Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSafe Reinforcement Learning with Preference-based Constraint Inference

Mar 24, 2026Safe reinforcement learning (RL) is a standard paradigm for safety-critical decision making. However, real-world safety constraints can be complex, subjective, and even hard to explicitly specify. Existing works on constraint inference rely on restrictive assumptions or extensive expert demonstrations, which is not realistic in many real-world applications. How to cheaply and reliably learn these constraints is the major challenge we focus on in this study. While inferring constraints from human preferences offers a data-efficient alternative, we identify the popular Bradley-Terry (BT) models fail to capture the asymmetric, heavy-tailed nature of safety costs, resulting in risk underestimation. It is still rare in the literature to understand the impacts of BT models on the downstream policy learning. To address the above knowledge gaps, we propose a novel approach namely Preference-based Constrained Reinforcement Learning (PbCRL). We introduce a novel dead zone mechanism into preference modeling and theoretically prove that it encourages heavy-tailed cost distributions, thereby achieving better constraint alignment. Additionally, we incorporate a Signal-to-Noise Ratio (SNR) loss to encourage exploration by cost variances, which is found to benefit policy learning. Further, two-stage training strategy are deployed to lower online labeling burdens while adaptively enhancing constraint satisfaction. Empirical results demonstrate that PbCRL achieves superior alignment with true safety requirements and outperforms the state-of-the-art baselines in terms of safety and reward. Our work explores a promising and effective way for constraint inference in Safe RL, which has great potential in a range of safety-critical applications.

A Graph Neural Network with Auxiliary Task Learning for Missing PMU Data Reconstruction

Dec 31, 2025In wide-area measurement systems (WAMS), phasor measurement unit (PMU) measurement is prone to data missingness due to hardware failures, communication delays, and cyber-attacks. Existing data-driven methods are limited by inadaptability to concept drift in power systems, poor robustness under high missing rates, and reliance on the unrealistic assumption of full system observability. Thus, this paper proposes an auxiliary task learning (ATL) method for reconstructing missing PMU data. First, a K-hop graph neural network (GNN) is proposed to enable direct learning on the subgraph consisting of PMU nodes, overcoming the limitation of the incompletely observable system. Then, an auxiliary learning framework consisting of two complementary graph networks is designed for accurate reconstruction: a spatial-temporal GNN extracts spatial-temporal dependencies from PMU data to reconstruct missing values, and another auxiliary GNN utilizes the low-rank property of PMU data to achieve unsupervised online learning. In this way, the low-rank properties of the PMU data are dynamically leveraged across the architecture to ensure robustness and self-adaptation. Numerical results demonstrate the superior offline and online performance of the proposed method under high missing rates and incomplete observability.

ExARNN: An Environment-Driven Adaptive RNN for Learning Non-Stationary Power Dynamics

May 23, 2025Non-stationary power system dynamics, influenced by renewable energy variability, evolving demand patterns, and climate change, are becoming increasingly complex. Accurately capturing these dynamics requires a model capable of adapting to environmental factors. Traditional models, including Recurrent Neural Networks (RNNs), lack efficient mechanisms to encode external factors, such as time or environmental data, for dynamic adaptation. To address this, we propose the External Adaptive RNN (ExARNN), a novel framework that integrates external data (e.g., weather, time) to continuously adjust the parameters of a base RNN. ExARNN achieves this through a hierarchical hypernetwork design, using Neural Controlled Differential Equations (NCDE) to process external data and generate RNN parameters adaptively. This approach enables ExARNN to handle inconsistent timestamps between power and external measurements, ensuring continuous adaptation. Extensive forecasting tests demonstrate ExARNN's superiority over established baseline models.

Tilted Quantile Gradient Updates for Quantile-Constrained Reinforcement Learning

Dec 17, 2024Safe reinforcement learning (RL) is a popular and versatile paradigm to learn reward-maximizing policies with safety guarantees. Previous works tend to express the safety constraints in an expectation form due to the ease of implementation, but this turns out to be ineffective in maintaining safety constraints with high probability. To this end, we move to the quantile-constrained RL that enables a higher level of safety without any expectation-form approximations. We directly estimate the quantile gradients through sampling and provide the theoretical proofs of convergence. Then a tilted update strategy for quantile gradients is implemented to compensate the asymmetric distributional density, with a direct benefit of return performance. Experiments demonstrate that the proposed model fully meets safety requirements (quantile constraints) while outperforming the state-of-the-art benchmarks with higher return.

