Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTransactionGPT

Nov 12, 2025We present TransactionGPT (TGPT), a foundation model for consumer transaction data within one of world's largest payment networks. TGPT is designed to understand and generate transaction trajectories while simultaneously supporting a variety of downstream prediction and classification tasks. We introduce a novel 3D-Transformer architecture specifically tailored for capturing the complex dynamics in payment transaction data. This architecture incorporates design innovations that enhance modality fusion and computational efficiency, while seamlessly enabling joint optimization with downstream objectives. Trained on billion-scale real-world transactions, TGPT significantly improves downstream classification performance against a competitive production model and exhibits advantages over baselines in generating future transactions. We conduct extensive empirical evaluations utilizing a diverse collection of company transaction datasets spanning multiple downstream tasks, thereby enabling a thorough assessment of TGPT's effectiveness and efficiency in comparison to established methodologies. Furthermore, we examine the incorporation of LLM-derived embeddings within TGPT and benchmark its performance against fine-tuned LLMs, demonstrating that TGPT achieves superior predictive accuracy as well as faster training and inference. We anticipate that the architectural innovations and practical guidelines from this work will advance foundation models for transaction-like data and catalyze future research in this emerging field.

NdLinear Is All You Need for Representation Learning

Mar 21, 2025Many high-impact machine learning tasks involve multi-dimensional data (e.g., images, volumetric medical scans, multivariate time-series). Yet, most neural architectures flatten inputs, discarding critical cross-dimension information. We introduce NdLinear, a novel linear transformation that preserves these structures without extra overhead. By operating separately along each dimension, NdLinear captures dependencies that standard fully connected layers overlook. Extensive experiments across convolutional, recurrent, and transformer-based networks show significant improvements in representational power and parameter efficiency. Crucially, NdLinear serves as a foundational building block for large-scale foundation models by operating on any unimodal or multimodal data in its native form. This removes the need for flattening or modality-specific preprocessing. Ndlinear rethinks core architectural priorities beyond attention, enabling more expressive, context-aware models at scale. We propose NdLinear as a drop-in replacement for standard linear layers -- marking an important step toward next-generation neural architectures.

Towards Efficient Large Scale Spatial-Temporal Time Series Forecasting via Improved Inverted Transformers

