Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTemporal Data Meets LLM -- Explainable Financial Time Series Forecasting

Jun 19, 2023This paper presents a novel study on harnessing Large Language Models' (LLMs) outstanding knowledge and reasoning abilities for explainable financial time series forecasting. The application of machine learning models to financial time series comes with several challenges, including the difficulty in cross-sequence reasoning and inference, the hurdle of incorporating multi-modal signals from historical news, financial knowledge graphs, etc., and the issue of interpreting and explaining the model results. In this paper, we focus on NASDAQ-100 stocks, making use of publicly accessible historical stock price data, company metadata, and historical economic/financial news. We conduct experiments to illustrate the potential of LLMs in offering a unified solution to the aforementioned challenges. Our experiments include trying zero-shot/few-shot inference with GPT-4 and instruction-based fine-tuning with a public LLM model Open LLaMA. We demonstrate our approach outperforms a few baselines, including the widely applied classic ARMA-GARCH model and a gradient-boosting tree model. Through the performance comparison results and a few examples, we find LLMs can make a well-thought decision by reasoning over information from both textual news and price time series and extracting insights, leveraging cross-sequence information, and utilizing the inherent knowledge embedded within the LLM. Additionally, we show that a publicly available LLM such as Open-LLaMA, after fine-tuning, can comprehend the instruction to generate explainable forecasts and achieve reasonable performance, albeit relatively inferior in comparison to GPT-4.

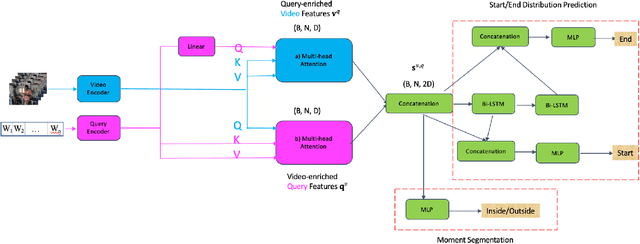

Video Moment Retrieval via Natural Language Queries

Sep 10, 2020

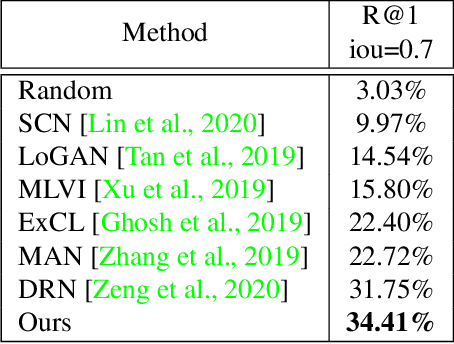

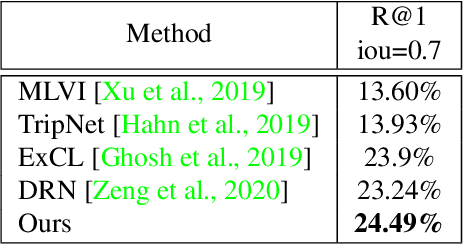

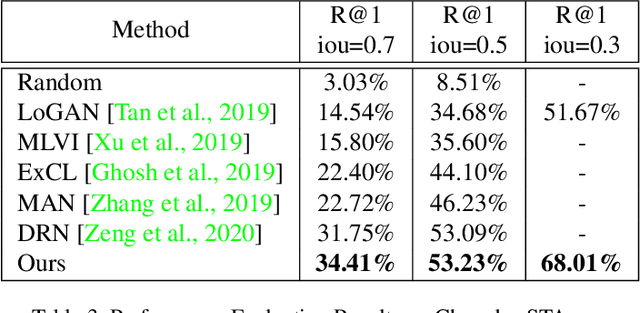

In this paper, we propose a novel method for video moment retrieval (VMR) that achieves state of the arts (SOTA) performance on R@1 metrics and surpassing the SOTA on the high IoU metric (R@1, IoU=0.7). First, we propose to use a multi-head self-attention mechanism, and further a cross-attention scheme to capture video/query interaction and long-range query dependencies from video context. The attention-based methods can develop frame-to-query interaction and query-to-frame interaction at arbitrary positions and the multi-head setting ensures the sufficient understanding of complicated dependencies. Our model has a simple architecture, which enables faster training and inference while maintaining . Second, We also propose to use multiple task training objective consists of moment segmentation task, start/end distribution prediction and start/end location regression task. We have verified that start/end prediction are noisy due to annotator disagreement and joint training with moment segmentation task can provide richer information since frames inside the target clip are also utilized as positive training examples. Third, we propose to use an early fusion approach, which achieves better performance at the cost of inference time. However, the inference time will not be a problem for our model since our model has a simple architecture which enables efficient training and inference.

