling, the focus is not on absolute values but rather on the reward difference between chosen and rejected responses, referred to as preference strength. Thus, precise evaluation of preference strength holds paramount importance in preference modeling. However, an easily overlooked factor significantly affecting preference strength measurement is that human attitudes towards two responses may not solely indicate a preference for one over the other and ties are also a common occurrence. To address this, we propose the adoption of the generalized Bradley-Terry model -- the Bradley-Terry model with ties (BTT) -- to accommodate tied preferences, thus leveraging additional information. We prove that even with the access to the true distributions of prompt and response, disregarding ties can lead to a notable bias in preference strength measurement. Comprehensive experiments further validate the advantages of incorporating ties in preference modeling. Notably, fine-tuning with BTT significantly outperforms fine-tuning with BT on synthetic preference datasets with ties, labeled by state-of-the-art open-source LLMs.

Satisficing Exploration in Bandit Optimization

Jun 10, 2024Motivated by the concept of satisficing in decision-making, we consider the problem of satisficing exploration in bandit optimization. In this setting, the learner aims at selecting satisficing arms (arms with mean reward exceeding a certain threshold value) as frequently as possible. The performance is measured by satisficing regret, which is the cumulative deficit of the chosen arm's mean reward compared to the threshold. We propose SELECT, a general algorithmic template for Satisficing Exploration via LowEr Confidence bound Testing, that attains constant satisficing regret for a wide variety of bandit optimization problems in the realizable case (i.e., a satisficing arm exists). Specifically, given a class of bandit optimization problems and a corresponding learning oracle with sub-linear (standard) regret upper bound, SELECT iteratively makes use of the oracle to identify a potential satisficing arm with low regret. Then, it collects data samples from this arm, and continuously compares the LCB of the identified arm's mean reward against the threshold value to determine if it is a satisficing arm. As a complement, SELECT also enjoys the same (standard) regret guarantee as the oracle in the non-realizable case. Finally, we conduct numerical experiments to validate the performance of SELECT for several popular bandit optimization settings.

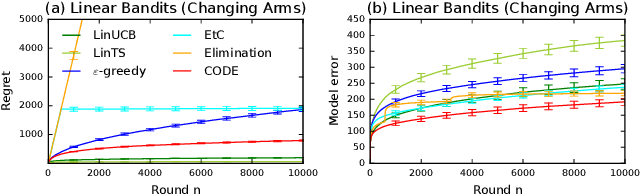

Efficient and Interpretable Bandit Algorithms

Oct 23, 2023

Motivated by the importance of explainability in modern machine learning, we design bandit algorithms that are \emph{efficient} and \emph{interpretable}. A bandit algorithm is interpretable if it explores with the objective of reducing uncertainty in the unknown model parameter. To quantify the interpretability, we introduce a novel metric of \textit{uncertainty loss}, which compares the rate of the uncertainty reduction to the theoretical optimum. We propose CODE, a bandit algorithm based on a \textbf{C}onstrained \textbf{O}ptimal \textbf{DE}sign, that is interpretable and maximally reduces the uncertainty. The key idea in \code is to explore among all plausible actions, determined by a statistical constraint, to achieve interpretability. We implement CODE efficiently in both multi-armed and linear bandits and derive near-optimal regret bounds by leveraging the optimality criteria of the approximate optimal design. CODE can be also viewed as removing phases in conventional phased elimination, which makes it more practical and general. We demonstrate the advantage of \code by numerical experiments on both synthetic and real-world problems. CODE outperforms other state-of-the-art interpretable designs while matching the performance of popular but uninterpretable designs, such as upper confidence bound algorithms.

