Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgedaVinci-Agency: Unlocking Long-Horizon Agency Data-Efficiently

Feb 02, 2026While Large Language Models (LLMs) excel at short-term tasks, scaling them to long-horizon agentic workflows remains challenging. The core bottleneck lies in the scarcity of training data that captures authentic long-dependency structures and cross-stage evolutionary dynamics--existing synthesis methods either confine to single-feature scenarios constrained by model distribution, or incur prohibitive human annotation costs, failing to provide scalable, high-quality supervision. We address this by reconceptualizing data synthesis through the lens of real-world software evolution. Our key insight: Pull Request (PR) sequences naturally embody the supervision signals for long-horizon learning. They decompose complex objectives into verifiable submission units, maintain functional coherence across iterations, and encode authentic refinement patterns through bug-fix histories. Building on this, we propose daVinci-Agency, which systematically mines structured supervision from chain-of-PRs through three interlocking mechanisms: (1) progressive task decomposition via continuous commits, (2) long-term consistency enforcement through unified functional objectives, and (3) verifiable refinement from authentic bug-fix trajectories. Unlike synthetic trajectories that treat each step independently, daVinci-Agency's PR-grounded structure inherently preserves the causal dependencies and iterative refinements essential for teaching persistent goal-directed behavior and enables natural alignment with project-level, full-cycle task modeling. The resulting trajectories are substantial--averaging 85k tokens and 116 tool calls--yet remarkably data-efficient: fine-tuning GLM-4.6 on 239 daVinci-Agency samples yields broad improvements across benchmarks, notably achieving a 47% relative gain on Toolathlon. Beyond benchmark performance, our analysis confirms...

daVinci-Dev: Agent-native Mid-training for Software Engineering

Jan 27, 2026Recently, the frontier of Large Language Model (LLM) capabilities has shifted from single-turn code generation to agentic software engineering-a paradigm where models autonomously navigate, edit, and test complex repositories. While post-training methods have become the de facto approach for code agents, **agentic mid-training**-mid-training (MT) on large-scale data that mirrors authentic agentic workflows-remains critically underexplored due to substantial resource requirements, despite offering a more scalable path to instilling foundational agentic behaviors than relying solely on expensive reinforcement learning. A central challenge in realizing effective agentic mid-training is the distribution mismatch between static training data and the dynamic, feedback-rich environment of real development. To address this, we present a systematic study of agentic mid-training, establishing both the data synthesis principles and training methodology for effective agent development at scale. Central to our approach is **agent-native data**-supervision comprising two complementary types of trajectories: **contextually-native trajectories** that preserve the complete information flow an agent experiences, offering broad coverage and diversity; and **environmentally-native trajectories** collected from executable repositories where observations stem from actual tool invocations and test executions, providing depth and interaction authenticity. We verify the model's agentic capabilities on `SWE-Bench Verified`. We demonstrate our superiority over the previous open software engineering mid-training recipe `Kimi-Dev` under two post-training settings with an aligned base model and agentic scaffold, while using less than half mid-training tokens (73.1B). Besides relative advantage, our best performing 32B and 72B models achieve **56.1%** and **58.5%** resolution rates, respectively, which are ...

AgencyBench: Benchmarking the Frontiers of Autonomous Agents in 1M-Token Real-World Contexts

Jan 16, 2026Large Language Models (LLMs) based autonomous agents demonstrate multifaceted capabilities to contribute substantially to economic production. However, existing benchmarks remain focused on single agentic capability, failing to capture long-horizon real-world scenarios. Moreover, the reliance on human-in-the-loop feedback for realistic tasks creates a scalability bottleneck, hindering automated rollout collection and evaluation. To bridge this gap, we introduce AgencyBench, a comprehensive benchmark derived from daily AI usage, evaluating 6 core agentic capabilities across 32 real-world scenarios, comprising 138 tasks with specific queries, deliverables, and rubrics. These scenarios require an average of 90 tool calls, 1 million tokens, and hours of execution time to resolve. To enable automated evaluation, we employ a user simulation agent to provide iterative feedback, and a Docker sandbox to conduct visual and functional rubric-based assessment. Experiments reveal that closed-source models significantly outperform open-source models (48.4% vs 32.1%). Further analysis reveals significant disparities across models in resource efficiency, feedback-driven self-correction, and specific tool-use preferences. Finally, we investigate the impact of agentic scaffolds, observing that proprietary models demonstrate superior performance within their native ecosystems (e.g., Claude-4.5-Opus via Claude-Agent-SDK), while open-source models exhibit distinct performance peaks, suggesting potential optimization for specific execution frameworks. AgencyBench serves as a critical testbed for next-generation agents, highlighting the necessity of co-optimizing model architecture with agentic frameworks. We believe this work sheds light on the future direction of autonomous agents, and we release the full benchmark and evaluation toolkit at https://github.com/GAIR-NLP/AgencyBench.