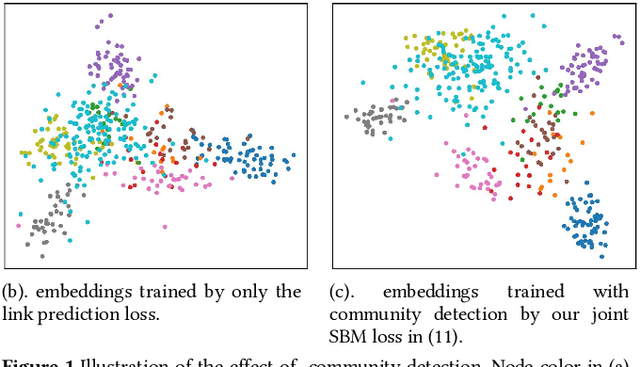

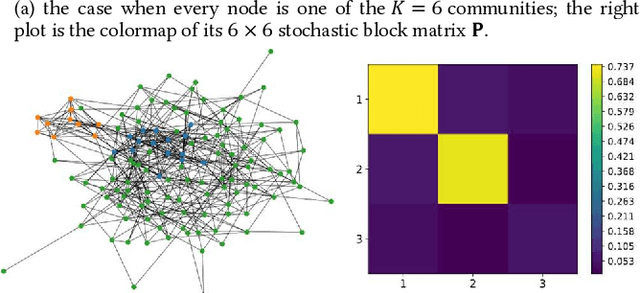

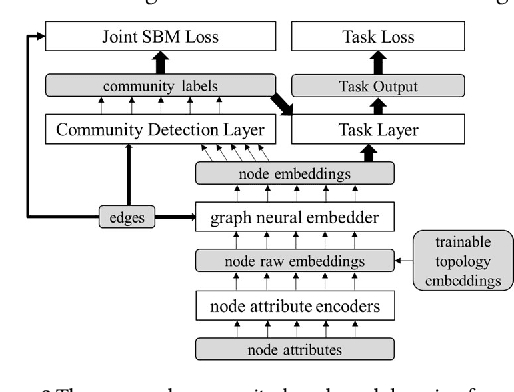

Neural Stochastic Block Model & Scalable Community-Based Graph Learning

May 16, 2020

This paper proposes a novel scalable community-based neural framework for graph learning. The framework learns the graph topology through the task of community detection and link prediction by optimizing with our proposed joint SBM loss function, which results from a non-trivial adaptation of the likelihood function of the classic Stochastic Block Model (SBM). Compared with SBM, our framework is flexible, naturally allows soft labels and digestion of complex node attributes. The main goal is efficient valuation of complex graph data, therefore our design carefully aims at accommodating large data, and ensures there is a single forward pass for efficient evaluation. For large graph, it remains an open problem of how to efficiently leverage its underlying structure for various graph learning tasks. Previously it can be heavy work. With our community-based framework, this becomes less difficult and allows the task models to basically plug-in-and-play and perform joint training. We currently look into two particular applications, the graph alignment and the anomalous correlation detection, and discuss how to make use of our framework to tackle both problems. Extensive experiments are conducted to demonstrate the effectiveness of our approach. We also contributed tweaks of classic techniques which we find helpful for performance and scalability. For example, 1) the GAT+, an improved design of GAT (Graph Attention Network), the scaled-cosine similarity, and a unified implementation of the convolution/attention based and the random-walk based neural graph models.

