Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Unifying View of Coverage in Linear Off-Policy Evaluation

Jan 26, 2026Off-policy evaluation (OPE) is a fundamental task in reinforcement learning (RL). In the classic setting of linear OPE, finite-sample guarantees often take the form $$ \textrm{Evaluation error} \le \textrm{poly}(C^π, d, 1/n,\log(1/δ)), $$ where $d$ is the dimension of the features and $C^π$ is a coverage parameter that characterizes the degree to which the visited features lie in the span of the data distribution. While such guarantees are well-understood for several popular algorithms under stronger assumptions (e.g. Bellman completeness), the understanding is lacking and fragmented in the minimal setting where only the target value function is linearly realizable in the features. Despite recent interest in tight characterizations of the statistical rate in this setting, the right notion of coverage remains unclear, and candidate definitions from prior analyses have undesirable properties and are starkly disconnected from more standard definitions in the literature. We provide a novel finite-sample analysis of a canonical algorithm for this setting, LSTDQ. Inspired by an instrumental-variable view, we develop error bounds that depend on a novel coverage parameter, the feature-dynamics coverage, which can be interpreted as linear coverage in an induced dynamical system for feature evolution. With further assumptions -- such as Bellman-completeness -- our definition successfully recovers the coverage parameters specialized to those settings, finally yielding a unified understanding for coverage in linear OPE.

Is Best-of-N the Best of Them? Coverage, Scaling, and Optimality in Inference-Time Alignment

Mar 27, 2025

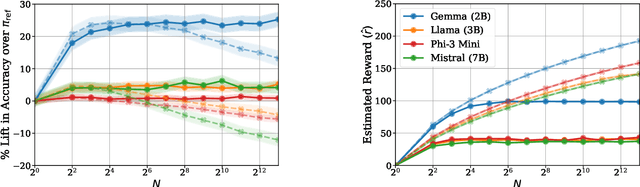

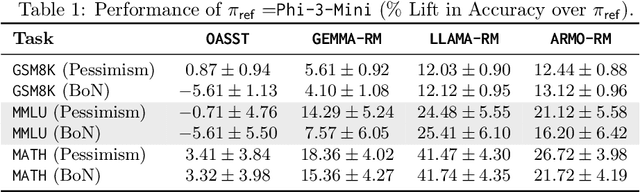

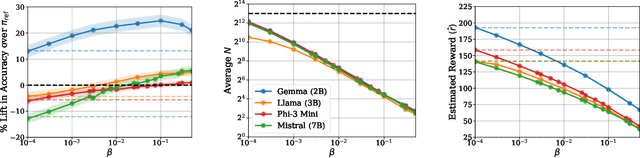

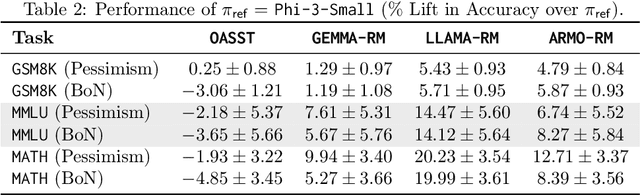

Inference-time computation provides an important axis for scaling language model performance, but naively scaling compute through techniques like Best-of-$N$ sampling can cause performance to degrade due to reward hacking. Toward a theoretical understanding of how to best leverage additional computation, we focus on inference-time alignment which we formalize as the problem of improving a pre-trained policy's responses for a prompt of interest, given access to an imperfect reward model. We analyze the performance of inference-time alignment algorithms in terms of (i) response quality, and (ii) compute, and provide new results that highlight the importance of the pre-trained policy's coverage over high-quality responses for performance and compute scaling: 1. We show that Best-of-$N$ alignment with an ideal choice for $N$ can achieve optimal performance under stringent notions of coverage, but provably suffers from reward hacking when $N$ is large, and fails to achieve tight guarantees under more realistic coverage conditions. 2. We introduce $\texttt{InferenceTimePessimism}$, a new algorithm which mitigates reward hacking through deliberate use of inference-time compute, implementing the principle of pessimism in the face of uncertainty via rejection sampling; we prove that its performance is optimal and does not degrade with $N$, meaning it is scaling-monotonic. We complement our theoretical results with an experimental evaluation that demonstrate the benefits of $\texttt{InferenceTimePessimism}$ across a variety of tasks and models.

