Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFrom Soliloquy to Agora: Memory-Enhanced LLM Agents with Decentralized Debate for Optimization Modeling

Apr 28, 2026Optimization modeling underpins real-world decision-making in logistics, manufacturing, energy, and public services, but reliably solving such problems from natural-language requirements remains challenging for current large language models (LLMs). In this paper, we propose \emph{Agora-Opt}, a modular agentic framework for optimization modeling that combines decentralized debate with a read-write memory bank. Agora-Opt allows multiple agent teams to independently produce end-to-end solutions and reconcile them through an outcome-grounded debate protocol, while memory stores solver-verified artifacts and past disagreement resolutions to support training-free improvement over time. This design is flexible across both backbones and methods: it reduces base-model lock-in, transfers across different LLM families, and can be layered onto existing pipelines with minimal coupling. Across public benchmarks, Agora-Opt achieves the strongest overall performance among all compared methods, outperforming strong zero-shot LLMs, training-centric approaches, and prior agentic baselines. Further analyses show robust gains across backbone choices and component variants, and demonstrate that decentralized debate offers a structural advantage over centralized selection by enabling agents to refine candidate solutions through interaction and even recover correct formulations when all initial candidates are flawed. These results suggest that reliable optimization modeling benefits from combining collaborative cross-checking with reusable experience, and position Agora-Opt as a practical and extensible foundation for trustworthy optimization modeling assistance. Our code and data are available at https://github.com/CHIANGEL/Agora-Opt.

SimRecon: SimReady Compositional Scene Reconstruction from Real Videos

Mar 03, 2026Compositional scene reconstruction seeks to create object-centric representations rather than holistic scenes from real-world videos, which is natively applicable for simulation and interaction. Conventional compositional reconstruction approaches primarily emphasize on visual appearance and show limited generalization ability to real-world scenarios. In this paper, we propose SimRecon, a framework that realizes a "Perception-Generation-Simulation" pipeline towards cluttered scene reconstruction, which first conducts scene-level semantic reconstruction from video input, then performs single-object generation, and finally assembles these assets in the simulator. However, naively combining these three stages leads to visual infidelity of generated assets and physical implausibility of the final scene, a problem particularly severe for complex scenes. Thus, we further propose two bridging modules between the three stages to address this problem. To be specific, for the transition from Perception to Generation, critical for visual fidelity, we introduce Active Viewpoint Optimization, which actively searches in 3D space to acquire optimal projected images as conditions for single-object completion. Moreover, for the transition from Generation to Simulation, essential for physical plausibility, we propose a Scene Graph Synthesizer, which guides the construction from scratch in 3D simulators, mirroring the native, constructive principle of the real world. Extensive experiments on the ScanNet dataset validate our method's superior performance over previous state-of-the-art approaches.

Learning to Price Bundles: A GCN Approach for Mixed Bundling

Sep 26, 2025Bundle pricing refers to designing several product combinations (i.e., bundles) and determining their prices in order to maximize the expected profit. It is a classic problem in revenue management and arises in many industries, such as e-commerce, tourism, and video games. However, the problem is typically intractable due to the exponential number of candidate bundles. In this paper, we explore the usage of graph convolutional networks (GCNs) in solving the bundle pricing problem. Specifically, we first develop a graph representation of the mixed bundling model (where every possible bundle is assigned with a specific price) and then train a GCN to learn the latent patterns of optimal bundles. Based on the trained GCN, we propose two inference strategies to derive high-quality feasible solutions. A local-search technique is further proposed to improve the solution quality. Numerical experiments validate the effectiveness and efficiency of our proposed GCN-based framework. Using a GCN trained on instances with 5 products, our methods consistently achieve near-optimal solutions (better than 97%) with only a fraction of computational time for problems of small to medium size. It also achieves superior solutions for larger size of problems compared with other heuristic methods such as bundle size pricing (BSP). The method can also provide high quality solutions for instances with more than 30 products even for the challenging cases where product utilities are non-additive.