Large-Scale Joint Topic, Sentiment & User Preference Analysis for Online Reviews

Jan 14, 2019

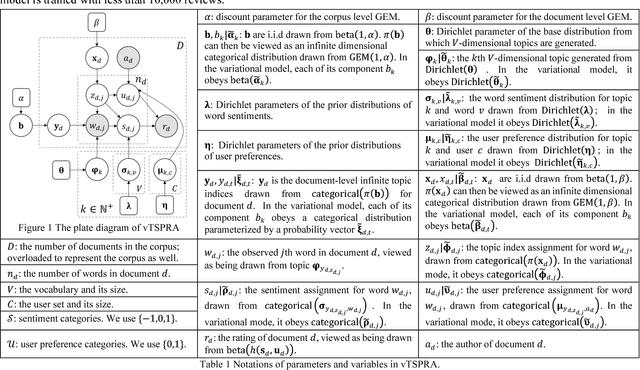

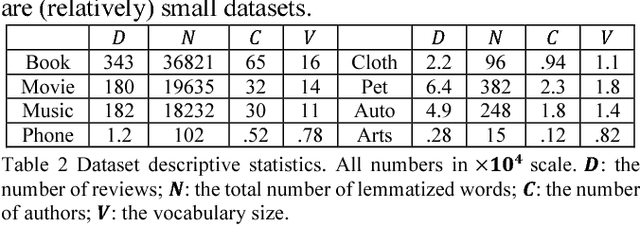

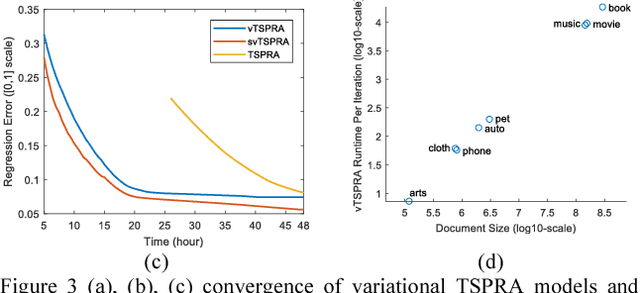

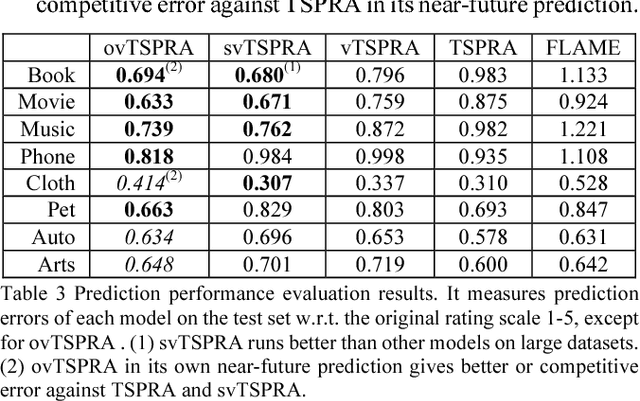

This paper presents a non-trivial reconstruction of a previous joint topic-sentiment-preference review model TSPRA with stick-breaking representation under the framework of variational inference (VI) and stochastic variational inference (SVI). TSPRA is a Gibbs Sampling based model that solves topics, word sentiments and user preferences altogether and has been shown to achieve good performance, but for large data set it can only learn from a relatively small sample. We develop the variational models vTSPRA and svTSPRA to improve the time use, and our new approach is capable of processing millions of reviews. We rebuild the generative process, improve the rating regression, solve and present the coordinate-ascent updates of variational parameters, and show the time complexity of each iteration is theoretically linear to the corpus size, and the experiments on Amazon data sets show it converges faster than TSPRA and attains better results given the same amount of time. In addition, we tune svTSPRA into an online algorithm ovTSPRA that can monitor oscillations of sentiment and preference overtime. Some interesting fluctuations are captured and possible explanations are provided. The results give strong visual evidence that user preference is better treated as an independent factor from sentiment.

