Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTraceable Latent Variable Discovery Based on Multi-Agent Collaboration

Feb 16, 2026Revealing the underlying causal mechanisms in the real world is crucial for scientific and technological progress. Despite notable advances in recent decades, the lack of high-quality data and the reliance of traditional causal discovery algorithms (TCDA) on the assumption of no latent confounders, as well as their tendency to overlook the precise semantics of latent variables, have long been major obstacles to the broader application of causal discovery. To address this issue, we propose a novel causal modeling framework, TLVD, which integrates the metadata-based reasoning capabilities of large language models (LLMs) with the data-driven modeling capabilities of TCDA for inferring latent variables and their semantics. Specifically, we first employ a data-driven approach to construct a causal graph that incorporates latent variables. Then, we employ multi-LLM collaboration for latent variable inference, modeling this process as a game with incomplete information and seeking its Bayesian Nash Equilibrium (BNE) to infer the possible specific latent variables. Finally, to validate the inferred latent variables across multiple real-world web-based data sources, we leverage LLMs for evidence exploration to ensure traceability. We comprehensively evaluate TLVD on three de-identified real patient datasets provided by a hospital and two benchmark datasets. Extensive experimental results confirm the effectiveness and reliability of TLVD, with average improvements of 32.67% in Acc, 62.21% in CAcc, and 26.72% in ECit across the five datasets.

Transferable Graph Condensation from the Causal Perspective

Jan 29, 2026The increasing scale of graph datasets has significantly improved the performance of graph representation learning methods, but it has also introduced substantial training challenges. Graph dataset condensation techniques have emerged to compress large datasets into smaller yet information-rich datasets, while maintaining similar test performance. However, these methods strictly require downstream applications to match the original dataset and task, which often fails in cross-task and cross-domain scenarios. To address these challenges, we propose a novel causal-invariance-based and transferable graph dataset condensation method, named \textbf{TGCC}, providing effective and transferable condensed datasets. Specifically, to preserve domain-invariant knowledge, we first extract domain causal-invariant features from the spatial domain of the graph using causal interventions. Then, to fully capture the structural and feature information of the original graph, we perform enhanced condensation operations. Finally, through spectral-domain enhanced contrastive learning, we inject the causal-invariant features into the condensed graph, ensuring that the compressed graph retains the causal information of the original graph. Experimental results on five public datasets and our novel \textbf{FinReport} dataset demonstrate that TGCC achieves up to a 13.41\% improvement in cross-task and cross-domain complex scenarios compared to existing methods, and achieves state-of-the-art performance on 5 out of 6 datasets in the single dataset and task scenario.

Taming Gradient Variance in Federated Learning with Networked Control Variates

Oct 26, 2023Federated learning, a decentralized approach to machine learning, faces significant challenges such as extensive communication overheads, slow convergence, and unstable improvements. These challenges primarily stem from the gradient variance due to heterogeneous client data distributions. To address this, we introduce a novel Networked Control Variates (FedNCV) framework for Federated Learning. We adopt the REINFORCE Leave-One-Out (RLOO) as a fundamental control variate unit in the FedNCV framework, implemented at both client and server levels. At the client level, the RLOO control variate is employed to optimize local gradient updates, mitigating the variance introduced by data samples. Once relayed to the server, the RLOO-based estimator further provides an unbiased and low-variance aggregated gradient, leading to robust global updates. This dual-side application is formalized as a linear combination of composite control variates. We provide a mathematical expression capturing this integration of double control variates within FedNCV and present three theoretical results with corresponding proofs. This unique dual structure equips FedNCV to address data heterogeneity and scalability issues, thus potentially paving the way for large-scale applications. Moreover, we tested FedNCV on six diverse datasets under a Dirichlet distribution with {\alpha} = 0.1, and benchmarked its performance against six SOTA methods, demonstrating its superiority.