Interaction as Intelligence Part II: Asynchronous Human-Agent Rollout for Long-Horizon Task Training

Nov 03, 2025Large Language Model (LLM) agents have recently shown strong potential in domains such as automated coding, deep research, and graphical user interface manipulation. However, training them to succeed on long-horizon, domain-specialized tasks remains challenging. Current methods primarily fall into two categories. The first relies on dense human annotations through behavior cloning, which is prohibitively expensive for long-horizon tasks that can take days or months. The second depends on outcome-driven sampling, which often collapses due to the rarity of valid positive trajectories on domain-specialized tasks. We introduce Apollo, a sampling framework that integrates asynchronous human guidance with action-level data filtering. Instead of requiring annotators to shadow every step, Apollo allows them to intervene only when the agent drifts from a promising trajectory, by providing prior knowledge, strategic advice, etc. This lightweight design makes it possible to sustain interactions for over 30 hours and produces valuable trajectories at a lower cost. Apollo then applies supervision control to filter out sub-optimal actions and prevent error propagation. Together, these components enable reliable and effective data collection in long-horizon environments. To demonstrate the effectiveness of Apollo, we evaluate it using InnovatorBench. Our experiments show that when applied to train the GLM-4.5 model on InnovatorBench, Apollo achieves more than a 50% improvement over the untrained baseline and a 28% improvement over a variant trained without human interaction. These results highlight the critical role of human-in-the-loop sampling and the robustness of Apollo's design in handling long-horizon, domain-specialized tasks.

InnovatorBench: Evaluating Agents' Ability to Conduct Innovative LLM Research

Nov 03, 2025

AI agents could accelerate scientific discovery by automating hypothesis formation, experiment design, coding, execution, and analysis, yet existing benchmarks probe narrow skills in simplified settings. To address this gap, we introduce InnovatorBench, a benchmark-platform pair for realistic, end-to-end assessment of agents performing Large Language Model (LLM) research. It comprises 20 tasks spanning Data Construction, Filtering, Augmentation, Loss Design, Reward Design, and Scaffold Construction, which require runnable artifacts and assessment of correctness, performance, output quality, and uncertainty. To support agent operation, we develop ResearchGym, a research environment offering rich action spaces, distributed and long-horizon execution, asynchronous monitoring, and snapshot saving. We also implement a lightweight ReAct agent that couples explicit reasoning with executable planning using frontier models such as Claude-4, GPT-5, GLM-4.5, and Kimi-K2. Our experiments demonstrate that while frontier models show promise in code-driven research tasks, they struggle with fragile algorithm-related tasks and long-horizon decision making, such as impatience, poor resource management, and overreliance on template-based reasoning. Furthermore, agents require over 11 hours to achieve their best performance on InnovatorBench, underscoring the benchmark's difficulty and showing the potential of InnovatorBench to be the next generation of code-based research benchmark.

DatasetResearch: Benchmarking Agent Systems for Demand-Driven Dataset Discovery

Aug 09, 2025The rapid advancement of large language models has fundamentally shifted the bottleneck in AI development from computational power to data availability-with countless valuable datasets remaining hidden across specialized repositories, research appendices, and domain platforms. As reasoning capabilities and deep research methodologies continue to evolve, a critical question emerges: can AI agents transcend conventional search to systematically discover any dataset that meets specific user requirements, enabling truly autonomous demand-driven data curation? We introduce DatasetResearch, the first comprehensive benchmark evaluating AI agents' ability to discover and synthesize datasets from 208 real-world demands across knowledge-intensive and reasoning-intensive tasks. Our tri-dimensional evaluation framework reveals a stark reality: even advanced deep research systems achieve only 22% score on our challenging DatasetResearch-pro subset, exposing the vast gap between current capabilities and perfect dataset discovery. Our analysis uncovers a fundamental dichotomy-search agents excel at knowledge tasks through retrieval breadth, while synthesis agents dominate reasoning challenges via structured generation-yet both catastrophically fail on "corner cases" outside existing distributions. These findings establish the first rigorous baseline for dataset discovery agents and illuminate the path toward AI systems capable of finding any dataset in the digital universe. Our benchmark and comprehensive analysis provide the foundation for the next generation of self-improving AI systems and are publicly available at https://github.com/GAIR-NLP/DatasetResearch.

