Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Graph Neural Network with Auxiliary Task Learning for Missing PMU Data Reconstruction

Dec 31, 2025In wide-area measurement systems (WAMS), phasor measurement unit (PMU) measurement is prone to data missingness due to hardware failures, communication delays, and cyber-attacks. Existing data-driven methods are limited by inadaptability to concept drift in power systems, poor robustness under high missing rates, and reliance on the unrealistic assumption of full system observability. Thus, this paper proposes an auxiliary task learning (ATL) method for reconstructing missing PMU data. First, a K-hop graph neural network (GNN) is proposed to enable direct learning on the subgraph consisting of PMU nodes, overcoming the limitation of the incompletely observable system. Then, an auxiliary learning framework consisting of two complementary graph networks is designed for accurate reconstruction: a spatial-temporal GNN extracts spatial-temporal dependencies from PMU data to reconstruct missing values, and another auxiliary GNN utilizes the low-rank property of PMU data to achieve unsupervised online learning. In this way, the low-rank properties of the PMU data are dynamically leveraged across the architecture to ensure robustness and self-adaptation. Numerical results demonstrate the superior offline and online performance of the proposed method under high missing rates and incomplete observability.

Reinforcement Learning Based Bidding Framework with High-dimensional Bids in Power Markets

Oct 15, 2024

Over the past decade, bidding in power markets has attracted widespread attention. Reinforcement Learning (RL) has been widely used for power market bidding as a powerful AI tool to make decisions under real-world uncertainties. However, current RL methods mostly employ low dimensional bids, which significantly diverge from the N price-power pairs commonly used in the current power markets. The N-pair bidding format is denoted as High Dimensional Bids (HDBs), which has not been fully integrated into the existing RL-based bidding methods. The loss of flexibility in current RL bidding methods could greatly limit the bidding profits and make it difficult to tackle the rising uncertainties brought by renewable energy generations. In this paper, we intend to propose a framework to fully utilize HDBs for RL-based bidding methods. First, we employ a special type of neural network called Neural Network Supply Functions (NNSFs) to generate HDBs in the form of N price-power pairs. Second, we embed the NNSF into a Markov Decision Process (MDP) to make it compatible with most existing RL methods. Finally, experiments on Energy Storage Systems (ESSs) in the PJM Real-Time (RT) power market show that the proposed bidding method with HDBs can significantly improve bidding flexibility, thereby improving the profit of the state-of-the-art RL bidding methods.

Misaka: Interactive Swarm Testbed for Smart Grid Distributed Algorithm Test and Evaluation

Apr 26, 2024In this paper, we present Misaka, a visualized swarm testbed for smart grid algorithm evaluation, also an extendable open-source open-hardware platform for developing tabletop tangible swarm interfaces. The platform consists of a collection of custom-designed 3 omni-directional wheels robots each 10 cm in diameter, high accuracy localization through a microdot pattern overlaid on top of the activity sheets, and a software framework for application development and control, while remaining affordable (per unit cost about 30 USD at the prototype stage). We illustrate the potential of tabletop swarm user interfaces through a set of smart grid algorithm application scenarios developed with Misaka.

Real-time scheduling of renewable power systems through planning-based reinforcement learning

Mar 13, 2023

The growing renewable energy sources have posed significant challenges to traditional power scheduling. It is difficult for operators to obtain accurate day-ahead forecasts of renewable generation, thereby requiring the future scheduling system to make real-time scheduling decisions aligning with ultra-short-term forecasts. Restricted by the computation speed, traditional optimization-based methods can not solve this problem. Recent developments in reinforcement learning (RL) have demonstrated the potential to solve this challenge. However, the existing RL methods are inadequate in terms of constraint complexity, algorithm performance, and environment fidelity. We are the first to propose a systematic solution based on the state-of-the-art reinforcement learning algorithm and the real power grid environment. The proposed approach enables planning and finer time resolution adjustments of power generators, including unit commitment and economic dispatch, thus increasing the grid's ability to admit more renewable energy. The well-trained scheduling agent significantly reduces renewable curtailment and load shedding, which are issues arising from traditional scheduling's reliance on inaccurate day-ahead forecasts. High-frequency control decisions exploit the existing units' flexibility, reducing the power grid's dependence on hardware transformations and saving investment and operating costs, as demonstrated in experimental results. This research exhibits the potential of reinforcement learning in promoting low-carbon and intelligent power systems and represents a solid step toward sustainable electricity generation.