A Comprehensive Survey on Enterprise Financial Risk Analysis: Problems, Methods, Spotlights and Applications

Nov 28, 2022Enterprise financial risk analysis aims at predicting the enterprises' future financial risk.Due to the wide application, enterprise financial risk analysis has always been a core research issue in finance. Although there are already some valuable and impressive surveys on risk management, these surveys introduce approaches in a relatively isolated way and lack the recent advances in enterprise financial risk analysis. Due to the rapid expansion of the enterprise financial risk analysis, especially from the computer science and big data perspective, it is both necessary and challenging to comprehensively review the relevant studies. This survey attempts to connect and systematize the existing enterprise financial risk researches, as well as to summarize and interpret the mechanisms and the strategies of enterprise financial risk analysis in a comprehensive way, which may help readers have a better understanding of the current research status and ideas. This paper provides a systematic literature review of over 300 articles published on enterprise risk analysis modelling over a 50-year period, 1968 to 2022. We first introduce the formal definition of enterprise risk as well as the related concepts. Then, we categorized the representative works in terms of risk type and summarized the three aspects of risk analysis. Finally, we compared the analysis methods used to model the enterprise financial risk. Our goal is to clarify current cutting-edge research and its possible future directions to model enterprise risk, aiming to fully understand the mechanisms of enterprise risk communication and influence and its application on corporate governance, financial institution and government regulation.

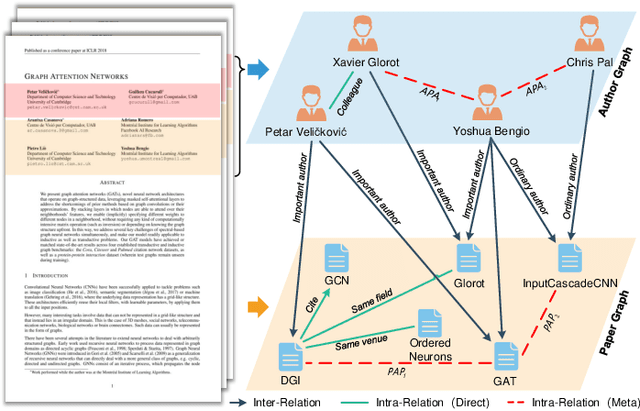

Learning Bi-typed Multi-relational Heterogeneous Graph via Dual Hierarchical Attention Networks

Jan 25, 2022

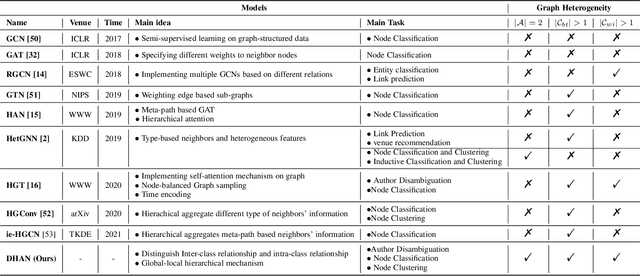

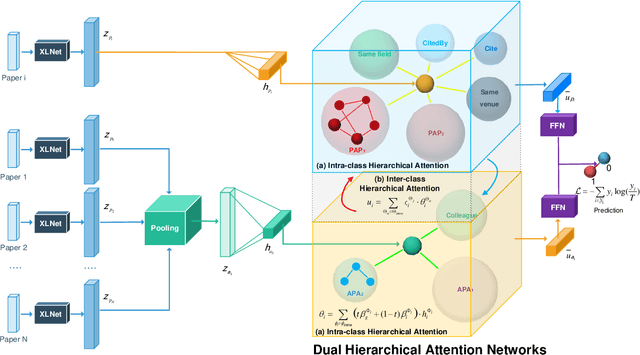

Bi-type multi-relational heterogeneous graph (BMHG) is one of the most common graphs in practice, for example, academic networks, e-commerce user behavior graph and enterprise knowledge graph. It is a critical and challenge problem on how to learn the numerical representation for each node to characterize subtle structures. However, most previous studies treat all node relations in BMHG as the same class of relation without distinguishing the different characteristics between the intra-class relations and inter-class relations of the bi-typed nodes, causing the loss of significant structure information. To address this issue, we propose a novel Dual Hierarchical Attention Networks (DHAN) based on the bi-typed multi-relational heterogeneous graphs to learn comprehensive node representations with the intra-class and inter-class attention-based encoder under a hierarchical mechanism. Specifically, the former encoder aggregates information from the same type of nodes, while the latter aggregates node representations from its different types of neighbors. Moreover, to sufficiently model node multi-relational information in BMHG, we adopt a newly proposed hierarchical mechanism. By doing so, the proposed dual hierarchical attention operations enable our model to fully capture the complex structures of the bi-typed multi-relational heterogeneous graphs. Experimental results on various tasks against the state-of-the-arts sufficiently confirm the capability of DHAN in learning node representations on the BMHGs.

