Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

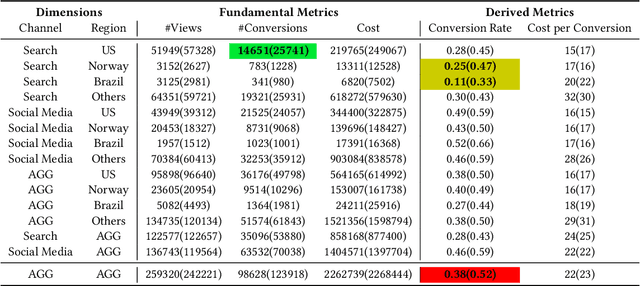

Add to EdgeCMMD: Cross-Metric Multi-Dimensional Root Cause Analysis

Mar 30, 2022

In large-scale online services, crucial metrics, a.k.a., key performance indicators (KPIs), are monitored periodically to check their running statuses. Generally, KPIs are aggregated along multiple dimensions and derived by complex calculations among fundamental metrics from the raw data. Once abnormal KPI values are observed, root cause analysis (RCA) can be applied to identify the reasons for anomalies, so that we can troubleshoot quickly. Recently, several automatic RCA techniques were proposed to localize the related dimensions (or a combination of dimensions) to explain the anomalies. However, their analyses are limited to the data on the abnormal metric and ignore the data of other metrics which may be also related to the anomalies, leading to imprecise or even incorrect root causes. To this end, we propose a cross-metric multi-dimensional root cause analysis method, named CMMD, which consists of two key components: 1) relationship modeling, which utilizes graph neural network (GNN) to model the unknown complex calculation among metrics and aggregation function among dimensions from historical data; 2) root cause localization, which adopts the genetic algorithm to efficiently and effectively dive into the raw data and localize the abnormal dimension(s) once the KPI anomalies are detected. Experiments on synthetic datasets, public datasets and online production environment demonstrate the superiority of our proposed CMMD method compared with baselines. Currently, CMMD is running as an online service in Microsoft Azure.

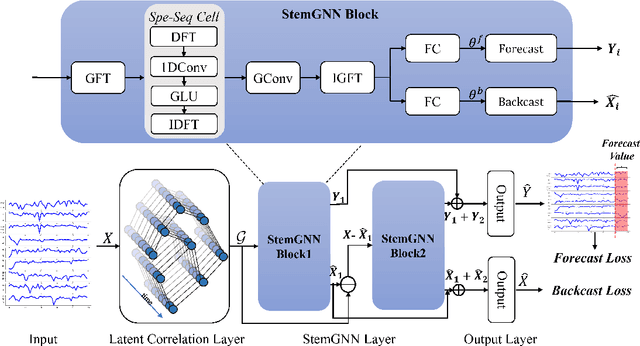

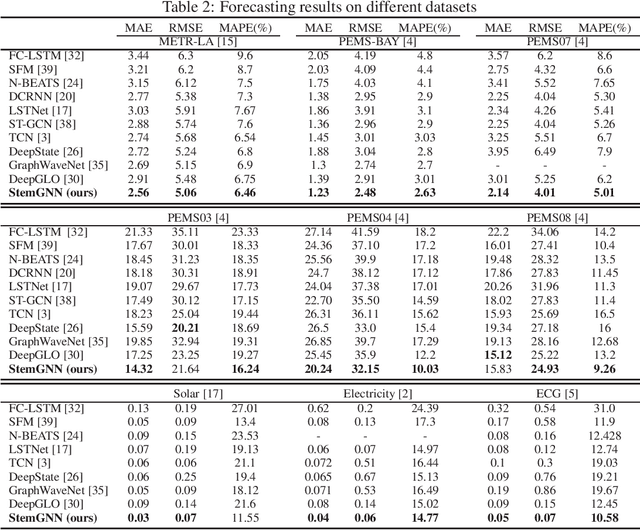

Spectral Temporal Graph Neural Network for Multivariate Time-series Forecasting

Mar 13, 2021

Multivariate time-series forecasting plays a crucial role in many real-world applications. It is a challenging problem as one needs to consider both intra-series temporal correlations and inter-series correlations simultaneously. Recently, there have been multiple works trying to capture both correlations, but most, if not all of them only capture temporal correlations in the time domain and resort to pre-defined priors as inter-series relationships. In this paper, we propose Spectral Temporal Graph Neural Network (StemGNN) to further improve the accuracy of multivariate time-series forecasting. StemGNN captures inter-series correlations and temporal dependencies \textit{jointly} in the \textit{spectral domain}. It combines Graph Fourier Transform (GFT) which models inter-series correlations and Discrete Fourier Transform (DFT) which models temporal dependencies in an end-to-end framework. After passing through GFT and DFT, the spectral representations hold clear patterns and can be predicted effectively by convolution and sequential learning modules. Moreover, StemGNN learns inter-series correlations automatically from the data without using pre-defined priors. We conduct extensive experiments on ten real-world datasets to demonstrate the effectiveness of StemGNN. Code is available at https://github.com/microsoft/StemGNN/