Mar 13, 2025

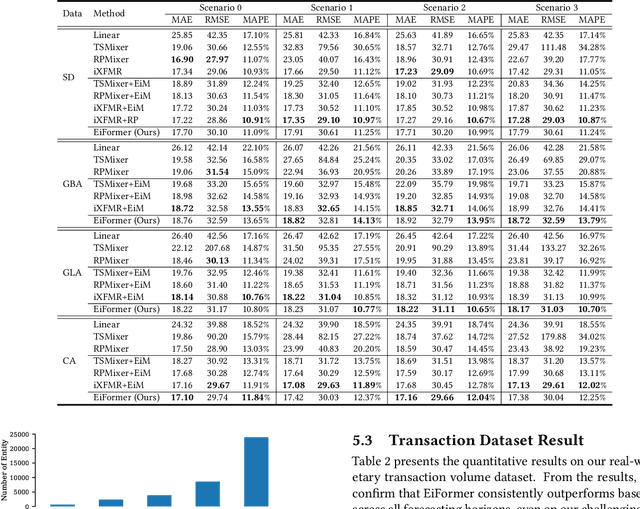

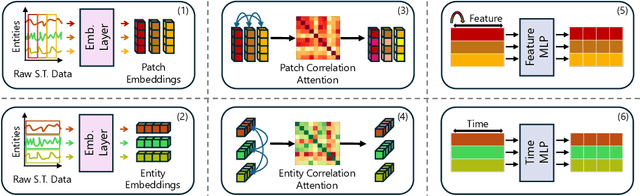

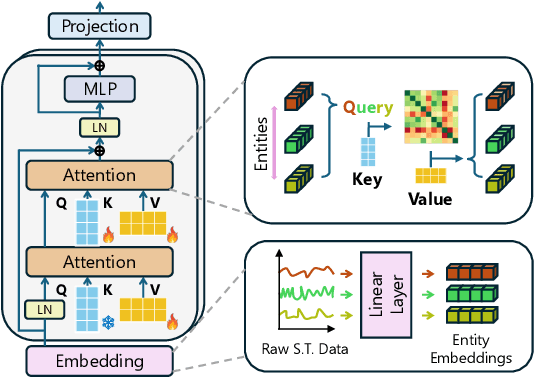

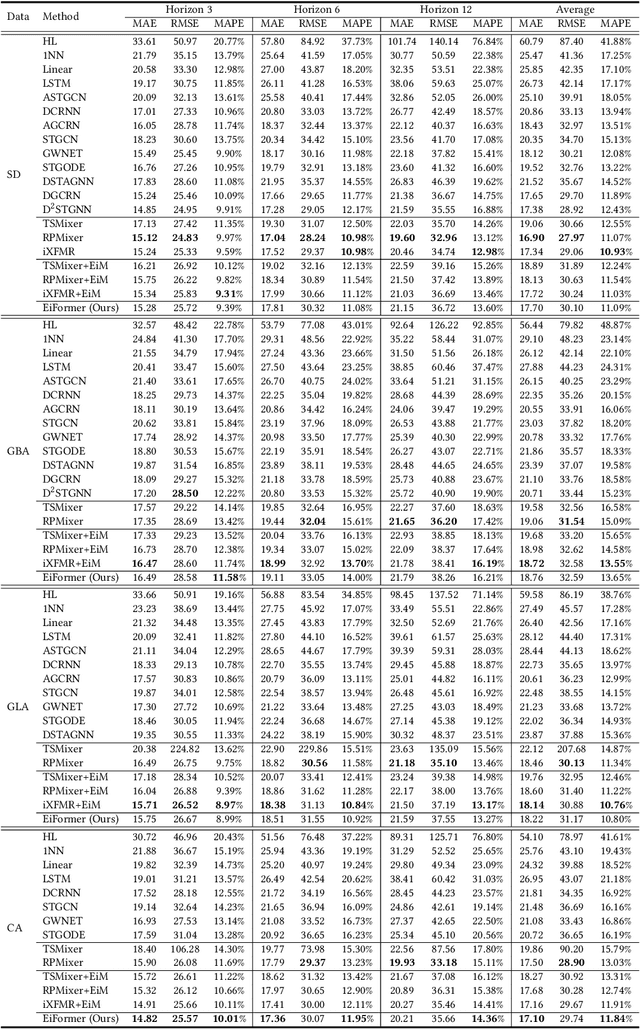

Time series forecasting at scale presents significant challenges for modern prediction systems, particularly when dealing with large sets of synchronized series, such as in a global payment network. In such systems, three key challenges must be overcome for accurate and scalable predictions: 1) emergence of new entities, 2) disappearance of existing entities, and 3) the large number of entities present in the data. The recently proposed Inverted Transformer (iTransformer) architecture has shown promising results by effectively handling variable entities. However, its practical application in large-scale settings is limited by quadratic time and space complexity ($O(N^2)$) with respect to the number of entities $N$. In this paper, we introduce EiFormer, an improved inverted transformer architecture that maintains the adaptive capabilities of iTransformer while reducing computational complexity to linear scale ($O(N)$). Our key innovation lies in restructuring the attention mechanism to eliminate redundant computations without sacrificing model expressiveness. Additionally, we incorporate a random projection mechanism that not only enhances efficiency but also improves prediction accuracy through better feature representation. Extensive experiments on the public LargeST benchmark dataset and a proprietary large-scale time series dataset demonstrate that EiFormer significantly outperforms existing methods in both computational efficiency and forecasting accuracy. Our approach enables practical deployment of transformer-based forecasting in industrial applications where handling time series at scale is essential.