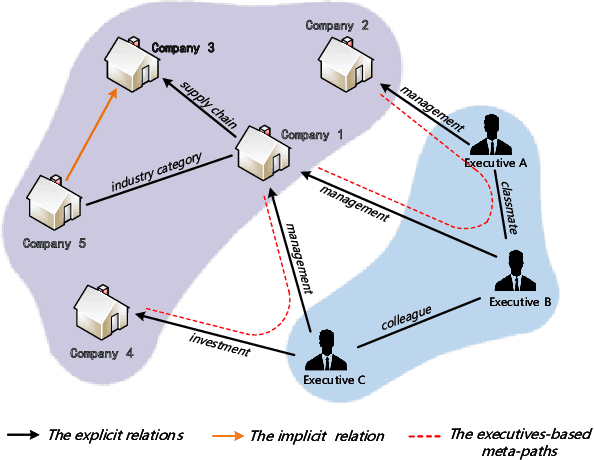

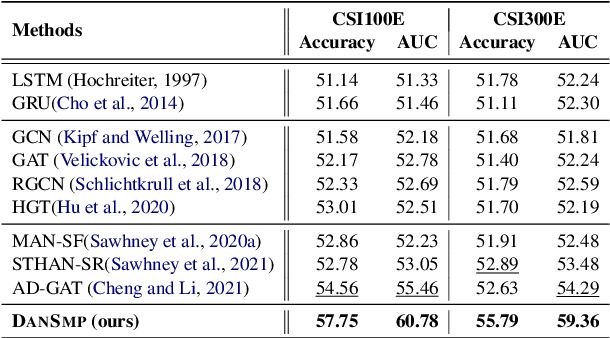

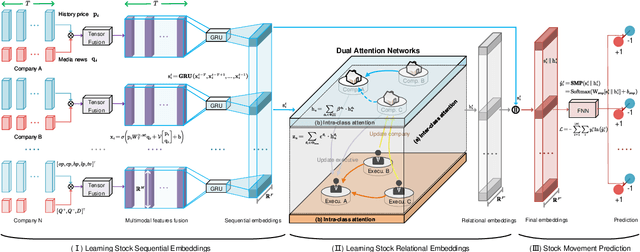

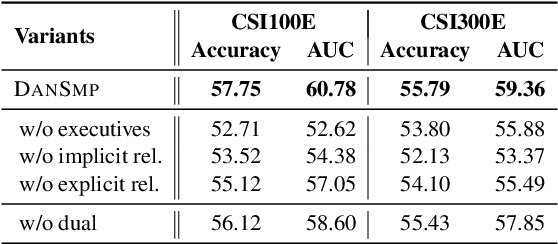

Stock Movement Prediction Based on Bi-typed Hybrid-relational Market Knowledge Graph via Dual Attention Networks

Jan 24, 2022

Stock Movement Prediction (SMP) aims at predicting listed companies' stock future price trend, which is a challenging task due to the volatile nature of financial markets. Recent financial studies show that the momentum spillover effect plays a significant role in stock fluctuation. However, previous studies typically only learn the simple connection information among related companies, which inevitably fail to model complex relations of listed companies in the real financial market. To address this issue, we first construct a more comprehensive Market Knowledge Graph (MKG) which contains bi-typed entities including listed companies and their associated executives, and hybrid-relations including the explicit relations and implicit relations. Afterward, we propose DanSmp, a novel Dual Attention Networks to learn the momentum spillover signals based upon the constructed MKG for stock prediction. The empirical experiments on our constructed datasets against nine SOTA baselines demonstrate that the proposed DanSmp is capable of improving stock prediction with the constructed MKG.