Infrequent Resolving Algorithm for Online Linear Programming

Aug 02, 2024Online linear programming (OLP) has gained significant attention from both researchers and practitioners due to its extensive applications, such as online auction, network revenue management and advertising. Existing OLP algorithms fall into two categories: LP-based algorithms and LP-free algorithms. The former one typically guarantees better performance, even offering a constant regret, but requires solving a large number of LPs, which could be computationally expensive. In contrast, LP-free algorithm only requires first-order computations but induces a worse performance, lacking a constant regret bound. In this work, we bridge the gap between these two extremes by proposing an algorithm that achieves a constant regret while solving LPs only $O(\log\log T)$ times over the time horizon $T$. Moreover, when we are allowed to solve LPs only $M$ times, we propose an algorithm that can guarantee an $O\left(T^{(1/2+\epsilon)^{M-1}}\right)$ regret. Furthermore, when the arrival probabilities are known at the beginning, our algorithm can guarantee a constant regret by solving LPs $O(\log\log T)$ times, and an $O\left(T^{(1/2+\epsilon)^{M}}\right)$ regret by solving LPs only $M$ times. Numerical experiments are conducted to demonstrate the efficiency of the proposed algorithms.

ORLM: Training Large Language Models for Optimization Modeling

May 30, 2024

Large Language Models (LLMs) have emerged as powerful tools for tackling complex Operations Research (OR) problem by providing the capacity in automating optimization modeling. However, current methodologies heavily rely on prompt engineering (e.g., multi-agent cooperation) with proprietary LLMs, raising data privacy concerns that could be prohibitive in industry applications. To tackle this issue, we propose training open-source LLMs for optimization modeling. We identify four critical requirements for the training dataset of OR LLMs, design and implement OR-Instruct, a semi-automated process for creating synthetic data tailored to specific requirements. We also introduce the IndustryOR benchmark, the first industrial benchmark for testing LLMs on solving real-world OR problems. We apply the data from OR-Instruct to various open-source LLMs of 7b size (termed as ORLMs), resulting in a significantly improved capability for optimization modeling. Our best-performing ORLM achieves state-of-the-art performance on the NL4OPT, MAMO, and IndustryOR benchmarks. Our code and data are available at \url{https://github.com/Cardinal-Operations/ORLM}.