Improving Sample Efficiency of Deep Learning Models in Electricity Market

Oct 11, 2022

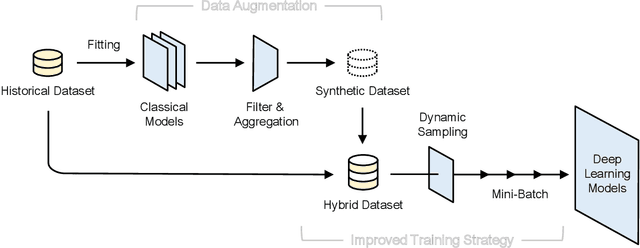

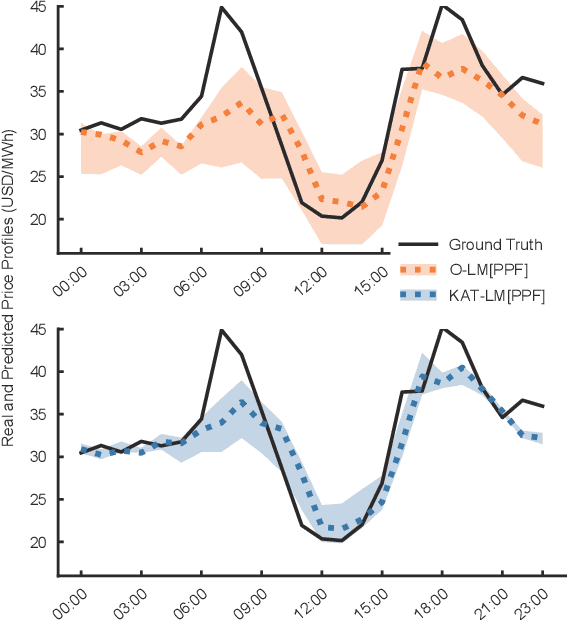

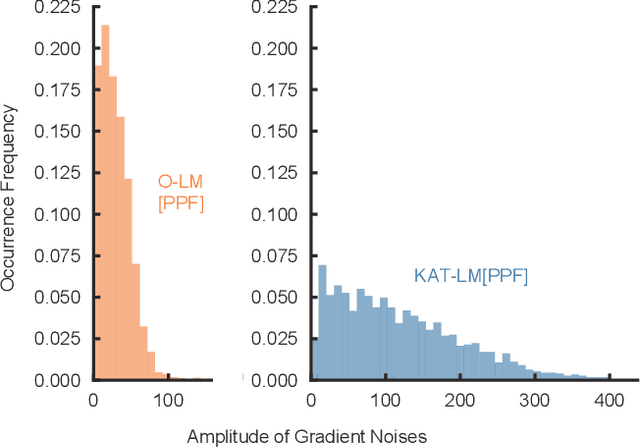

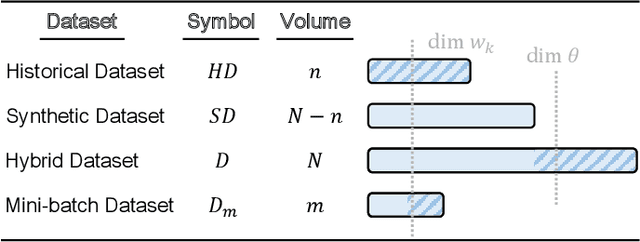

The superior performance of deep learning relies heavily on a large collection of sample data, but the data insufficiency problem turns out to be relatively common in global electricity markets. How to prevent overfitting in this case becomes a fundamental challenge when training deep learning models in different market applications. With this in mind, we propose a general framework, namely Knowledge-Augmented Training (KAT), to improve the sample efficiency, and the main idea is to incorporate domain knowledge into the training procedures of deep learning models. Specifically, we propose a novel data augmentation technique to generate some synthetic data, which are later processed by an improved training strategy. This KAT methodology follows and realizes the idea of combining analytical and deep learning models together. Modern learning theories demonstrate the effectiveness of our method in terms of effective prediction error feedbacks, a reliable loss function, and rich gradient noises. At last, we study two popular applications in detail: user modeling and probabilistic price forecasting. The proposed method outperforms other competitors in all numerical tests, and the underlying reasons are explained by further statistical and visualization results.

Evaluation of Look-ahead Economic Dispatch Using Reinforcement Learning

Sep 21, 2022

Modern power systems are experiencing a variety of challenges driven by renewable energy, which calls for developing novel dispatch methods such as reinforcement learning (RL). Evaluation of these methods as well as the RL agents are largely under explored. In this paper, we propose an evaluation approach to analyze the performance of RL agents in a look-ahead economic dispatch scheme. This approach is conducted by scanning multiple operational scenarios. In particular, a scenario generation method is developed to generate the network scenarios and demand scenarios for evaluation, and network structures are aggregated according to the change rates of power flow. Then several metrics are defined to evaluate the agents' performance from the perspective of economy and security. In the case study, we use a modified IEEE 30-bus system to illustrate the effectiveness of the proposed evaluation approach, and the simulation results reveal good and rapid adaptation to different scenarios. The comparison between different RL agents is also informative to offer advice for a better design of the learning strategies.