Explainable Modeling for Wind Power Forecasting: A Glass-Box Approach with Exceptional Accuracy

Oct 28, 2023

Machine learning models (e.g., neural networks) achieve high accuracy in wind power forecasting, but they are usually regarded as black boxes that lack interpretability. To address this issue, the paper proposes a glass-box approach that combines exceptional accuracy with transparency for wind power forecasting. Specifically, advanced artificial intelligence methods (e.g., gradient boosting) are innovatively employed to create shape functions within the forecasting model. These functions effectively map the intricate non-linear relationships between wind power output and input features. Furthermore, the forecasting model is enriched by incorporating interaction terms that adeptly capture interdependencies and synergies among the input features. Simulation results show that the proposed glass-box approach effectively interprets the results of wind power forecasting from both global and instance perspectives. Besides, it outperforms most benchmark models and exhibits comparable performance to the best-performing neural networks. This dual strength of transparency and high accuracy positions the proposed glass-box approach as a compelling choice for reliable wind power forecasting.

Improving Sample Efficiency of Deep Learning Models in Electricity Market

Oct 11, 2022

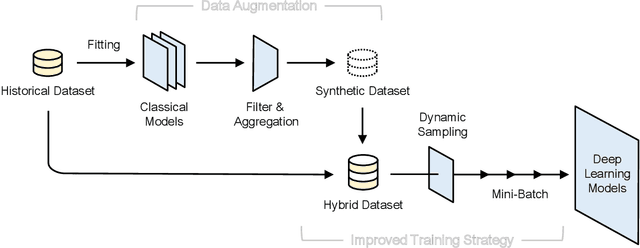

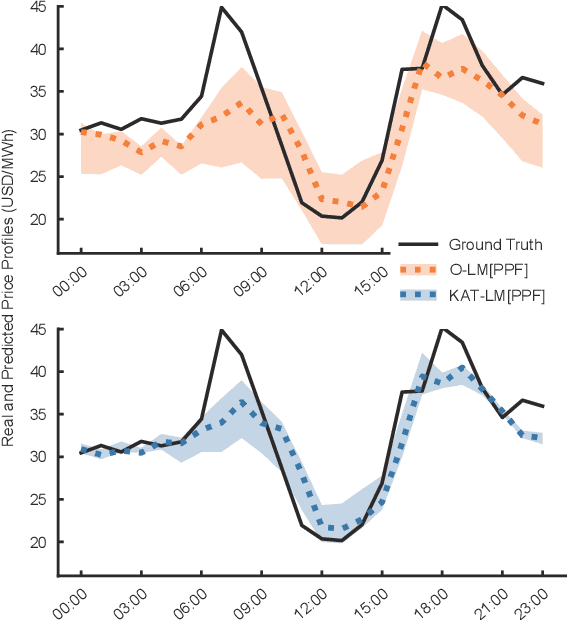

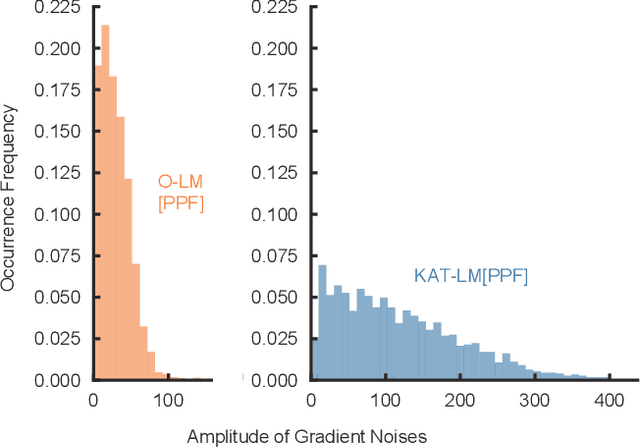

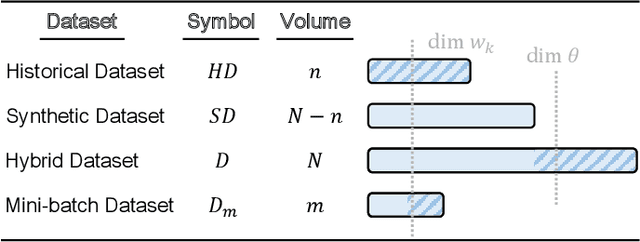

The superior performance of deep learning relies heavily on a large collection of sample data, but the data insufficiency problem turns out to be relatively common in global electricity markets. How to prevent overfitting in this case becomes a fundamental challenge when training deep learning models in different market applications. With this in mind, we propose a general framework, namely Knowledge-Augmented Training (KAT), to improve the sample