Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOptimal Empirical Risk Minimization under Temporal Distribution Shifts

Jul 17, 2025Temporal distribution shifts pose a key challenge for machine learning models trained and deployed in dynamically evolving environments. This paper introduces RIDER (RIsk minimization under Dynamically Evolving Regimes) which derives optimally-weighted empirical risk minimization procedures under temporal distribution shifts. Our approach is theoretically grounded in the random distribution shift model, where random shifts arise as a superposition of numerous unpredictable changes in the data-generating process. We show that common weighting schemes, such as pooling all data, exponentially weighting data, and using only the most recent data, emerge naturally as special cases in our framework. We demonstrate that RIDER consistently improves out-of-sample predictive performance when applied as a fine-tuning step on the Yearbook dataset, across a range of benchmark methods in Wild-Time. Moreover, we show that RIDER outperforms standard weighting strategies in two other real-world tasks: predicting stock market volatility and forecasting ride durations in NYC taxi data.

The Effect of State Representation on LLM Agent Behavior in Dynamic Routing Games

Jun 18, 2025Large Language Models (LLMs) have shown promise as decision-makers in dynamic settings, but their stateless nature necessitates creating a natural language representation of history. We present a unifying framework for systematically constructing natural language "state" representations for prompting LLM agents in repeated multi-agent games. Previous work on games with LLM agents has taken an ad hoc approach to encoding game history, which not only obscures the impact of state representation on agents' behavior, but also limits comparability between studies. Our framework addresses these gaps by characterizing methods of state representation along three axes: action informativeness (i.e., the extent to which the state representation captures actions played); reward informativeness (i.e., the extent to which the state representation describes rewards obtained); and prompting style (or natural language compression, i.e., the extent to which the full text history is summarized). We apply this framework to a dynamic selfish routing game, chosen because it admits a simple equilibrium both in theory and in human subject experiments \cite{rapoport_choice_2009}. Despite the game's relative simplicity, we find that there are key dependencies of LLM agent behavior on the natural language state representation. In particular, we observe that representations which provide agents with (1) summarized, rather than complete, natural language representations of past history; (2) information about regrets, rather than raw payoffs; and (3) limited information about others' actions lead to behavior that more closely matches game theoretic equilibrium predictions, and with more stable game play by the agents. By contrast, other representations can exhibit either large deviations from equilibrium, higher variation in dynamic game play over time, or both.

Learning Explainable Treatment Policies with Clinician-Informed Representations: A Practical Approach

Nov 26, 2024

Digital health interventions (DHIs) and remote patient monitoring (RPM) have shown great potential in improving chronic disease management through personalized care. However, barriers like limited efficacy and workload concerns hinder adoption of existing DHIs; while limited sample sizes and lack of interpretability limit the effectiveness and adoption of purely black-box algorithmic DHIs. In this paper, we address these challenges by developing a pipeline for learning explainable treatment policies for RPM-enabled DHIs. We apply our approach in the real-world setting of RPM using a DHI to improve glycemic control of youth with type 1 diabetes. Our main contribution is to reveal the importance of clinical domain knowledge in developing state and action representations for effective, efficient, and interpretable targeting policies. We observe that policies learned from clinician-informed representations are significantly more efficacious and efficient than policies learned from black-box representations. This work emphasizes the importance of collaboration between ML researchers and clinicians for developing effective DHIs in the real world.

Hybrid Square Neural ODE Causal Modeling

Feb 27, 2024Hybrid models combine mechanistic ODE-based dynamics with flexible and expressive neural network components. Such models have grown rapidly in popularity, especially in scientific domains where such ODE-based modeling offers important interpretability and validated causal grounding (e.g., for counterfactual reasoning). The incorporation of mechanistic models also provides inductive bias in standard blackbox modeling approaches, critical when learning from small datasets or partially observed, complex systems. Unfortunately, as hybrid models become more flexible, the causal grounding provided by the mechanistic model can quickly be lost. We address this problem by leveraging another common source of domain knowledge: ranking of treatment effects for a set of interventions, even if the precise treatment effect is unknown. We encode this information in a causal loss that we combine with the standard predictive loss to arrive at a hybrid loss that biases our learning towards causally valid hybrid models. We demonstrate our ability to achieve a win-win -- state-of-the-art predictive performance and causal validity -- in the challenging task of modeling glucose dynamics during exercise.

