Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNetDP: An Industrial-Scale Distributed Network Representation Framework for Default Prediction in Ant Credit Pay

Apr 01, 2020

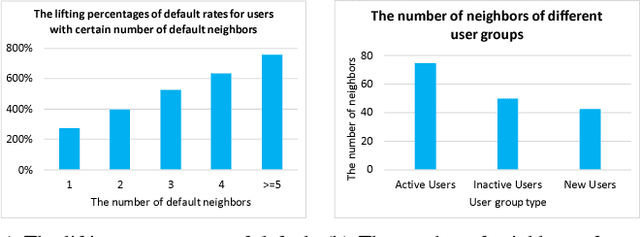

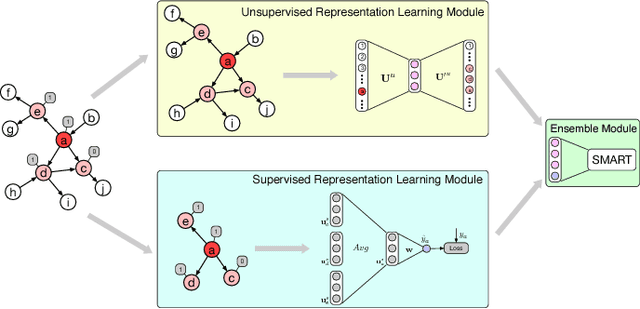

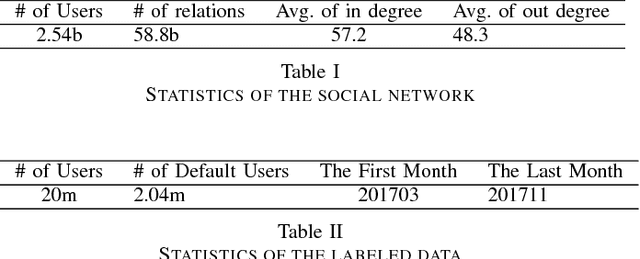

Ant Credit Pay is a consumer credit service in Ant Financial Service Group. Similar to credit card, loan default is one of the major risks of this credit product. Hence, effective algorithm for default prediction is the key to losses reduction and profits increment for the company. However, the challenges facing in our scenario are different from those in conventional credit card service. The first one is scalability. The huge volume of users and their behaviors in Ant Financial requires the ability to process industrial-scale data and perform model training efficiently. The second challenges is the cold-start problem. Different from the manual review for credit card application in conventional banks, the credit limit of Ant Credit Pay is automatically offered to users based on the knowledge learned from big data. However, default prediction for new users is suffered from lack of enough credit behaviors. It requires that the proposal should leverage other new data source to alleviate the cold-start problem. Considering the above challenges and the special scenario in Ant Financial, we try to incorporate default prediction with network information to alleviate the cold-start problem. In this paper, we propose an industrial-scale distributed network representation framework, termed NetDP, for default prediction in Ant Credit Pay. The proposal explores network information generated by various interaction between users, and blends unsupervised and supervised network representation in a unified framework for default prediction problem. Moreover, we present a parameter-server-based distributed implement of our proposal to handle the scalability challenge. Experimental results demonstrate the effectiveness of our proposal, especially in cold-start problem, as well as the efficiency for industrial-scale dataset.