efficiency, and the main idea is to incorporate domain knowledge into the training procedures of deep learning models. Specifically, we propose a novel data augmentation technique to generate some synthetic data, which are later processed by an improved training strategy. This KAT methodology follows and realizes the idea of combining analytical and deep learning models together. Modern learning theories demonstrate the effectiveness of our method in terms of effective prediction error feedbacks, a reliable loss function, and rich gradient noises. At last, we study two popular applications in detail: user modeling and probabilistic price forecasting. The proposed method outperforms other competitors in all numerical tests, and the underlying reasons are explained by further statistical and visualization results.

Evaluation of Look-ahead Economic Dispatch Using Reinforcement Learning

Sep 21, 2022

Modern power systems are experiencing a variety of challenges driven by renewable energy, which calls for developing novel dispatch methods such as reinforcement learning (RL). Evaluation of these methods as well as the RL agents are largely under explored. In this paper, we propose an evaluation approach to analyze the performance of RL agents in a look-ahead economic dispatch scheme. This approach is conducted by scanning multiple operational scenarios. In particular, a scenario generation method is developed to generate the network scenarios and demand scenarios for evaluation, and network structures are aggregated according to the change rates of power flow. Then several metrics are defined to evaluate the agents' performance from the perspective of economy and security. In the case study, we use a modified IEEE 30-bus system to illustrate the effectiveness of the proposed evaluation approach, and the simulation results reveal good and rapid adaptation to different scenarios. The comparison between different RL agents is also informative to offer advice for a better design of the learning strategies.