Price Interpretability of Prediction Markets: A Convergence Analysis

May 18, 2022

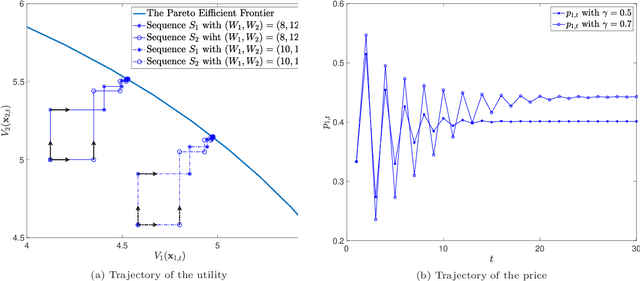

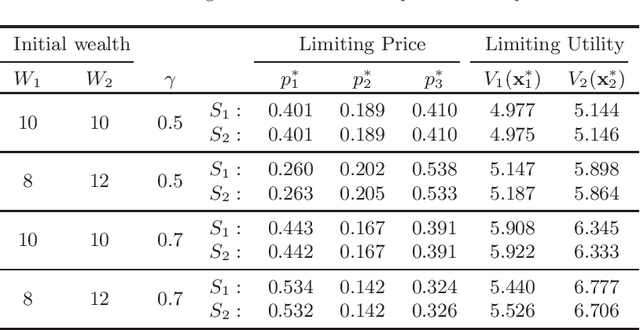

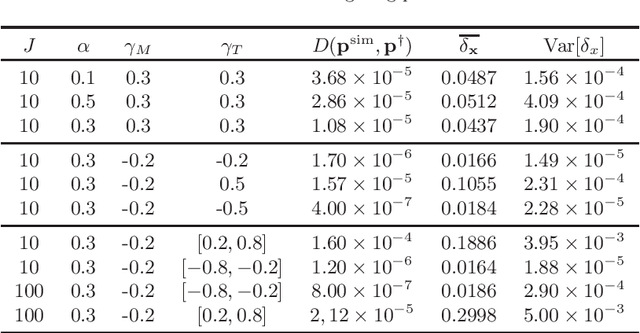

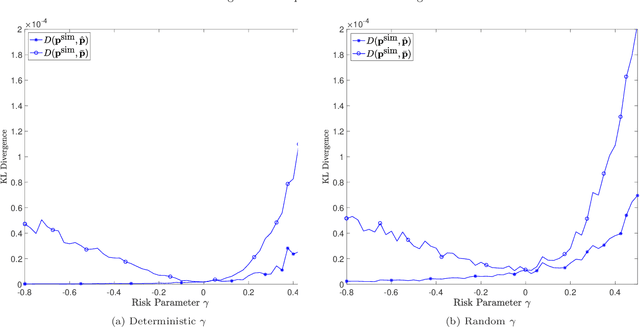

Prediction markets are long known for prediction accuracy. However, there is still a lack of systematic understanding of how prediction markets aggregate information and why they work so well. This work proposes a multivariate utility (MU)-based mechanism that unifies several existing prediction market-making schemes. Based on this mechanism, we derive convergence results for markets with myopic, risk-averse traders who repeatedly interact with the market maker. We show that the resulting limiting wealth distribution lies on the Pareto efficient frontier defined by all market participants' utilities. With the help of this result, we establish both analytical and numerical results for the limiting price for different market models. We show that the limiting price converges to the geometric mean of agents' beliefs for exponential utility-based markets. For risk measure-based markets, we construct a risk measure family that meets the convergence requirements and show that the limiting price can converge to a weighted power mean of agent beliefs. For markets based on hyperbolic absolute risk aversion (HARA) utilities, we show that the limiting price is also a risk-adjusted weighted power mean of agent beliefs, even though the trading order will affect the aggregation weights. We further propose an approximation scheme for the limiting price under the HARA utility family. We show through numerical experiments that our approximation scheme works well in predicting the convergent prices.

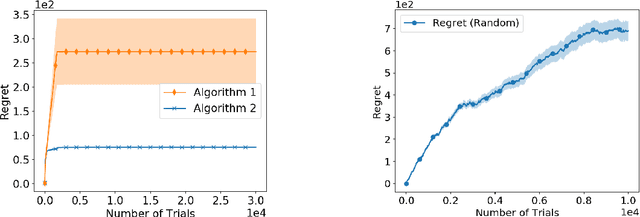

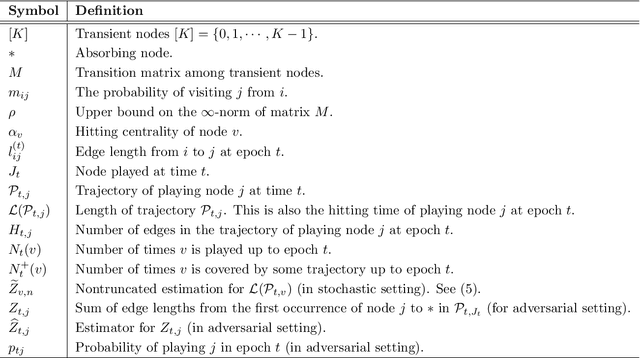

Random Walk Bandits

Nov 03, 2020

Bandit learning problems find important applications ranging from medical trials to online advertisement. In this paper, we study a novel bandit learning problem motivated by recommender systems. The goal is to recommend items so that users are likely to continue browsing. Our model views a user's browsing record as a random walk over a graph of webpages. This random walk ends (hits an absorbing node) when the user exits the website. Our model introduces a novel learning problem that calls for new technical insights on learning with graph random walk feedback. In particular, the performance and complexity depend on the structure of the decision space (represented by graphs). Our paper provides a comprehensive understanding of this new problem. We provide bandit learning algorithms for this problem with provable performance guarantees, and provide matching lower bounds.