A Compact Model for Large-Scale Time Series Forecasting

Feb 28, 2025

Spatio-temporal data, which commonly arise in real-world applications such as traffic monitoring, financial transactions, and ride-share demands, represent a special category of multivariate time series. They exhibit two distinct characteristics: high dimensionality and commensurability across spatial locations. These attributes call for computationally efficient modeling approaches and facilitate the use of univariate forecasting models in a channel-independent fashion. SparseTSF, a recently introduced competitive univariate forecasting model, harnesses periodicity to achieve compactness by concentrating on cross-period dynamics, thereby extending the Pareto frontier with respect to model size and predictive performance. Nonetheless, it underperforms on spatio-temporal data due to an inadequate capture of intra-period temporal dependencies. To address this shortcoming, we propose UltraSTF, which integrates a cross-period forecasting module with an ultra-compact shape bank component. Our model effectively detects recurring patterns in time series through the attention mechanism of the shape bank component, thereby strengthening its ability to learn intra-period dynamics. UltraSTF achieves state-of-the-art performance on the LargeST benchmark while employing fewer than 0.2% of the parameters required by the second-best approaches, thus further extending the Pareto frontier of existing methods.

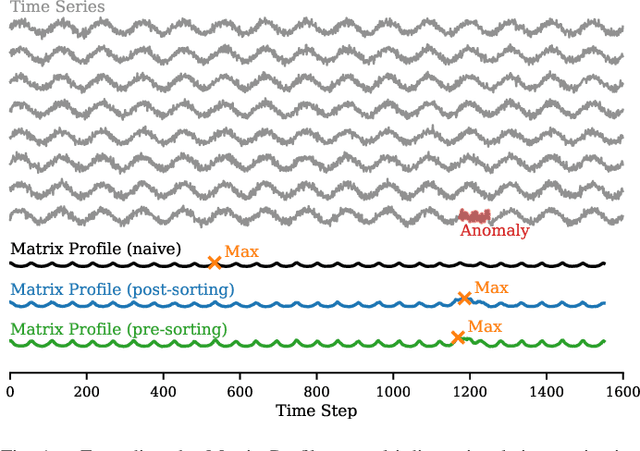

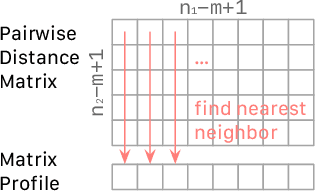

Matrix Profile for Anomaly Detection on Multidimensional Time Series

Sep 14, 2024

The Matrix Profile (MP), a versatile tool for time series data mining, has been shown effective in time series anomaly detection (TSAD). This paper delves into the problem of anomaly detection in multidimensional time series, a common occurrence in real-world applications. For instance, in a manufacturing factory, multiple sensors installed across the site collect time-varying data for analysis. The Matrix Profile, named for its role in profiling the matrix storing pairwise distance between subsequences of univariate time series, becomes complex in multidimensional scenarios. If the input univariate time series has n subsequences, the pairwise distance matrix is a n x n matrix. In a multidimensional time series with d dimensions, the pairwise distance information must be stored in a n x n x d tensor. In this paper, we first analyze different strategies for condensing this tensor into a profile vector. We then investigate the potential of extending the MP to efficiently find k-nearest neighbors for anomaly detection. Finally, we benchmark the multidimensional MP against 19 baseline methods on 119 multidimensional TSAD datasets. The experiments covers three learning setups: unsupervised, supervised, and semi-supervised. MP is the only method that consistently delivers high performance across all setups.

Preserving Individuality while Following the Crowd: Understanding the Role of User Taste and Crowd Wisdom in Online Product Rating Prediction

Sep 06, 2024

Numerous algorithms have been developed for online product rating prediction, but the specific influence of user and product information in determining the final prediction score remains largely unexplored. Existing research often relies on narrowly defined data settings, which overlooks real-world challenges such as the cold-start problem, cross-category information utilization, and scalability and deployment issues. To delve deeper into these aspects, and particularly to uncover the roles of individual user taste and collective wisdom, we propose a unique and practical approach that emphasizes historical ratings at both the user and product levels, encapsulated using a continuously updated dynamic tree representation. This representation effectively captures the temporal dynamics of users and products, leverages user information across product categories, and provides a natural solution to the cold-start problem. Furthermore, we have developed an efficient data processing strategy that makes this approach highly scalable and easily deployable. Comprehensive experiments in real industry settings demonstrate the effectiveness of our approach. Notably, our findings reveal that individual taste dominates over collective wisdom in online product rating prediction, a perspective that contrasts with the commonly observed wisdom of the crowd phenomenon in other domains. This dominance of individual user taste is consistent across various model types, including the boosting tree model, recurrent neural network (RNN), and transformer-based architectures. This observation holds true across the overall population, within individual product categories, and in cold-start scenarios. Our findings underscore the significance of individual user tastes in the context of online product rating prediction and the robustness of our approach across different model architectures.