User Experience Design Professionals' Perceptions of Generative Artificial Intelligence

Sep 26, 2023

Among creative professionals, Generative Artificial Intelligence (GenAI) has sparked excitement over its capabilities and fear over unanticipated consequences. How does GenAI impact User Experience Design (UXD) practice, and are fears warranted? We interviewed 20 UX Designers, with diverse experience and across companies (startups to large enterprises). We probed them to characterize their practices, and sample their attitudes, concerns, and expectations. We found that experienced designers are confident in their originality, creativity, and empathic skills, and find GenAI's role as assistive. They emphasized the unique human factors of "enjoyment" and "agency", where humans remain the arbiters of "AI alignment". However, skill degradation, job replacement, and creativity exhaustion can adversely impact junior designers. We discuss implications for human-GenAI collaboration, specifically copyright and ownership, human creativity and agency, and AI literacy and access. Through the lens of responsible and participatory AI, we contribute a deeper understanding of GenAI fears and opportunities for UXD.

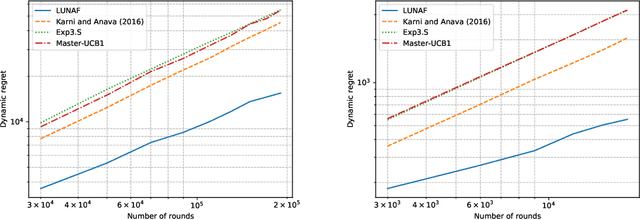

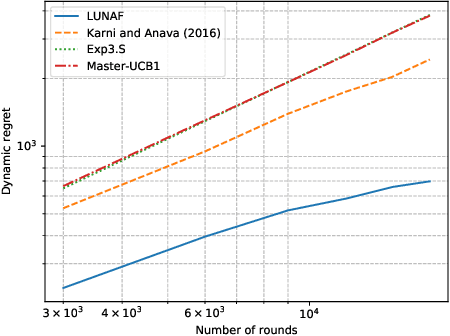

Phase Transitions in Learning and Earning under Price Protection Guarantee

Nov 03, 2022Motivated by the prevalence of ``price protection guarantee", which allows a customer who purchased a product in the past to receive a refund from the seller during the so-called price protection period (typically defined as a certain time window after the purchase date) in case the seller decides to lower the price, we study the impact of such policy on the design of online learning algorithm for data-driven dynamic pricing with initially unknown customer demand. We consider a setting where a firm sells a product over a horizon of $T$ time steps. For this setting, we characterize how the value of $M$, the length of price protection period, can affect the optimal regret of the learning process. We show that the optimal regret is $\tilde{\Theta}(\sqrt{T}+\min\{M,\,T^{2/3}\})$ by first establishing a fundamental impossible regime with novel regret lower bound instances. Then, we propose LEAP, a phased exploration type algorithm for \underline{L}earning and \underline{EA}rning under \underline{P}rice Protection to match this lower bound up to logarithmic factors or even doubly logarithmic factors (when there are only two prices available to the seller). Our results reveal the surprising phase transitions of the optimal regret with respect to $M$. Specifically, when $M$ is not too large, the optimal regret has no major difference when compared to that of the classic setting with no price protection guarantee. We also show that there exists an upper limit on how much the optimal regret can deteriorate when $M$ grows large. Finally, we conduct extensive numerical experiments to show the benefit of LEAP over other heuristic methods for this problem.

