Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeIntegrative Analysis of Financial Market Sentiment Using CNN and GRU for Risk Prediction and Alert Systems

Paper and Code

Dec 13, 2024

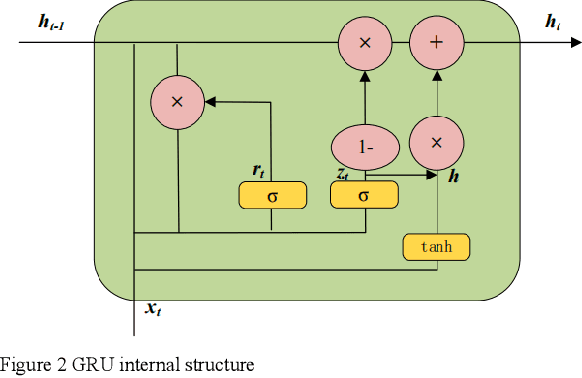

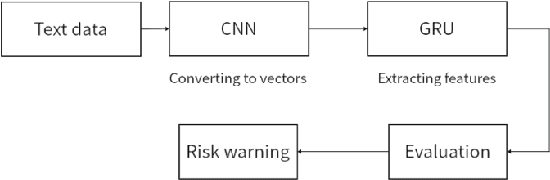

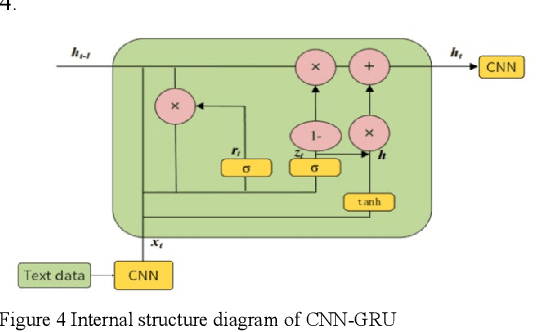

This document presents an in-depth examination of stock market sentiment through the integration of Convolutional Neural Networks (CNN) and Gated Recurrent Units (GRU), enabling precise risk alerts. The robust feature extraction capability of CNN is utilized to preprocess and analyze extensive network text data, identifying local features and patterns. The extracted feature sequences are then input into the GRU model to understand the progression of emotional states over time and their potential impact on future market sentiment and risk. This approach addresses the order dependence and long-term dependencies inherent in time series data, resulting in a detailed analysis of stock market sentiment and effective early warnings of future risks.