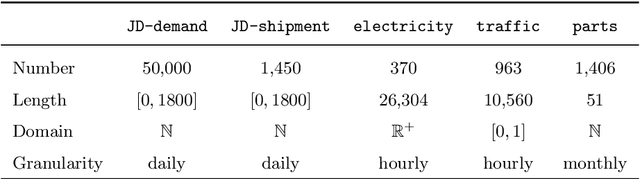

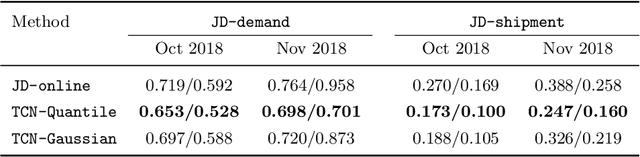

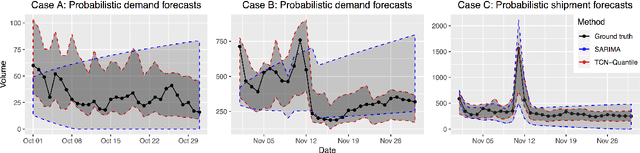

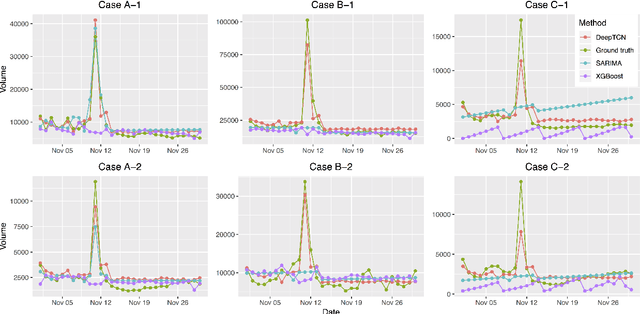

Probabilistic Forecasting with Temporal Convolutional Neural Network

Jun 11, 2019

We present a probabilistic forecasting framework based on convolutional neural network for multiple related time series forecasting. The framework can be applied to estimate probability density under both parametric and non-parametric settings. More specifically, stacked residual blocks based on dilated causal convolutional nets are constructed to capture the temporal dependencies of the series. Combined with representation learning, our approach is able to learn complex patterns such as seasonality, holiday effects within and across series, and to leverage those patterns for more accurate forecasts, especially when historical data is sparse or unavailable. Extensive empirical studies are performed on several real-world datasets, including datasets from JD.com, China's largest online retailer. The results show that our framework outperforms other state-of-the-art methods in both accuracy and efficiency.

A Near-Optimal Dynamic Learning Algorithm for Online Matching Problems with Concave Returns

Jun 06, 2015

We consider an online matching problem with concave returns. This problem is a significant generalization of the Adwords allocation problem and has vast applications in online advertising. In this problem, a sequence of items arrive sequentially and each has to be allocated to one of the bidders, who bid a certain value for each item. At each time, the decision maker has to allocate the current item to one of the bidders without knowing the future bids and the objective is to maximize the sum of some concave functions of each bidder's aggregate value. In this work, we propose an algorithm that achieves near-optimal performance for this problem when the bids arrive in a random order and the input data satisfies certain conditions. The key idea of our algorithm is to learn the input data pattern dynamically: we solve a sequence of carefully chosen partial allocation problems and use their optimal solutions to assist with the future decision. Our analysis belongs to the primal-dual paradigm, however, the absence of linearity of the objective function and the dynamic feature of the algorithm makes our analysis quite unique.

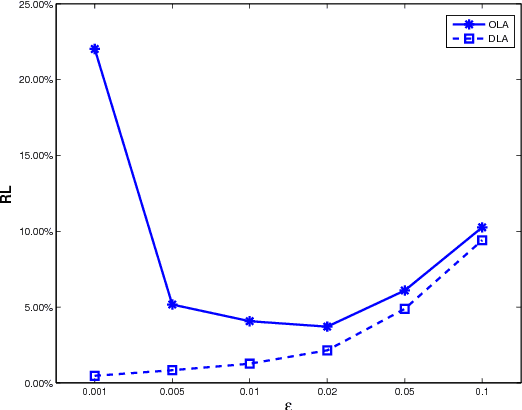

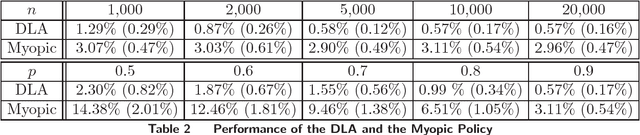

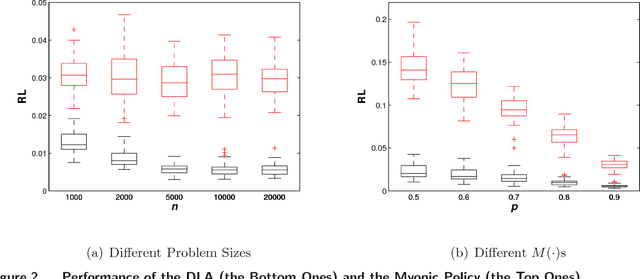

A Dynamic Near-Optimal Algorithm for Online Linear Programming

Apr 09, 2014A natural optimization model that formulates many online resource allocation and revenue management problems is the online linear program (LP) in which the constraint matrix is revealed column by column along with the corresponding objective coefficient. In such a model, a decision variable has to be set each time a column is revealed without observing the future inputs and the goal is to maximize the overall objective function. In this paper, we provide a near-optimal algorithm for this general class of online problems under the assumption of random order of arrival and some mild conditions on the size of the LP right-hand-side input. Specifically, our learning-based algorithm works by dynamically updating a threshold price vector at geometric time intervals, where the dual prices learned from the revealed columns in the previous period are used to determine the sequential decisions in the current period. Due to the feature of dynamic learning, the competitiveness of our algorithm improves over the past study of the same problem. We also present a worst-case example showing that the performance of our algorithm is near-optimal.