Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGRAND: Graph Neural Diffusion

Jun 21, 2021

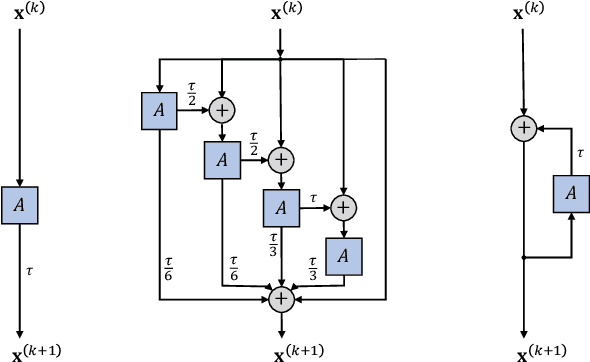

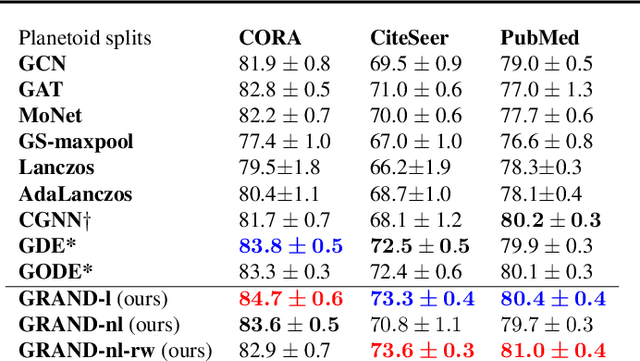

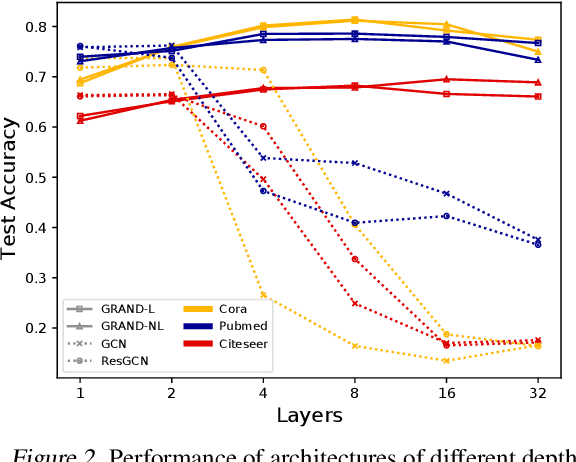

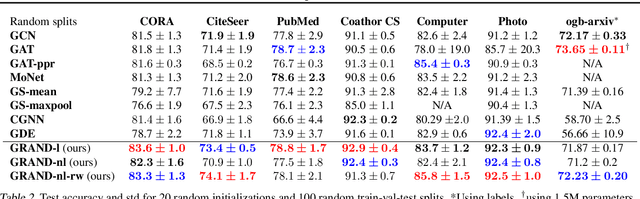

We present Graph Neural Diffusion (GRAND) that approaches deep learning on graphs as a continuous diffusion process and treats Graph Neural Networks (GNNs) as discretisations of an underlying PDE. In our model, the layer structure and topology correspond to the discretisation choices of temporal and spatial operators. Our approach allows a principled development of a broad new class of GNNs that are able to address the common plights of graph learning models such as depth, oversmoothing, and bottlenecks. Key to the success of our models are stability with respect to perturbations in the data and this is addressed for both implicit and explicit discretisation schemes. We develop linear and nonlinear versions of GRAND, which achieve competitive results on many standard graph benchmarks.

