Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

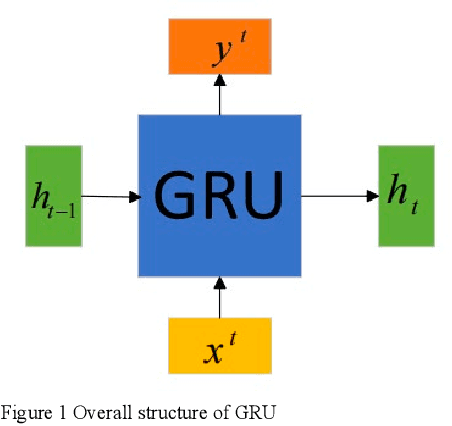

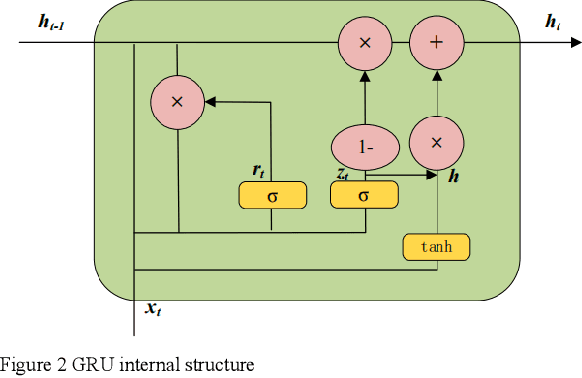

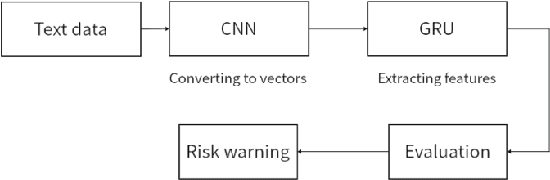

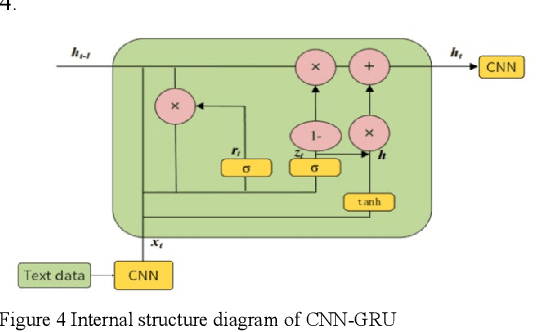

Add to EdgeIntegrative Analysis of Financial Market Sentiment Using CNN and GRU for Risk Prediction and Alert Systems

Dec 13, 2024

This document presents an in-depth examination of stock market sentiment through the integration of Convolutional Neural Networks (CNN) and Gated Recurrent Units (GRU), enabling precise risk alerts. The robust feature extraction capability of CNN is utilized to preprocess and analyze extensive network text data, identifying local features and patterns. The extracted feature sequences are then input into the GRU model to understand the progression of emotional states over time and their potential impact on future market sentiment and risk. This approach addresses the order dependence and long-term dependencies inherent in time series data, resulting in a detailed analysis of stock market sentiment and effective early warnings of future risks.

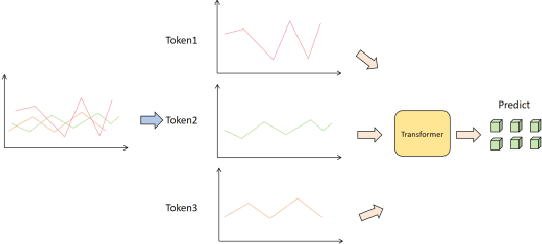

Advanced Risk Prediction and Stability Assessment of Banks Using Time Series Transformer Models

