Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGaia: Graph Neural Network with Temporal Shift aware Attention for Gross Merchandise Value Forecast in E-commerce

Jul 27, 2022

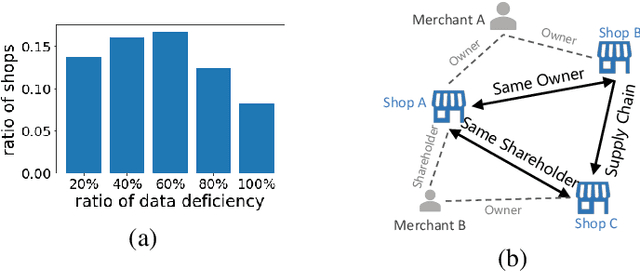

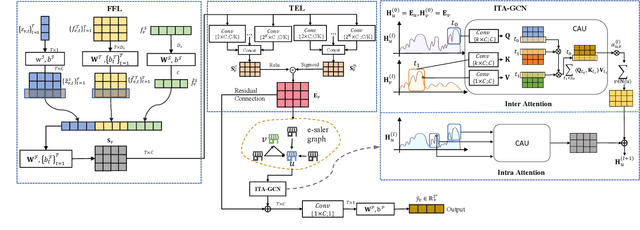

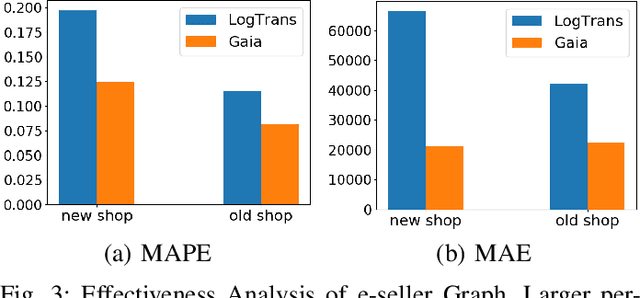

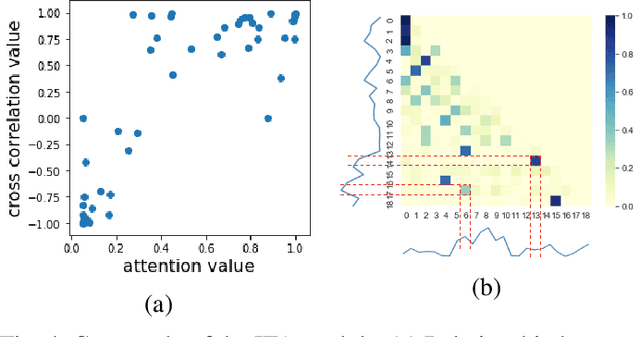

E-commerce has gone a long way in empowering merchants through the internet. In order to store the goods efficiently and arrange the marketing resource properly, it is important for them to make the accurate gross merchandise value (GMV) prediction. However, it's nontrivial to make accurate prediction with the deficiency of digitized data. In this article, we present a solution to better forecast GMV inside Alipay app. Thanks to graph neural networks (GNN) which has great ability to correlate different entities to enrich information, we propose Gaia, a graph neural network (GNN) model with temporal shift aware attention. Gaia leverages the relevant e-seller' sales information and learn neighbor correlation based on temporal dependencies. By testing on Alipay's real dataset and comparing with other baselines, Gaia has shown the best performance. And Gaia is deployed in the simulated online environment, which also achieves great improvement compared with baselines.