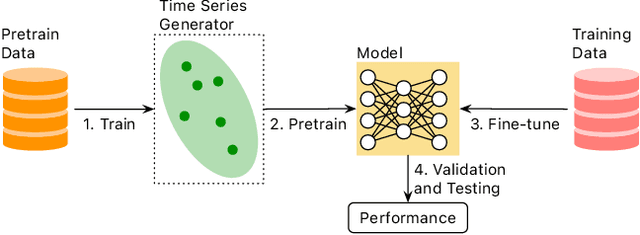

A Systematic Evaluation of Generated Time Series and Their Effects in Self-Supervised Pretraining

Aug 15, 2024

Self-supervised Pretrained Models (PTMs) have demonstrated remarkable performance in computer vision and natural language processing tasks. These successes have prompted researchers to design PTMs for time series data. In our experiments, most self-supervised time series PTMs were surpassed by simple supervised models. We hypothesize this undesired phenomenon may be caused by data scarcity. In response, we test six time series generation methods, use the generated data in pretraining in lieu of the real data, and examine the effects on classification performance. Our results indicate that replacing a real-data pretraining set with a greater volume of only generated samples produces noticeable improvement.

Random Projection Layers for Multidimensional Time Series Forecasting

Feb 29, 2024

All-Multi-Layer Perceptron (all-MLP) mixer models have been shown to be effective for time series forecasting problems. However, when such a model is applied to high-dimensional time series (e.g., the time series in a spatial-temporal dataset), its performance is likely to degrade due to overfitting issues. In this paper, we propose an all-MLP time series forecasting architecture, referred to as RPMixer. Our method leverages the ensemble-like behavior of deep neural networks, where each individual block within the network acts like a base learner in an ensemble model, especially when identity mapping residual connections are incorporated. By integrating random projection layers into our model, we increase the diversity among the blocks' outputs, thereby enhancing the overall performance of RPMixer. Extensive experiments conducted on large-scale spatial-temporal forecasting benchmark datasets demonstrate that our proposed method outperforms alternative methods, including both spatial-temporal graph models and general forecasting models.

PUPAE: Intuitive and Actionable Explanations for Time Series Anomalies

Jan 16, 2024

In recent years there has been significant progress in time series anomaly detection. However, after detecting an (perhaps tentative) anomaly, can we explain it? Such explanations would be useful to triage anomalies. For example, in an oil refinery, should we respond to an anomaly by dispatching a hydraulic engineer, or an intern to replace the battery on a sensor? There have been some parallel efforts to explain anomalies, however many proposed techniques produce explanations that are indirect, and often seem more complex than the anomaly they seek to explain. Our review of the literature/checklists/user-manuals used by frontline practitioners in various domains reveals an interesting near-universal commonality. Most practitioners discuss, explain and report anomalies in the following format: The anomaly would be like normal data A, if not for the corruption B. The reader will appreciate that is a type of counterfactual explanation. In this work we introduce a domain agnostic counterfactual explanation technique to produce explanations for time series anomalies. As we will show, our method can produce both visual and text-based explanations that are objectively correct, intuitive and in many circumstances, directly actionable.

* 9 Page Manuscript, 1 Page Supplementary (Supplement not published in conference proceedings.)

Has Your Pretrained Model Improved? A Multi-head Posterior Based Approach

Jan 15, 2024

The emergence of pretrained models has significantly impacted Natural Language Processing (NLP) and Computer Vision to relational datasets. Traditionally, these models are assessed through fine-tuned downstream tasks. However, this raises the question of how to evaluate these models more efficiently and more effectively. In this study, we explore a novel approach where we leverage the meta features associated with each entity as a source of worldly knowledge and employ entity representations from the models. We propose using the consistency between these representations and the meta features as a metric for evaluating pretrained models. Our method's effectiveness is demonstrated across various domains, including models with relational datasets, large language models and image models.