Correlated Anomaly Detection from Large Streaming Data

Jan 14, 2019

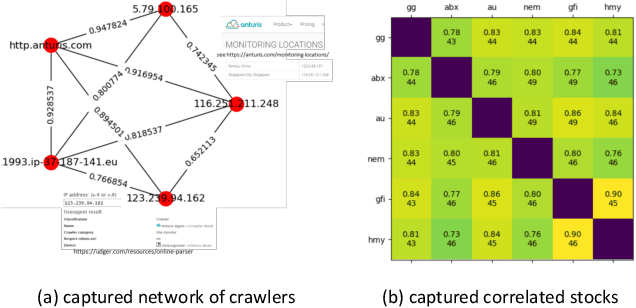

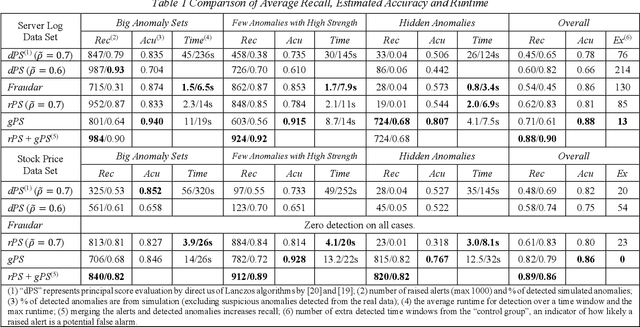

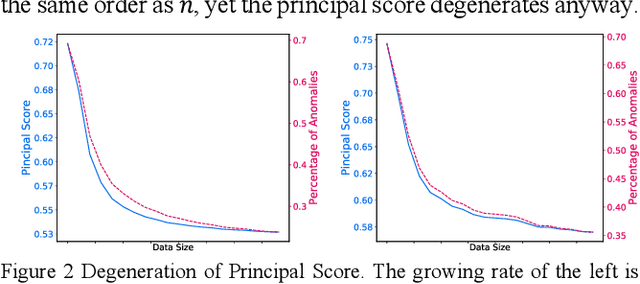

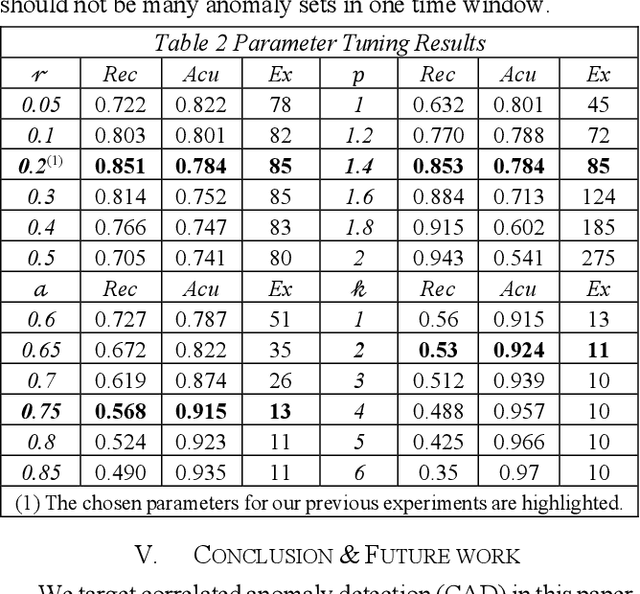

Correlated anomaly detection (CAD) from streaming data is a type of group anomaly detection and an essential task in useful real-time data mining applications like botnet detection, financial event detection, industrial process monitor, etc. The primary approach for this type of detection in previous researches is based on principal score (PS) of divided batches or sliding windows by computing top eigenvalues of the correlation matrix, e.g. the Lanczos algorithm. However, this paper brings up the phenomenon of principal score degeneration for large data set, and then mathematically and practically prove current PS-based methods are likely to fail for CAD on large-scale streaming data even if the number of correlated anomalies grows with the data size at a reasonable rate; in reality, anomalies tend to be the minority of the data, and this issue can be more serious. We propose a framework with two novel randomized algorithms rPS and gPS for better detection of correlated anomalies from large streaming data of various correlation strength. The experiment shows high and balanced recall and estimated accuracy of our framework for anomaly detection from a large server log data set and a U.S. stock daily price data set in comparison to direct principal score evaluation and some other recent group anomaly detection algorithms. Moreover, our techniques significantly improve the computation efficiency and scalability for principal score calculation.