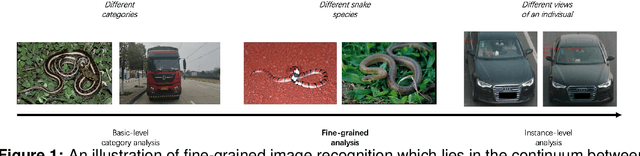

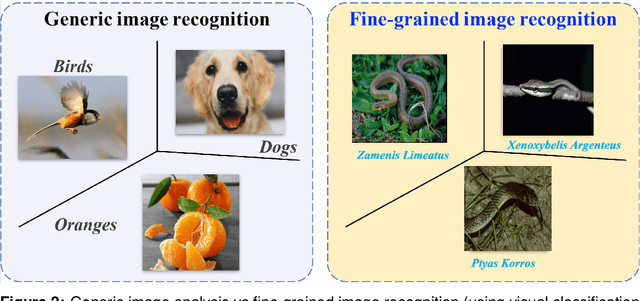

Explored An Effective Methodology for Fine-Grained Snake Recognition

Jul 24, 2022

Fine-Grained Visual Classification (FGVC) is a longstanding and fundamental problem in computer vision and pattern recognition, and underpins a diverse set of real-world applications. This paper describes our contribution at SnakeCLEF2022 with FGVC. Firstly, we design a strong multimodal backbone to utilize various meta-information to assist in fine-grained identification. Secondly, we provide new loss functions to solve the long tail distribution with dataset. Then, in order to take full advantage of unlabeled datasets, we use self-supervised learning and supervised learning joint training to provide pre-trained model. Moreover, some effective data process tricks also are considered in our experiments. Last but not least, fine-tuned in downstream task with hard mining, ensambled kinds of model performance. Extensive experiments demonstrate that our method can effectively improve the performance of fine-grained recognition. Our method can achieve a macro f1 score 92.7% and 89.4% on private and public dataset, respectively, which is the 1st place among the participators on private leaderboard.

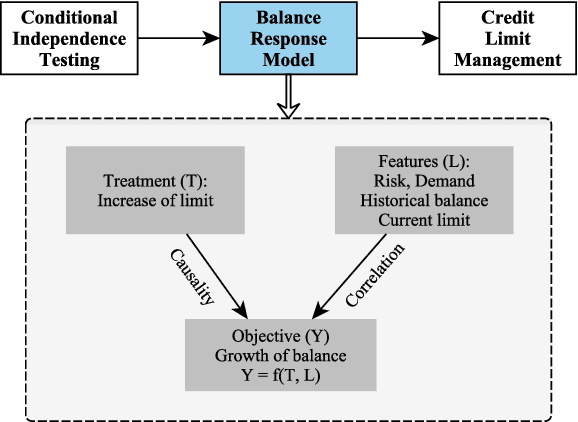

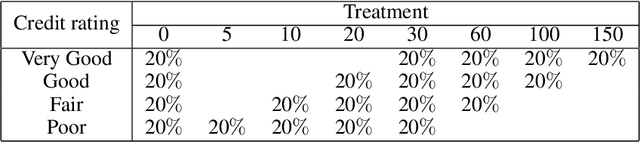

Intelligent Credit Limit Management in Consumer Loans Based on Causal Inference

Jul 10, 2020

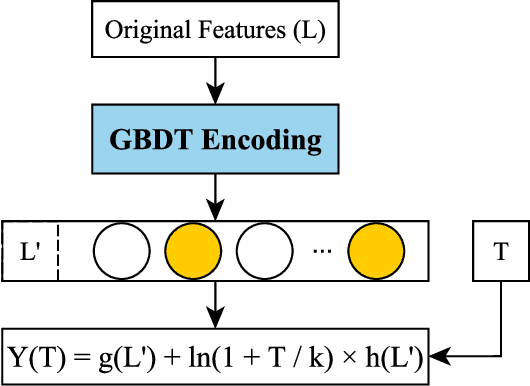

Nowadays consumer loan plays an important role in promoting the economic growth, and credit cards are the most popular consumer loan. One of the most essential parts in credit cards is the credit limit management. Traditionally, credit limits are adjusted based on limited heuristic strategies, which are developed by experienced professionals. In this paper, we present a data-driven approach to manage the credit limit intelligently. Firstly, a conditional independence testing is conducted to acquire the data for building models. Based on these testing data, a response model is then built to measure the heterogeneous treatment effect of increasing credit limits (i.e. treatments) for different customers, who are depicted by several control variables (i.e. features). In order to incorporate the diminishing marginal effect, a carefully selected log transformation is introduced to the treatment variable. Moreover, the model's capability can be further enhanced by applying a non-linear transformation on features via GBDT encoding. Finally, a well-designed metric is proposed to properly measure the performances of compared methods. The experimental results demonstrate the effectiveness of the proposed approach.

