Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeClose the Gaps: A Learning-while-Doing Algorithm for a Class of Single-Product Revenue Management Problems

Paper and Code

Jun 27, 2013

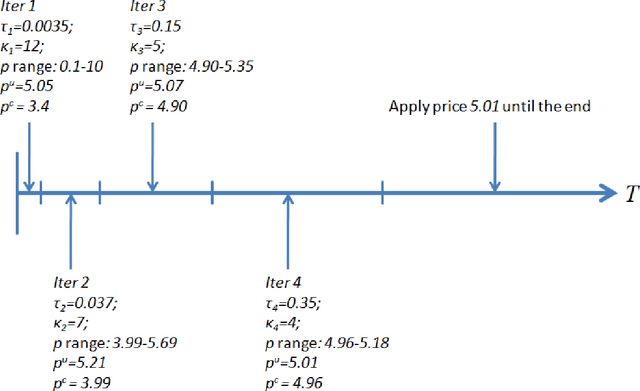

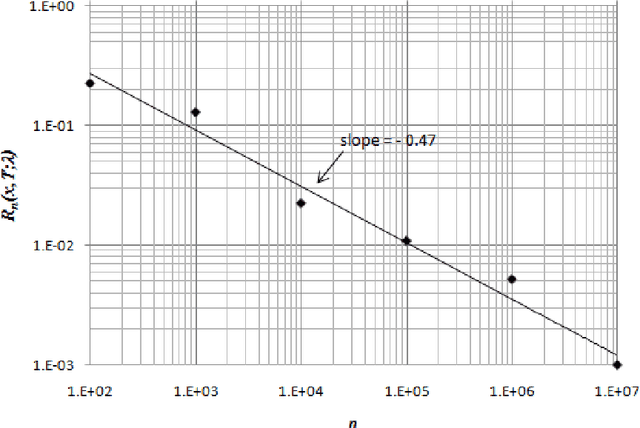

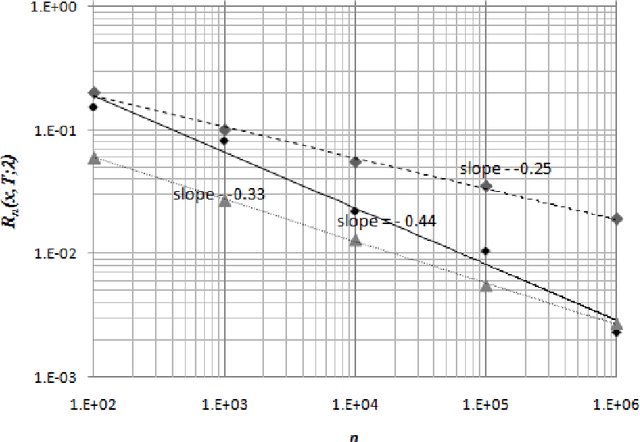

We consider a retailer selling a single product with limited on-hand inventory over a finite selling season. Customer demand arrives according to a Poisson process, the rate of which is influenced by a single action taken by the retailer (such as price adjustment, sales commission, advertisement intensity, etc.). The relationship between the action and the demand rate is not known in advance. However, the retailer is able to learn the optimal action "on the fly" as she maximizes her total expected revenue based on the observed demand reactions. Using the pricing problem as an example, we propose a dynamic "learning-while-doing" algorithm that only involves function value estimation to achieve a near-optimal performance. Our algorithm employs a series of shrinking price intervals and iteratively tests prices within that interval using a set of carefully chosen parameters. We prove that the convergence rate of our algorithm is among the fastest of all possible algorithms in terms of asymptotic "regret" (the relative loss comparing to the full information optimal solution). Our result closes the performance gaps between parametric and non-parametric learning and between a post-price mechanism and a customer-bidding mechanism. Important managerial insight from this research is that the values of information on both the parametric form of the demand function as well as each customer's exact reservation price are less important than prior literature suggests. Our results also suggest that firms would be better off to perform dynamic learning and action concurrently rather than sequentially.