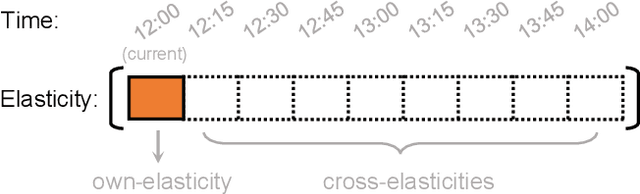

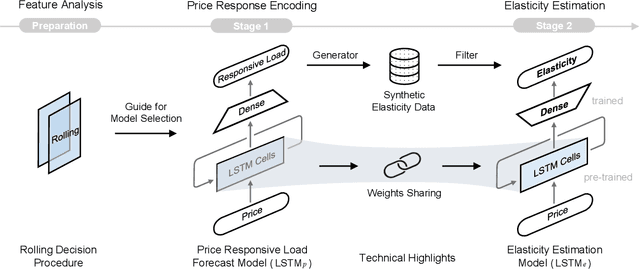

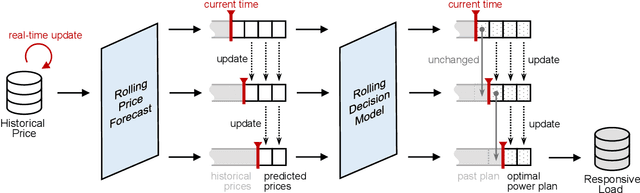

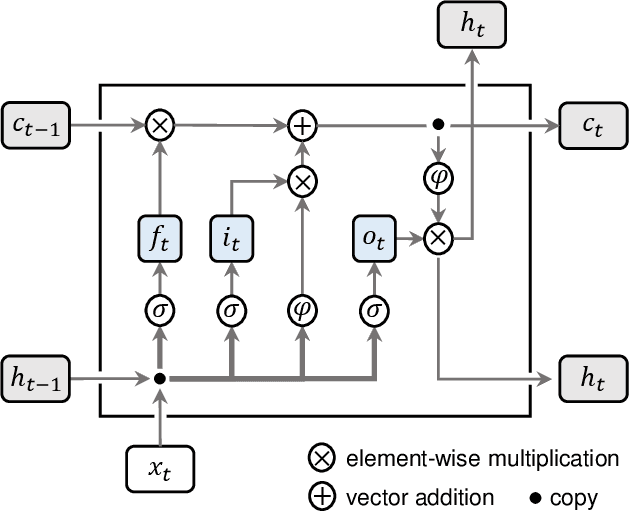

Estimating Demand Flexibility Using Siamese LSTM Neural Networks

Sep 03, 2021

There is an opportunity in modern power systems to explore the demand flexibility by incentivizing consumers with dynamic prices. In this paper, we quantify demand flexibility using an efficient tool called time-varying elasticity, whose value may change depending on the prices and decision dynamics. This tool is particularly useful for evaluating the demand response potential and system reliability. Recent empirical evidences have highlighted some abnormal features when studying demand flexibility, such as delayed responses and vanishing elasticities after price spikes. Existing methods fail to capture these complicated features because they heavily rely on some predefined (often over-simplified) regression expressions. Instead, this paper proposes a model-free methodology to automatically and accurately derive the optimal estimation pattern. We further develop a two-stage estimation process with Siamese long short-term memory (LSTM) networks. Here, a LSTM network encodes the price response, while the other network estimates the time-varying elasticities. In the case study, the proposed framework and models are validated to achieve higher overall estimation accuracy and better description for various abnormal features when compared with the state-of-the-art methods.