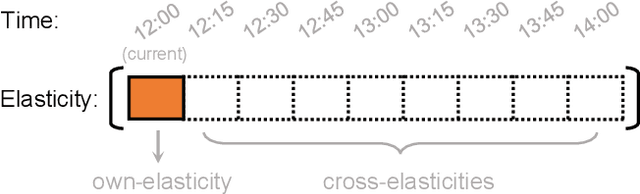

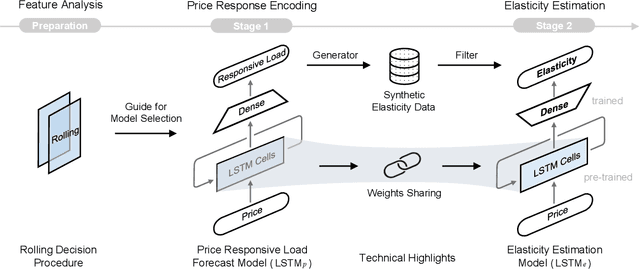

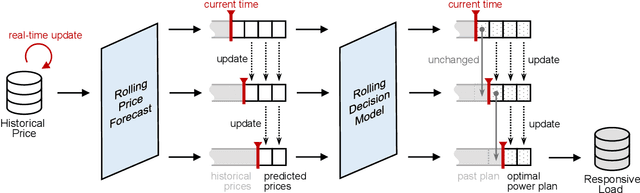

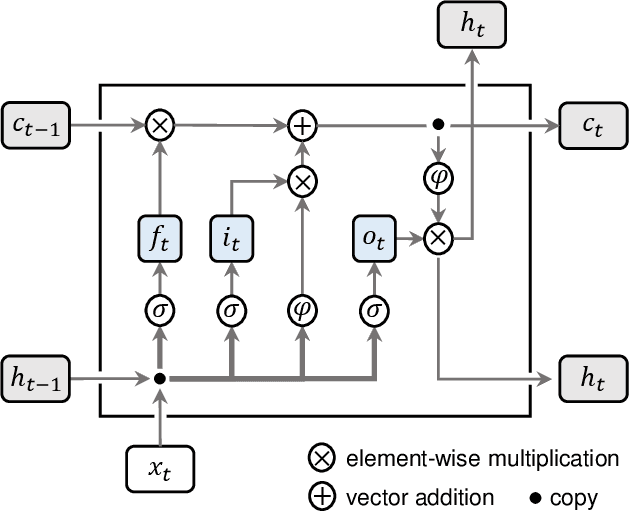

Estimating Demand Flexibility Using Siamese LSTM Neural Networks

Sep 03, 2021

There is an opportunity in modern power systems to explore the demand flexibility by incentivizing consumers with dynamic prices. In this paper, we quantify demand flexibility using an efficient tool called time-varying elasticity, whose value may change depending on the prices and decision dynamics. This tool is particularly useful for evaluating the demand response potential and system reliability. Recent empirical evidences have highlighted some abnormal features when studying demand flexibility, such as delayed responses and vanishing elasticities after price spikes. Existing methods fail to capture these complicated features because they heavily rely on some predefined (often over-simplified) regression expressions. Instead, this paper proposes a model-free methodology to automatically and accurately derive the optimal estimation pattern. We further develop a two-stage estimation process with Siamese long short-term memory (LSTM) networks. Here, a LSTM network encodes the price response, while the other network estimates the time-varying elasticities. In the case study, the proposed framework and models are validated to achieve higher overall estimation accuracy and better description for various abnormal features when compared with the state-of-the-art methods.

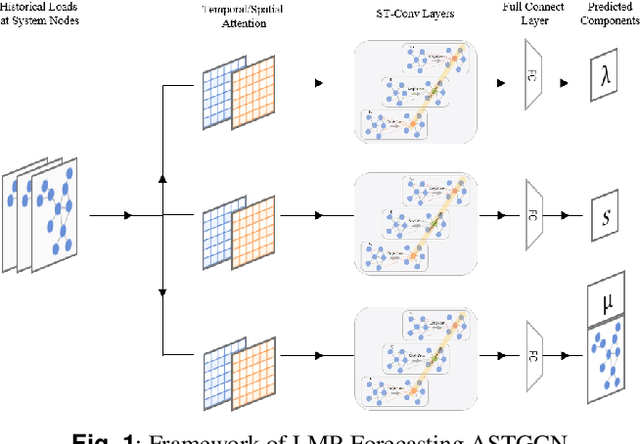

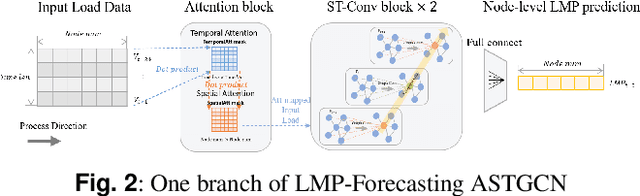

Short-Term Electricity Price Forecasting based on Graph Convolution Network and Attention Mechanism

Jul 26, 2021

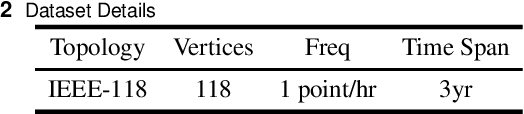

In electricity markets, locational marginal price (LMP) forecasting is particularly important for market participants in making reasonable bidding strategies, managing potential trading risks, and supporting efficient system planning and operation. Unlike existing methods that only consider LMPs' temporal features, this paper tailors a spectral graph convolutional network (GCN) to greatly improve the accuracy of short-term LMP forecasting. A three-branch network structure is then designed to match the structure of LMPs' compositions. Such kind of network can extract the spatial-temporal features of LMPs, and provide fast and high-quality predictions for all nodes simultaneously. The attention mechanism is also implemented to assign varying importance weights between different nodes and time slots. Case studies based on the IEEE-118 test system and real-world data from the PJM validate that the proposed model outperforms existing forecasting models in accuracy, and maintains a robust performance by avoiding extreme errors.