Learning to Price Supply Chain Contracts against a Learning Retailer

Nov 02, 2022

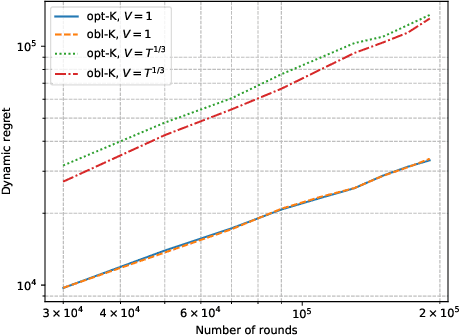

The rise of big data analytics has automated the decision-making of companies and increased supply chain agility. In this paper, we study the supply chain contract design problem faced by a data-driven supplier who needs to respond to the inventory decisions of the downstream retailer. Both the supplier and the retailer are uncertain about the market demand and need to learn about it sequentially. The goal for the supplier is to develop data-driven pricing policies with sublinear regret bounds under a wide range of possible retailer inventory policies for a fixed time horizon. To capture the dynamics induced by the retailer's learning policy, we first make a connection to non-stationary online learning by following the notion of variation budget. The variation budget quantifies the impact of the retailer's learning strategy on the supplier's decision-making. We then propose dynamic pricing policies for the supplier for both discrete and continuous demand. We also note that our proposed pricing policy only requires access to the support of the demand distribution, but critically, does not require the supplier to have any prior knowledge about the retailer's learning policy or the demand realizations. We examine several well-known data-driven policies for the retailer, including sample average approximation, distributionally robust optimization, and parametric approaches, and show that our pricing policies lead to sublinear regret bounds in all these cases. At the managerial level, we answer affirmatively that there is a pricing policy with a sublinear regret bound under a wide range of retailer's learning policies, even though she faces a learning retailer and an unknown demand distribution. Our work also provides a novel perspective in data-driven operations management where the principal has to learn to react to the learning policies employed by other agents in the system.

Risk-Aware Linear Bandits: Theory and Applications in Smart Order Routing

Aug 04, 2022

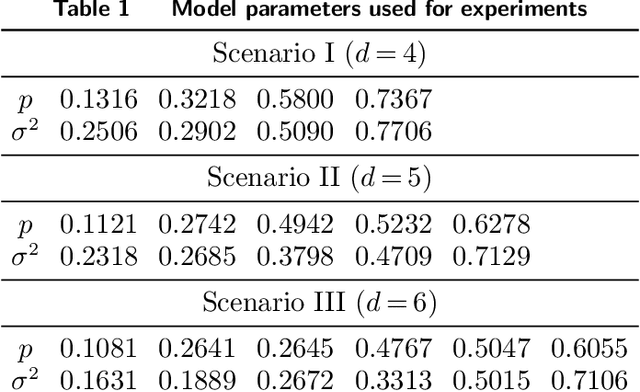

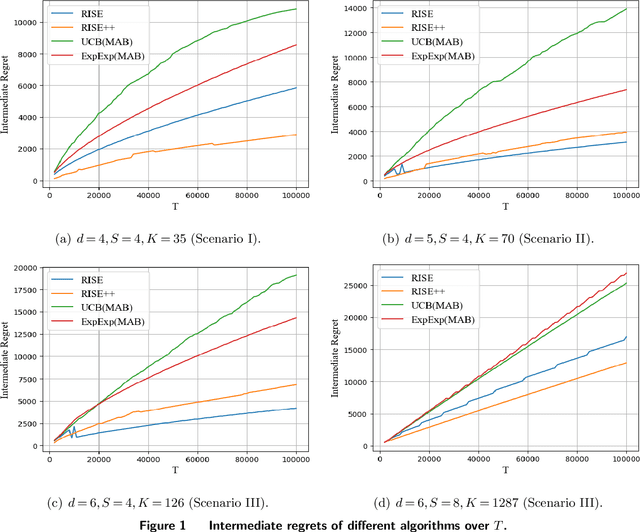

Motivated by practical considerations in machine learning for financial decision-making, such as risk-aversion and large action space, we initiate the study of risk-aware linear bandits. Specifically, we consider regret minimization under the mean-variance measure when facing a set of actions whose rewards can be expressed as linear functions of (initially) unknown parameters. Driven by the variance-minimizing G-optimal design, we propose the Risk-Aware Explore-then-Commit (RISE) algorithm and the Risk-Aware Successive Elimination (RISE++) algorithm. Then, we rigorously analyze their regret upper bounds to show that, by leveraging the linear structure, the algorithms can dramatically reduce the regret when compared to existing methods. Finally, we demonstrate the performance of the algorithms by conducting extensive numerical experiments in a synthetic smart order routing setup. Our results show that both RISE and RISE++ can outperform the competing methods, especially in complex decision-making scenarios.