Large-scale Uncertainty Estimation and Its Application in Revenue Forecast of SMEs

May 02, 2020

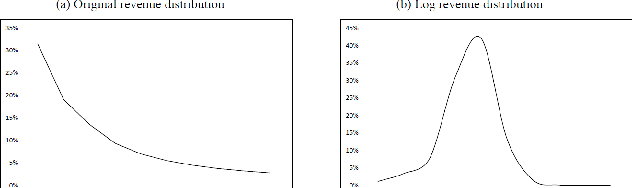

The economic and banking importance of the small and medium enterprise (SME) sector is well recognized in contemporary society. Business credit loans are very important for the operation of SMEs, and the revenue is a key indicator of credit limit management. Therefore, it is very beneficial to construct a reliable revenue forecasting model. If the uncertainty of an enterprise's revenue forecasting can be estimated, a more proper credit limit can be granted. Natural gradient boosting approach, which estimates the uncertainty of prediction by a multi-parameter boosting algorithm based on the natural gradient. However, its original implementation is not easy to scale into big data scenarios, and computationally expensive compared to state-of-the-art tree-based models (such as XGBoost). In this paper, we propose a Scalable Natural Gradient Boosting Machines that is simple to implement, readily parallelizable, interpretable and yields high-quality predictive uncertainty estimates. According to the characteristics of revenue distribution, we derive an uncertainty quantification function. We demonstrate that our method can distinguish between samples that are accurate and inaccurate on revenue forecasting of SMEs. What's more, interpretability can be naturally obtained from the model, satisfying the financial needs.

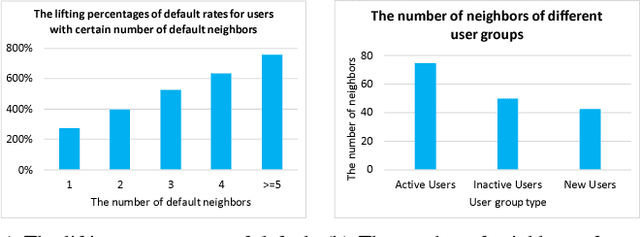

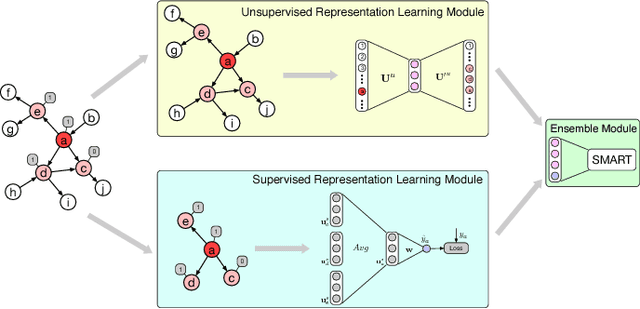

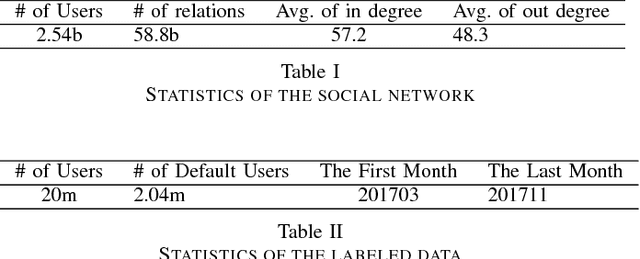

NetDP: An Industrial-Scale Distributed Network Representation Framework for Default Prediction in Ant Credit Pay

Apr 01, 2020

Ant Credit Pay is a consumer credit service in Ant Financial Service Group. Similar to credit card, loan default is one of the major risks of this credit product. Hence, effective algorithm for default prediction is the key to losses reduction and profits increment for the company. However, the challenges facing in our scenario are different from those in conventional credit card service. The first one is scalability. The huge volume of users and their behaviors in Ant Financial requires the ability to process industrial-scale data and perform model training efficiently. The second challenges is the cold-start problem. Different from the manual review for credit card application in conventional banks, the credit limit of Ant Credit Pay is automatically offered to users based on the knowledge learned from big data. However, default prediction for new users is suffered from lack of enough credit behaviors. It requires that the proposal should leverage other new data source to alleviate the cold-start problem. Considering the above challenges and the special scenario in Ant Financial, we try to incorporate default prediction with network information to alleviate the cold-start problem. In this paper, we propose an industrial-scale distributed network representation framework, termed NetDP, for default prediction in Ant Credit Pay. The proposal explores network information generated by various interaction between users, and blends unsupervised and supervised network representation in a unified framework for default prediction problem. Moreover, we present a parameter-server-based distributed implement of our proposal to handle the scalability challenge. Experimental results demonstrate the effectiveness of our proposal, especially in cold-start problem, as well as the efficiency for industrial-scale dataset.

