Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdvanced Risk Prediction and Stability Assessment of Banks Using Time Series Transformer Models

Paper and Code

Dec 04, 2024

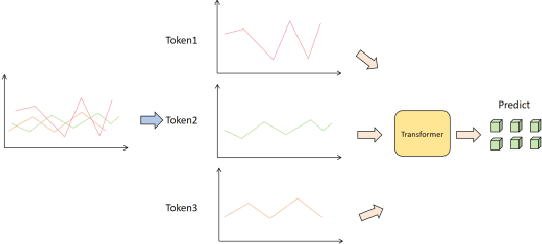

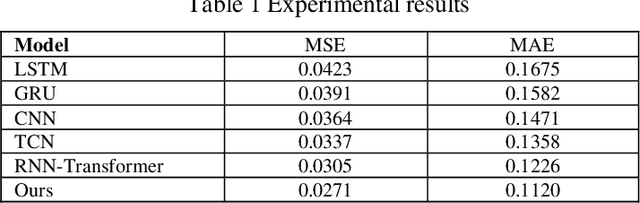

This paper aims to study the prediction of the bank stability index based on the Time Series Transformer model. The bank stability index is an important indicator to measure the health status and risk resistance of financial institutions. Traditional prediction methods are difficult to adapt to complex market changes because they rely on single-dimensional macroeconomic data. This paper proposes a prediction framework based on the Time Series Transformer, which uses the self-attention mechanism of the model to capture the complex temporal dependencies and nonlinear relationships in financial data. Through experiments, we compare the model with LSTM, GRU, CNN, TCN and RNN-Transformer models. The experimental results show that the Time Series Transformer model outperforms other models in both mean square error (MSE) and mean absolute error (MAE) evaluation indicators, showing strong prediction ability. This shows that the Time Series Transformer model can better handle multidimensional time series data in bank stability prediction, providing new technical approaches and solutions for financial risk management.