Online Learning for Traffic Routing under Unknown Preferences

Mar 31, 2022

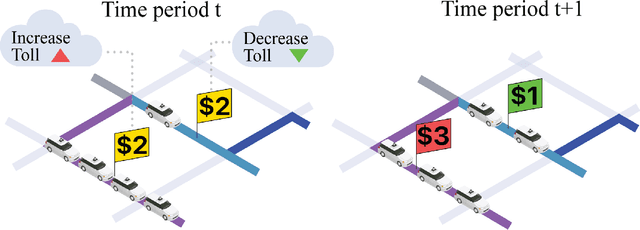

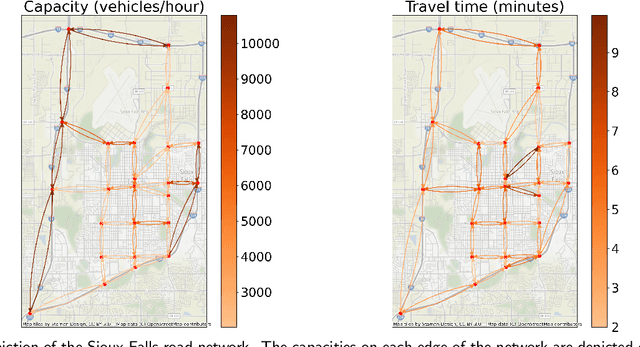

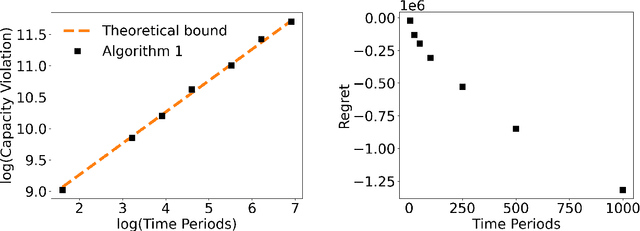

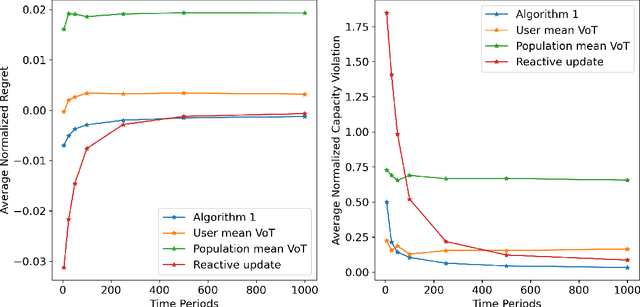

In transportation networks, users typically choose routes in a decentralized and self-interested manner to minimize their individual travel costs, which, in practice, often results in inefficient overall outcomes for society. As a result, there has been a growing interest in designing road tolling schemes to cope with these efficiency losses and steer users toward a system-efficient traffic pattern. However, the efficacy of road tolling schemes often relies on having access to complete information on users' trip attributes, such as their origin-destination (O-D) travel information and their values of time, which may not be available in practice. Motivated by this practical consideration, we propose an online learning approach to set tolls in a traffic network to drive heterogeneous users with different values of time toward a system-efficient traffic pattern. In particular, we develop a simple yet effective algorithm that adjusts tolls at each time period solely based on the observed aggregate flows on the roads of the network without relying on any additional trip attributes of users, thereby preserving user privacy. In the setting where the O-D pairs and values of time of users are drawn i.i.d. at each period, we show that our approach obtains an expected regret and road capacity violation of $O(\sqrt{T})$, where $T$ is the number of periods over which tolls are updated. Our regret guarantee is relative to an offline oracle that has complete information on users' trip attributes. We further establish a $\Omega(\sqrt{T})$ lower bound on the regret of any algorithm, which establishes that our algorithm is optimal up to constants. Finally, we demonstrate the superior performance of our approach relative to several benchmarks on a real-world transportation network, thereby highlighting its practical applicability.