Dec 04, 2024

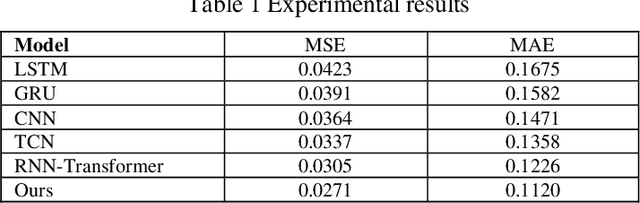

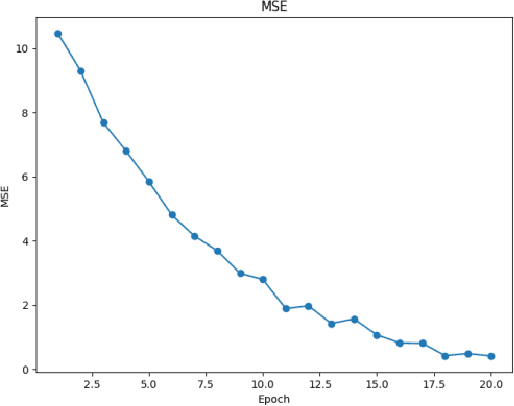

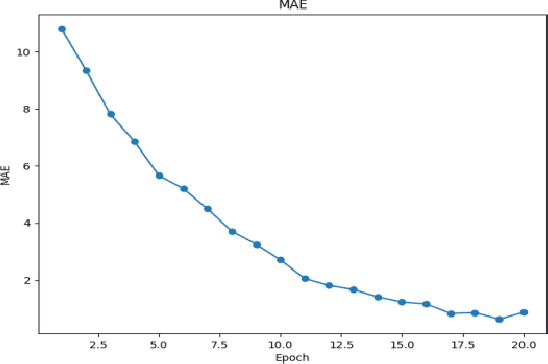

This paper aims to study the prediction of the bank stability index based on the Time Series Transformer model. The bank stability index is an important indicator to measure the health status and risk resistance of financial institutions. Traditional prediction methods are difficult to adapt to complex market changes because they rely on single-dimensional macroeconomic data. This paper proposes a prediction framework based on the Time Series Transformer, which uses the self-attention mechanism of the model to capture the complex temporal dependencies and nonlinear relationships in financial data. Through experiments, we compare the model with LSTM, GRU, CNN, TCN and RNN-Transformer models. The experimental results show that the Time Series Transformer model outperforms other models in both mean square error (MSE) and mean absolute error (MAE) evaluation indicators, showing strong prediction ability. This shows that the Time Series Transformer model can better handle multidimensional time series data in bank stability prediction, providing new technical approaches and solutions for financial risk management.

Applying Hybrid Graph Neural Networks to Strengthen Credit Risk Analysis

Oct 05, 2024This paper presents a novel approach to credit risk prediction by employing Graph Convolutional Neural Networks (GCNNs) to assess the creditworthiness of borrowers. Leveraging the power of big data and artificial intelligence, the proposed method addresses the challenges faced by traditional credit risk assessment models, particularly in handling imbalanced datasets and extracting meaningful features from complex relationships. The paper begins by transforming raw borrower data into graph-structured data, where borrowers and their relationships are represented as nodes and edges, respectively. A classic subgraph convolutional model is then applied to extract local features, followed by the introduction of a hybrid GCNN model that integrates both local and global convolutional operators to capture a comprehensive representation of node features. The hybrid model incorporates an attention mechanism to adaptively select features, mitigating issues of over-smoothing and insufficient feature consideration. The study demonstrates the potential of GCNNs in improving the accuracy of credit risk prediction, offering a robust solution for financial institutions seeking to enhance their lending decision-making processes.