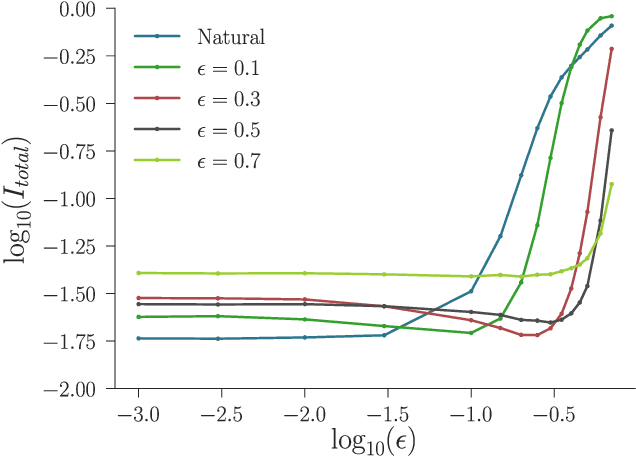

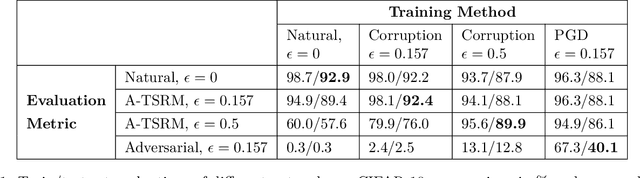

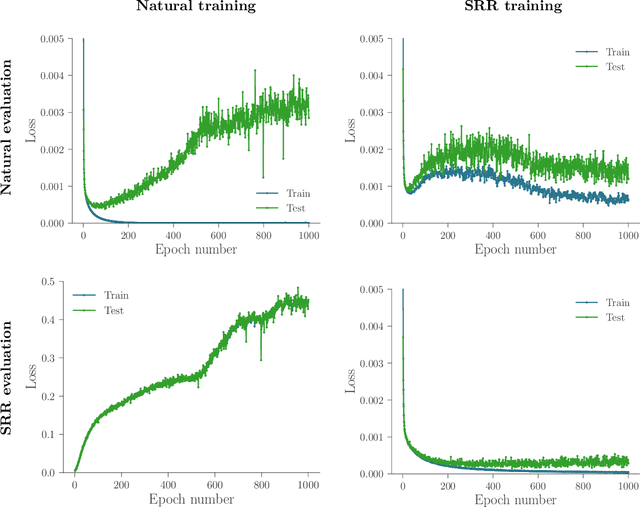

Statistically Robust Neural Network Classification

Dec 11, 2019

Recently there has been much interest in quantifying the robustness of neural network classifiers through adversarial risk metrics. However, for problems where test-time corruptions occur in a probabilistic manner, rather than being generated by an explicit adversary, adversarial metrics typically do not provide an accurate or reliable indicator of robustness. To address this, we introduce a statistically robust risk (SRR) framework which measures robustness in expectation over both network inputs and a corruption distribution. Unlike many adversarial risk metrics, which typically require separate applications on a point-by-point basis, the SRR can easily be directly estimated for an entire network and used as a training objective in a stochastic gradient scheme. Furthermore, we show both theoretically and empirically that it can scale to higher-dimensional networks by providing superior generalization performance compared with comparable adversarial risks.

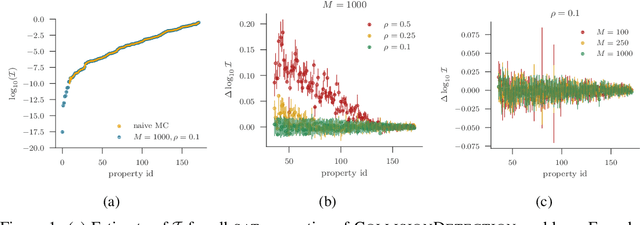

A Statistical Approach to Assessing Neural Network Robustness

Nov 29, 2018

We present a new approach to assessing the robustness of neural networks based on estimating the proportion of inputs for which a property is violated. Specifically, we estimate the probability of the event that the property is violated under an input model. Our approach critically varies from the formal verification framework in that when the property can be violated, it provides an informative notion of how robust the network is, rather than just the conventional assertion that the network is not verifiable. Furthermore, it provides an ability to scale to larger networks than formal verification approaches. Though the framework still provides a formal guarantee of satisfiability whenever it successfully finds one or more violations, these advantages do come at the cost of only providing a statistical estimate of unsatisfiability whenever no violation is found. Key to the practical success of our approach is an adaptation of multi-level splitting, a Monte Carlo approach for estimating the probability of rare events, to our statistical robustness framework. We demonstrate that our approach is able to emulate formal verification procedures on benchmark problems, while scaling to larger networks and providing reliable additional information in the form of accurate estimates of the violation probability.

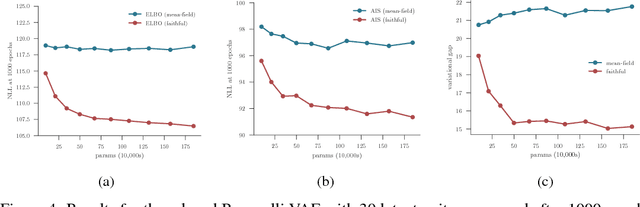

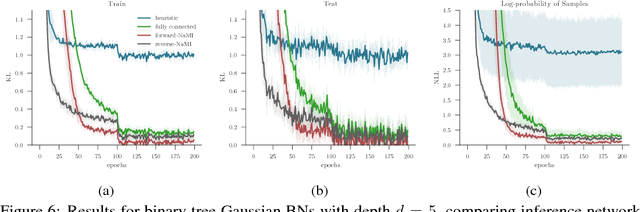

Faithful Inversion of Generative Models for Effective Amortized Inference

Oct 24, 2018

Inference amortization methods share information across multiple posterior-inference problems, allowing each to be carried out more efficiently. Generally, they require the inversion of the dependency structure in the generative model, as the modeller must learn a mapping from observations to distributions approximating the posterior. Previous approaches have involved inverting the dependency structure in a heuristic way that fails to capture these dependencies correctly, thereby limiting the achievable accuracy of the resulting approximations. We introduce an algorithm for faithfully, and minimally, inverting the graphical model structure of any generative model. Such inverses have two crucial properties: (a) they do not encode any independence assertions that are absent from the model and; (b) they are local maxima for the number of true independencies encoded. We prove the correctness of our approach and empirically show that the resulting minimally faithful inverses lead to better inference amortization than existing heuristic approaches.