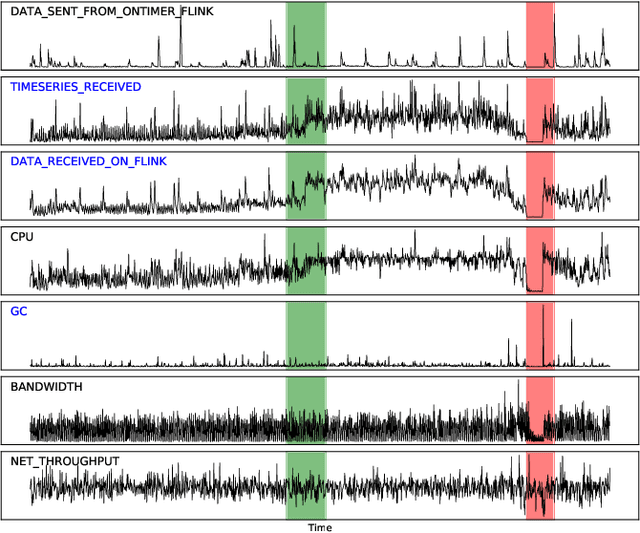

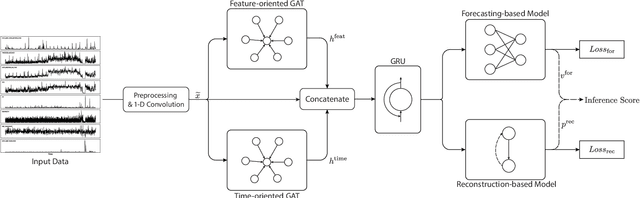

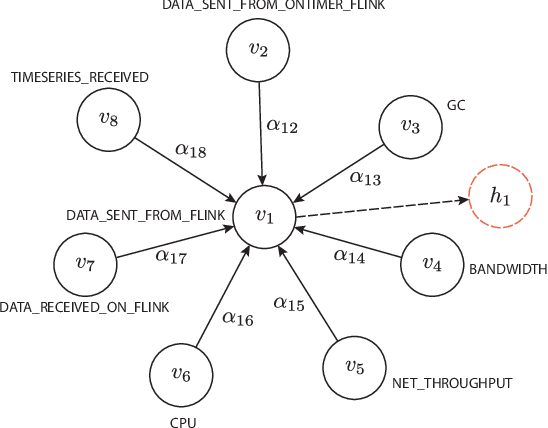

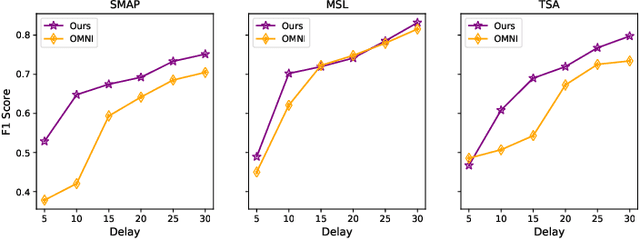

Multivariate Time-series Anomaly Detection via Graph Attention Network

Sep 04, 2020

Anomaly detection on multivariate time-series is of great importance in both data mining research and industrial applications. Recent approaches have achieved significant progress in this topic, but there is remaining limitations. One major limitation is that they do not capture the relationships between different time-series explicitly, resulting in inevitable false alarms. In this paper, we propose a novel self-supervised framework for multivariate time-series anomaly detection to address this issue. Our framework considers each univariate time-series as an individual feature and includes two graph attention layers in parallel to learn the complex dependencies of multivariate time-series in both temporal and feature dimensions. In addition, our approach jointly optimizes a forecasting-based model and are construction-based model, obtaining better time-series representations through a combination of single-timestamp prediction and reconstruction of the entire time-series. We demonstrate the efficacy of our model through extensive experiments. The proposed method outperforms other state-of-the-art models on three real-world datasets. Further analysis shows that our method has good interpretability and is useful for anomaly diagnosis.

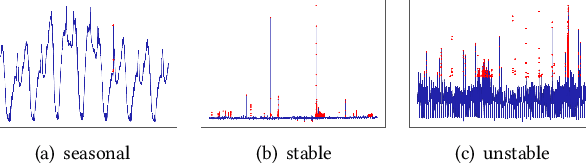

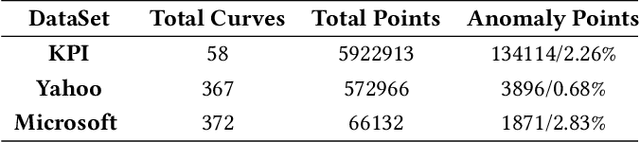

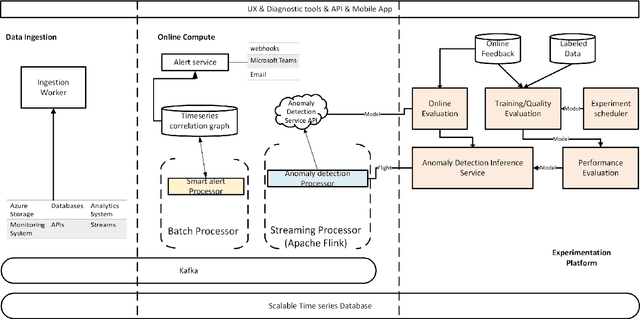

Time-Series Anomaly Detection Service at Microsoft

Jun 10, 2019

Large companies need to monitor various metrics (for example, Page Views and Revenue) of their applications and services in real time. At Microsoft, we develop a time-series anomaly detection service which helps customers to monitor the time-series continuously and alert for potential incidents on time. In this paper, we introduce the pipeline and algorithm of our anomaly detection service, which is designed to be accurate, efficient and general. The pipeline consists of three major modules, including data ingestion, experimentation platform and online compute. To tackle the problem of time-series anomaly detection, we propose a novel algorithm based on Spectral Residual (SR) and Convolutional Neural Network (CNN). Our work is the first attempt to borrow the SR model from visual saliency detection domain to time-series anomaly detection. Moreover, we innovatively combine SR and CNN together to improve the performance of SR model. Our approach achieves superior experimental results compared with state-of-the-art baselines on both public datasets and Microsoft production data.