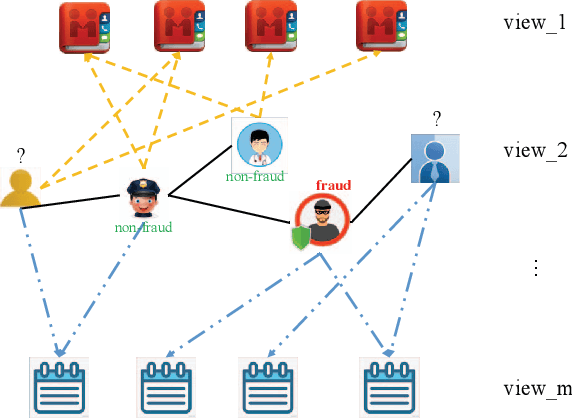

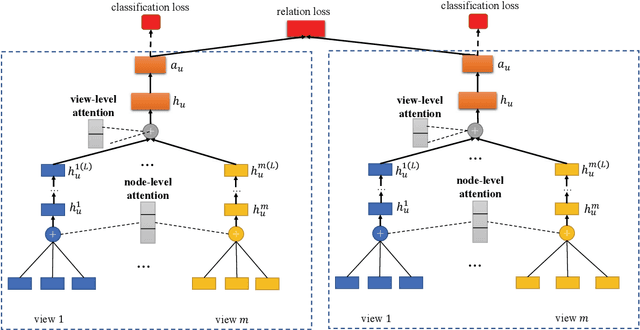

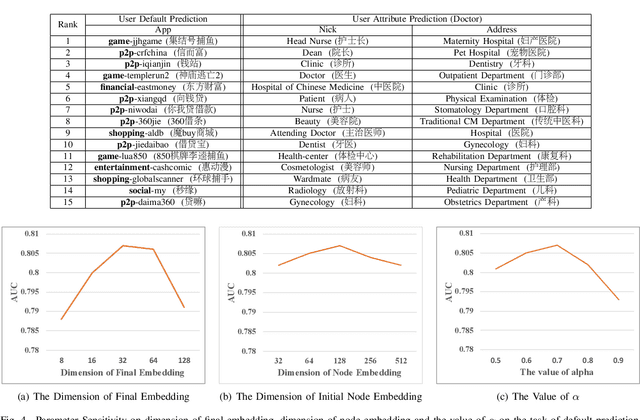

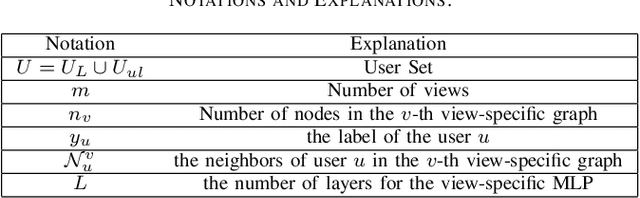

A Semi-supervised Graph Attentive Network for Financial Fraud Detection

Feb 28, 2020

With the rapid growth of financial services, fraud detection has been a very important problem to guarantee a healthy environment for both users and providers. Conventional solutions for fraud detection mainly use some rule-based methods or distract some features manually to perform prediction. However, in financial services, users have rich interactions and they themselves always show multifaceted information. These data form a large multiview network, which is not fully exploited by conventional methods. Additionally, among the network, only very few of the users are labelled, which also poses a great challenge for only utilizing labeled data to achieve a satisfied performance on fraud detection. To address the problem, we expand the labeled data through their social relations to get the unlabeled data and propose a semi-supervised attentive graph neural network, namedSemiGNN to utilize the multi-view labeled and unlabeled data for fraud detection. Moreover, we propose a hierarchical attention mechanism to better correlate different neighbors and different views. Simultaneously, the attention mechanism can make the model interpretable and tell what are the important factors for the fraud and why the users are predicted as fraud. Experimentally, we conduct the prediction task on the users of Alipay, one of the largest third-party online and offline cashless payment platform serving more than 4 hundreds of million users in China. By utilizing the social relations and the user attributes, our method can achieve a better accuracy compared with the state-of-the-art methods on two tasks. Moreover, the interpretable results also give interesting intuitions regarding the tasks.