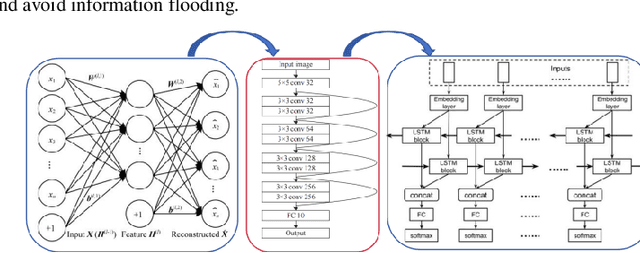

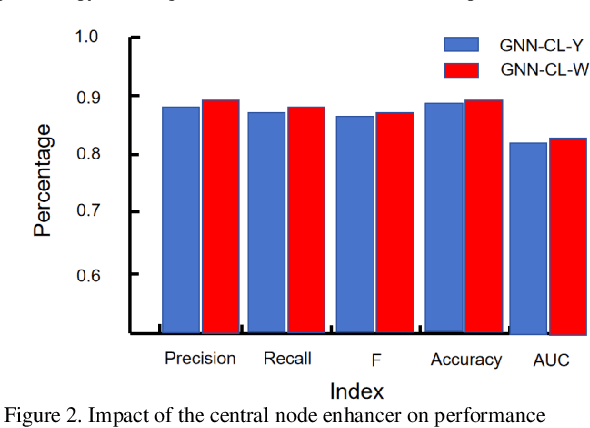

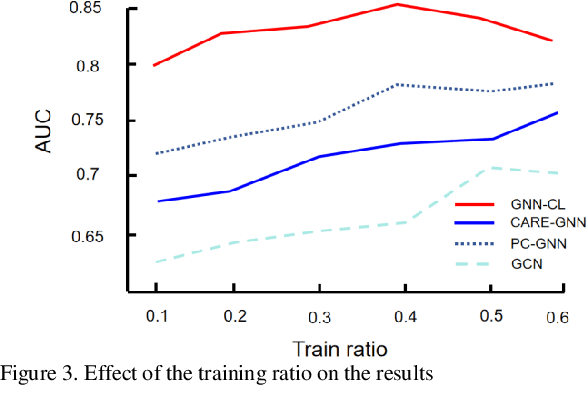

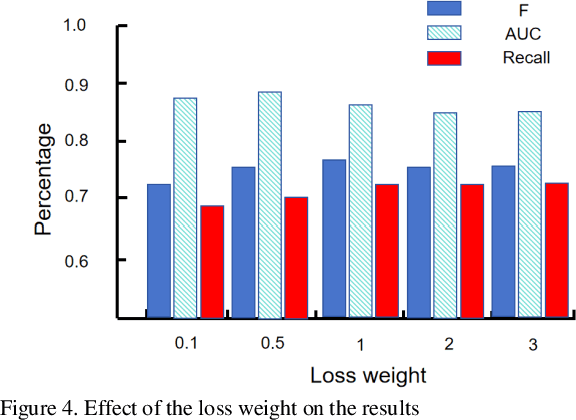

Advanced Financial Fraud Detection Using GNN-CL Model

Jul 09, 2024

The innovative GNN-CL model proposed in this paper marks a breakthrough in the field of financial fraud detection by synergistically combining the advantages of graph neural networks (gnn), convolutional neural networks (cnn) and long short-term memory (LSTM) networks. This convergence enables multifaceted analysis of complex transaction patterns, improving detection accuracy and resilience against complex fraudulent activities. A key novelty of this paper is the use of multilayer perceptrons (MLPS) to estimate node similarity, effectively filtering out neighborhood noise that can lead to false positives. This intelligent purification mechanism ensures that only the most relevant information is considered, thereby improving the model's understanding of the network structure. Feature weakening often plagues graph-based models due to the dilution of key signals. In order to further address the challenge of feature weakening, GNN-CL adopts reinforcement learning strategies. By dynamically adjusting the weights assigned to central nodes, it reinforces the importance of these influential entities to retain important clues of fraud even in less informative data. Experimental evaluations on Yelp datasets show that the results highlight the superior performance of GNN-CL compared to existing methods.

Advancing Financial Risk Prediction Through Optimized LSTM Model Performance and Comparative Analysis

May 31, 2024This paper focuses on the application and optimization of LSTM model in financial risk prediction. The study starts with an overview of the architecture and algorithm foundation of LSTM, and then details the model training process and hyperparameter tuning strategy, and adjusts network parameters through experiments to improve performance. Comparative experiments show that the optimized LSTM model shows significant advantages in AUC index compared with random forest, BP neural network and XGBoost, which verifies its efficiency and practicability in the field of financial risk prediction, especially its ability to deal with complex time series data, which lays a solid foundation for the application of the model in the actual production environment.