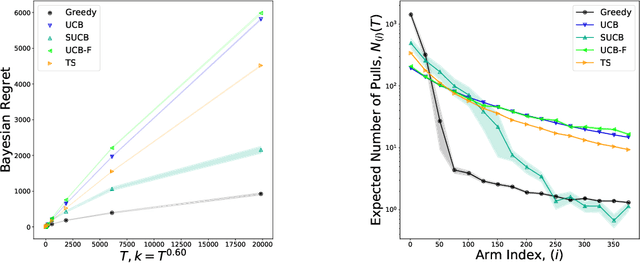

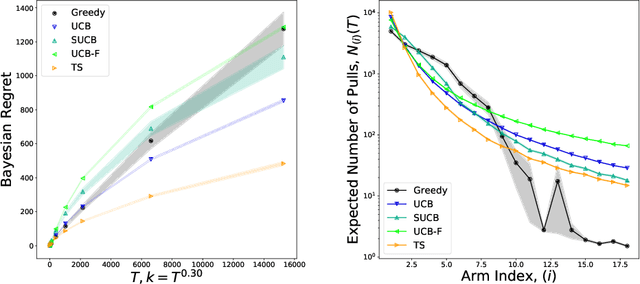

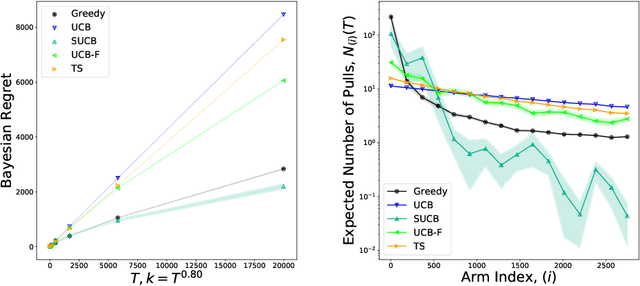

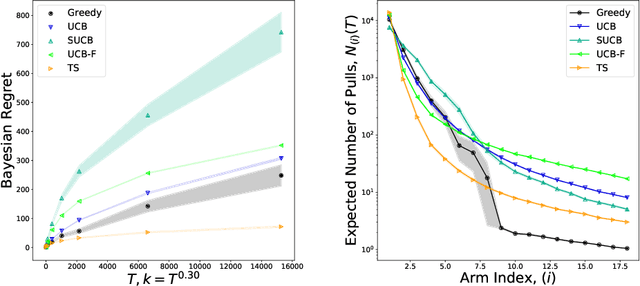

Optimal and Greedy Algorithms for Multi-Armed Bandits with Many Arms

Feb 24, 2020

We characterize Bayesian regret in a stochastic multi-armed bandit problem with a large but finite number of arms. In particular, we assume the number of arms $k$ is $T^{\alpha}$, where $T$ is the time-horizon and $\alpha$ is in $(0,1)$. We consider a Bayesian setting where the reward distribution of each arm is drawn independently from a common prior, and provide a complete analysis of expected regret with respect to this prior. Our results exhibit a sharp distinction around $\alpha = 1/2$. When $\alpha < 1/2$, the fundamental lower bound on regret is $\Omega(k)$; and it is achieved by a standard UCB algorithm. When $\alpha > 1/2$, the fundamental lower bound on regret is $\Omega(\sqrt{T})$, and it is achieved by an algorithm that first subsamples $\sqrt{T}$ arms uniformly at random, then runs UCB on just this subset. Interestingly, we also find that a sufficiently large number of arms allows the decision-maker to benefit from "free" exploration if she simply uses a greedy algorithm. In particular, this greedy algorithm exhibits a regret of $\tilde{O}(\max(k,T/\sqrt{k}))$, which translates to a {\em sublinear} (though not optimal) regret in the time horizon. We show empirically that this is because the greedy algorithm rapidly disposes of underperforming arms, a beneficial trait in the many-armed regime. Technically, our analysis of the greedy algorithm involves a novel application of the Lundberg inequality, an upper bound for the ruin probability of a random walk; this approach may be of independent interest.

Semi-parametric dynamic contextual pricing

Jan 07, 2019

We consider a canonical revenue maximization problem where customers arrive sequentially; each customer is interested in buying one product, and the customer purchases the product if her valuation for it exceeds the price set by the seller. The valuations of customers are not observed by the seller; however, the seller can leverage contextual information available to her in the form of noisy covariate vectors describing the customer's history and the product's type to set prices. The seller can learn the relationship between covariates and customer valuations by experimenting with prices and observing transaction outcomes. We consider a semi-parametric model where the relationship between the expectation of the log of valuation and the covariates is linear (hence parametric) and the residual uncertainty distribution, i.e., the noise distribution, is non-parametric. We develop a pricing policy, DEEP-C, which learns this relationship with minimal exploration and in turn achieves optimal regret asymptotically in the time horizon.