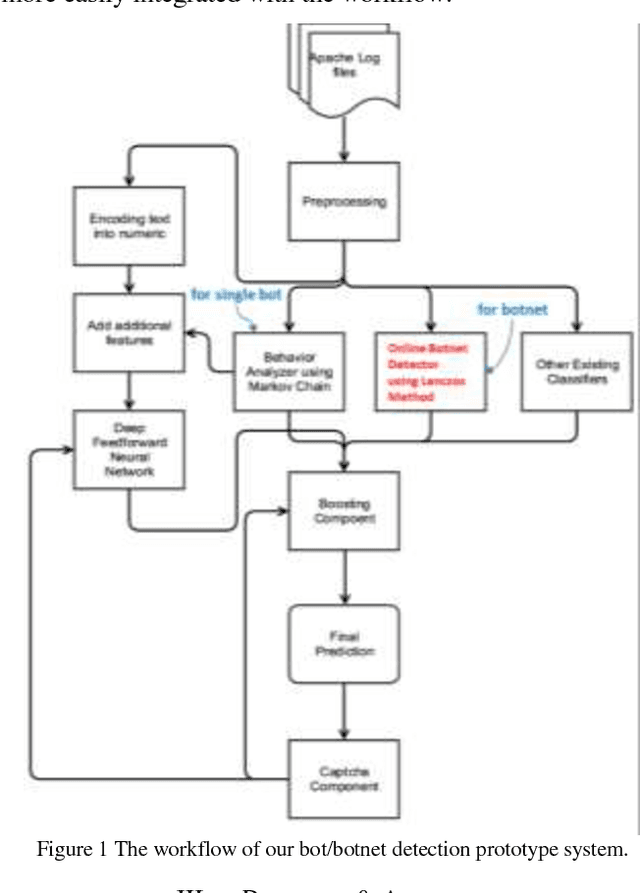

Fast Botnet Detection From Streaming Logs Using Online Lanczos Method

Dec 19, 2018

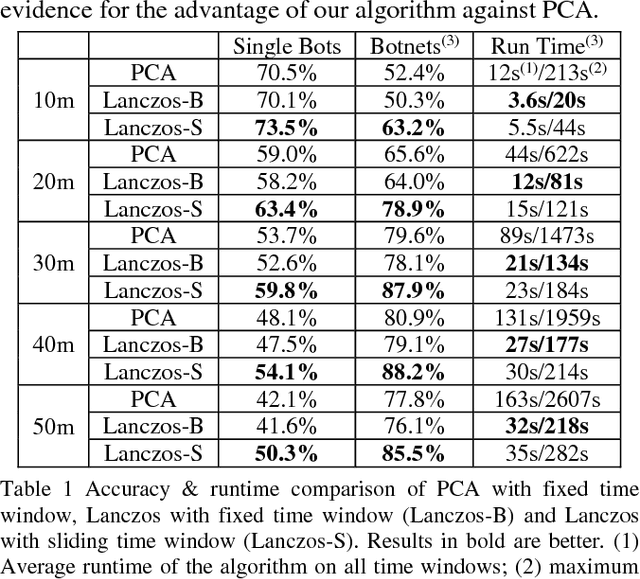

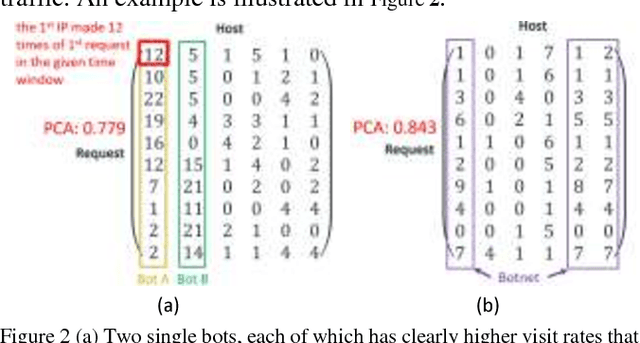

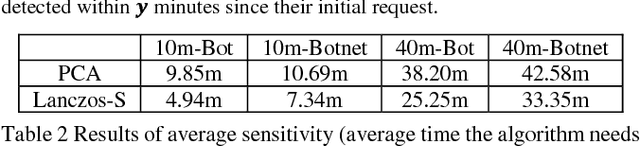

Botnet, a group of coordinated bots, is becoming the main platform of malicious Internet activities like DDOS, click fraud, web scraping, spam/rumor distribution, etc. This paper focuses on design and experiment of a new approach for botnet detection from streaming web server logs, motivated by its wide applicability, real-time protection capability, ease of use and better security of sensitive data. Our algorithm is inspired by a Principal Component Analysis (PCA) to capture correlation in data, and we are first to recognize and adapt Lanczos method to improve the time complexity of PCA-based botnet detection from cubic to sub-cubic, which enables us to more accurately and sensitively detect botnets with sliding time windows rather than fixed time windows. We contribute a generalized online correlation matrix update formula, and a new termination condition for Lanczos iteration for our purpose based on error bound and non-decreasing eigenvalues of symmetric matrices. On our dataset of an ecommerce website logs, experiments show the time cost of Lanczos method with different time windows are consistently only 20% to 25% of PCA.