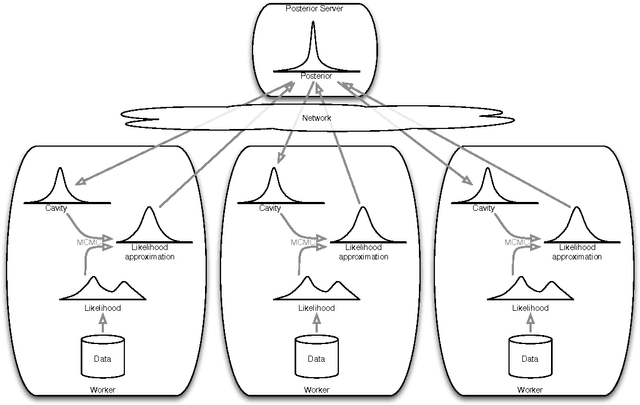

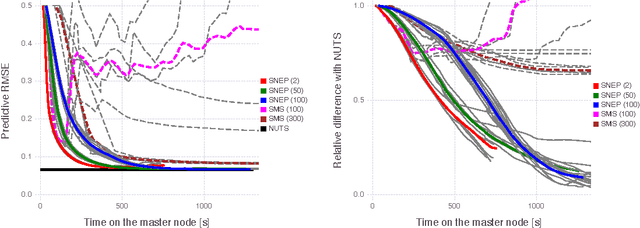

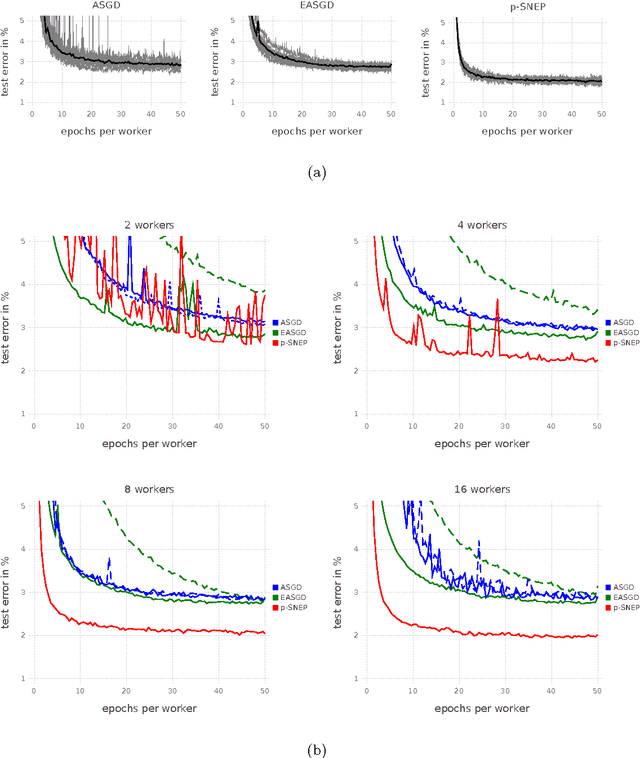

Distributed Bayesian Learning with Stochastic Natural-gradient Expectation Propagation and the Posterior Server

Sep 07, 2017

This paper makes two contributions to Bayesian machine learning algorithms. Firstly, we propose stochastic natural gradient expectation propagation (SNEP), a novel alternative to expectation propagation (EP), a popular variational inference algorithm. SNEP is a black box variational algorithm, in that it does not require any simplifying assumptions on the distribution of interest, beyond the existence of some Monte Carlo sampler for estimating the moments of the EP tilted distributions. Further, as opposed to EP which has no guarantee of convergence, SNEP can be shown to be convergent, even when using Monte Carlo moment estimates. Secondly, we propose a novel architecture for distributed Bayesian learning which we call the posterior server. The posterior server allows scalable and robust Bayesian learning in cases where a data set is stored in a distributed manner across a cluster, with each compute node containing a disjoint subset of data. An independent Monte Carlo sampler is run on each compute node, with direct access only to the local data subset, but which targets an approximation to the global posterior distribution given all data across the whole cluster. This is achieved by using a distributed asynchronous implementation of SNEP to pass messages across the cluster. We demonstrate SNEP and the posterior server on distributed Bayesian learning of logistic regression and neural networks. Keywords: Distributed Learning, Large Scale Learning, Deep Learning, Bayesian Learn- ing, Variational Inference, Expectation Propagation, Stochastic Approximation, Natural Gradient, Markov chain Monte Carlo, Parameter Server, Posterior Server.

* 37 pages, 7 figures