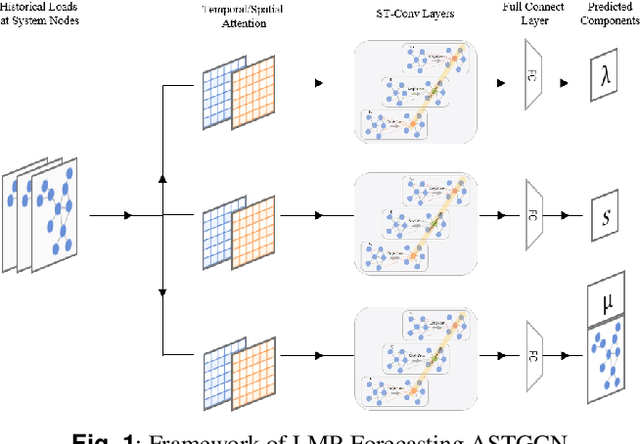

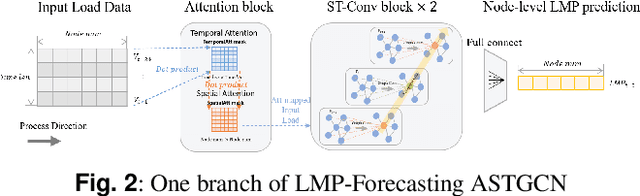

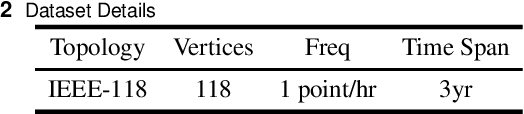

Short-Term Electricity Price Forecasting based on Graph Convolution Network and Attention Mechanism

Jul 26, 2021

In electricity markets, locational marginal price (LMP) forecasting is particularly important for market participants in making reasonable bidding strategies, managing potential trading risks, and supporting efficient system planning and operation. Unlike existing methods that only consider LMPs' temporal features, this paper tailors a spectral graph convolutional network (GCN) to greatly improve the accuracy of short-term LMP forecasting. A three-branch network structure is then designed to match the structure of LMPs' compositions. Such kind of network can extract the spatial-temporal features of LMPs, and provide fast and high-quality predictions for all nodes simultaneously. The attention mechanism is also implemented to assign varying importance weights between different nodes and time slots. Case studies based on the IEEE-118 test system and real-world data from the PJM validate that the proposed model outperforms existing forecasting models in accuracy, and maintains a robust performance by avoiding extreme errors.