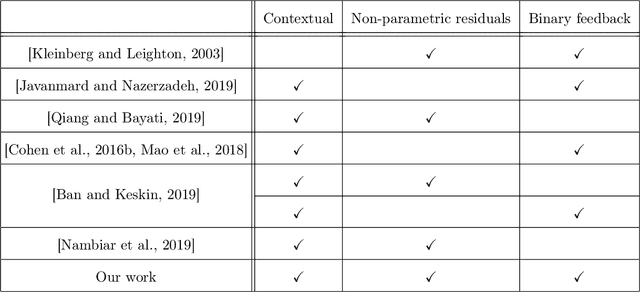

Designing Optimal Binary Rating Systems

Oct 28, 2018

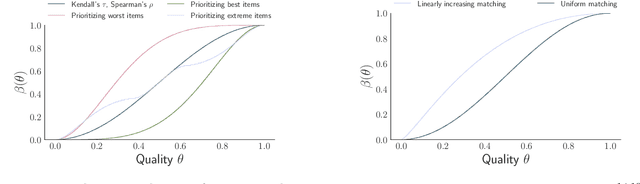

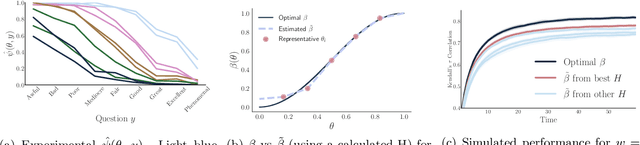

Modern online platforms rely on effective rating systems to learn about items. We consider the optimal design of rating systems that collect {\em binary feedback} after transactions. We make three contributions. First, we formalize the performance of a rating system as the speed with which it recovers the true underlying ranking on items (in a large deviations sense), accounting for both items' underlying match rates and the platform's preferences. Second, we provide an efficient algorithm to compute the binary feedback system that yields the highest such performance. Finally, we show how this theoretical perspective can be used to empirically design an implementable, approximately optimal rating system, and validate our approach using real-world experimental data collected on Amazon Mechanical Turk.

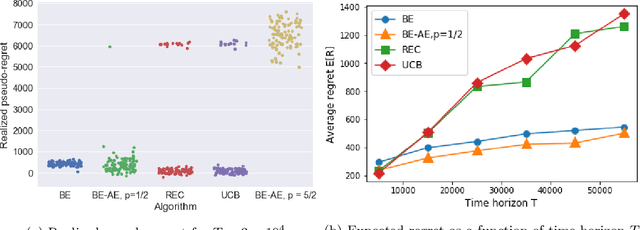

Bandit Learning with Positive Externalities

Oct 26, 2018

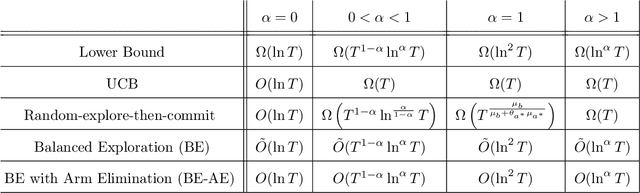

In many platforms, user arrivals exhibit a self-reinforcing behavior: future user arrivals are likely to have preferences similar to users who were satisfied in the past. In other words, arrivals exhibit positive externalities. We study multiarmed bandit (MAB) problems with positive externalities. We show that the self-reinforcing preferences may lead standard benchmark algorithms such as UCB to exhibit linear regret. We develop a new algorithm, Balanced Exploration (BE), which explores arms carefully to avoid suboptimal convergence of arrivals before sufficient evidence is gathered. We also introduce an adaptive variant of BE which successively eliminates suboptimal arms. We analyze their asymptotic regret, and establish optimality by showing that no algorithm can perform better.

Exploration vs. Exploitation in Team Formation

Oct 12, 2018

An online labor platform faces an online learning problem in matching workers with jobs and using the performance on these jobs to create better future matches. This learning problem is complicated by the rise of complex tasks on these platforms, such as web development and product design, that require a team of workers to complete. The success of a job is now a function of the skills and contributions of all workers involved, which may be unknown to both the platform and the client who posted the job. These team matchings result in a structured correlation between what is known about the individuals and this information can be utilized to create better future matches. We analyze two natural settings where the performance of a team is dictated by its strongest and its weakest member, respectively. We find that both problems pose an exploration-exploitation tradeoff between learning the performance of untested teams and repeating previously tested teams that resulted in a good performance. We establish fundamental regret bounds and design near-optimal algorithms that uncover several insights into these tradeoffs.