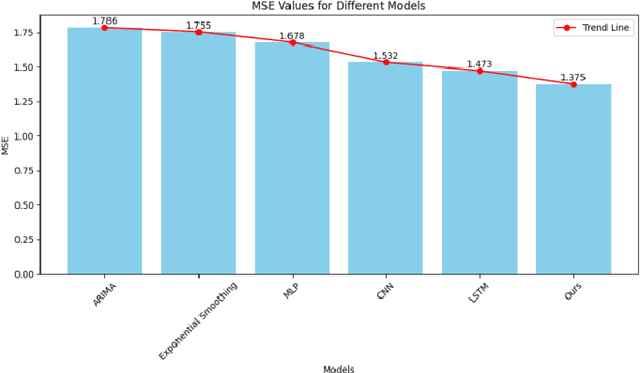

Predicting Liquidity Coverage Ratio with Gated Recurrent Units: A Deep Learning Model for Risk Management

Oct 24, 2024

With the global economic integration and the high interconnection of financial markets, financial institutions are facing unprecedented challenges, especially liquidity risk. This paper proposes a liquidity coverage ratio (LCR) prediction model based on the gated recurrent unit (GRU) network to help financial institutions manage their liquidity risk more effectively. By utilizing the GRU network in deep learning technology, the model can automatically learn complex patterns from historical data and accurately predict LCR for a period of time in the future. The experimental results show that compared with traditional methods, the GRU model proposed in this study shows significant advantages in mean absolute error (MAE), proving its higher accuracy and robustness. This not only provides financial institutions with a more reliable liquidity risk management tool but also provides support for regulators to formulate more scientific and reasonable policies, which helps to improve the stability of the entire financial system.

Applying Hybrid Graph Neural Networks to Strengthen Credit Risk Analysis

Oct 05, 2024This paper presents a novel approach to credit risk prediction by employing Graph Convolutional Neural Networks (GCNNs) to assess the creditworthiness of borrowers. Leveraging the power of big data and artificial intelligence, the proposed method addresses the challenges faced by traditional credit risk assessment models, particularly in handling imbalanced datasets and extracting meaningful features from complex relationships. The paper begins by transforming raw borrower data into graph-structured data, where borrowers and their relationships are represented as nodes and edges, respectively. A classic subgraph convolutional model is then applied to extract local features, followed by the introduction of a hybrid GCNN model that integrates both local and global convolutional operators to capture a comprehensive representation of node features. The hybrid model incorporates an attention mechanism to adaptively select features, mitigating issues of over-smoothing and insufficient feature consideration. The study demonstrates the potential of GCNNs in improving the accuracy of credit risk prediction, offering a robust solution for financial institutions seeking to enhance their lending decision-making processes.

Wasserstein Distance-Weighted Adversarial Network for Cross-Domain Credit Risk Assessment

Sep 27, 2024

This paper delves into the application of adversarial domain adaptation (ADA) for enhancing credit risk assessment in financial institutions. It addresses two critical challenges: the cold start problem, where historical lending data is scarce, and the data imbalance issue, where high-risk transactions are underrepresented. The paper introduces an improved ADA framework, the Wasserstein Distance Weighted Adversarial Domain Adaptation Network (WD-WADA), which leverages the Wasserstein distance to align source and target domains effectively. The proposed method includes an innovative weighted strategy to tackle data imbalance, adjusting for both the class distribution and the difficulty level of predictions. The paper demonstrates that WD-WADA not only mitigates the cold start problem but also provides a more accurate measure of domain differences, leading to improved cross-domain credit risk assessment. Extensive experiments on real-world credit datasets validate the model's effectiveness, showcasing superior performance in cross-domain learning, classification accuracy, and model stability compared to traditional methods.