Computational-Statistical Tradeoffs at the Next-Token Prediction Barrier: Autoregressive and Imitation Learning under Misspecification

Feb 18, 2025Next-token prediction with the logarithmic loss is a cornerstone of autoregressive sequence modeling, but, in practice, suffers from error amplification, where errors in the model compound and generation quality degrades as sequence length $H$ increases. From a theoretical perspective, this phenomenon should not appear in well-specified settings, and, indeed, a growing body of empirical work hypothesizes that misspecification, where the learner is not sufficiently expressive to represent the target distribution, may be the root cause. Under misspecification -- where the goal is to learn as well as the best-in-class model up to a multiplicative approximation factor $C\geq 1$ -- we confirm that $C$ indeed grows with $H$ for next-token prediction, lending theoretical support to this empirical hypothesis. We then ask whether this mode of error amplification is avoidable algorithmically, computationally, or information-theoretically, and uncover inherent computational-statistical tradeoffs. We show: (1) Information-theoretically, one can avoid error amplification and achieve $C=O(1)$. (2) Next-token prediction can be made robust so as to achieve $C=\tilde O(H)$, representing moderate error amplification, but this is an inherent barrier: any next-token prediction-style objective must suffer $C=\Omega(H)$. (3) For the natural testbed of autoregressive linear models, no computationally efficient algorithm can achieve sub-polynomial approximation factor $C=e^{(\log H)^{1-\Omega(1)}}$; however, at least for binary token spaces, one can smoothly trade compute for statistical power and improve on $C=\Omega(H)$ in sub-exponential time. Our results have consequences in the more general setting of imitation learning, where the widely-used behavior cloning algorithm generalizes next-token prediction.

Model Selection for Off-policy Evaluation: New Algorithms and Experimental Protocol

Feb 11, 2025

Holdout validation and hyperparameter tuning from data is a long-standing problem in offline reinforcement learning (RL). A standard framework is to use off-policy evaluation (OPE) methods to evaluate and select the policies, but OPE either incurs exponential variance (e.g., importance sampling) or has hyperparameters on their own (e.g., FQE and model-based). In this work we focus on hyperparameter tuning for OPE itself, which is even more under-investigated. Concretely, we select among candidate value functions ("model-free") or dynamics ("model-based") to best assess the performance of a target policy. Our contributions are two fold. We develop: (1) new model-free and model-based selectors with theoretical guarantees, and (2) a new experimental protocol for empirically evaluating them. Compared to the model-free protocol in prior works, our new protocol allows for more stable generation of candidate value functions, better control of misspecification, and evaluation of model-free and model-based methods alike. We exemplify the protocol on a Gym environment, and find that our new model-free selector, LSTD-Tournament, demonstrates promising empirical performance.

Self-Improvement in Language Models: The Sharpening Mechanism

Dec 02, 2024Recent work in language modeling has raised the possibility of self-improvement, where a language models evaluates and refines its own generations to achieve higher performance without external feedback. It is impossible for this self-improvement to create information that is not already in the model, so why should we expect that this will lead to improved capabilities? We offer a new perspective on the capabilities of self-improvement through a lens we refer to as sharpening. Motivated by the observation that language models are often better at verifying response quality than they are at generating correct responses, we formalize self-improvement as using the model itself as a verifier during post-training in order to ``sharpen'' the model to one placing large mass on high-quality sequences, thereby amortizing the expensive inference-time computation of generating good sequences. We begin by introducing a new statistical framework for sharpening in which the learner aims to sharpen a pre-trained base policy via sample access, and establish fundamental limits. Then we analyze two natural families of self-improvement algorithms based on SFT and RLHF.

Correcting the Mythos of KL-Regularization: Direct Alignment without Overparameterization via Chi-squared Preference Optimization

Jul 18, 2024

Language model alignment methods, such as reinforcement learning from human feedback (RLHF), have led to impressive advances in language model capabilities, but existing techniques are limited by a widely observed phenomenon known as overoptimization, where the quality of the language model plateaus or degrades over the course of the alignment process. Overoptimization is often attributed to overfitting to an inaccurate reward model, and while it can be mitigated through online data collection, this is infeasible in many settings. This raises a fundamental question: Do existing offline alignment algorithms make the most of the data they have, or can their sample-efficiency be improved further? We address this question with a new algorithm for offline alignment, $\chi^2$-Preference Optimization ($\chi$PO). $\chi$PO is a one-line change to Direct Preference Optimization (DPO; Rafailov et al., 2023), which only involves modifying the logarithmic link function in the DPO objective. Despite this minimal change, $\chi$PO implicitly implements the principle of pessimism in the face of uncertainty via regularization with the $\chi^2$-divergence -- which quantifies uncertainty more effectively than KL-regularization -- and provably alleviates overoptimization, achieving sample-complexity guarantees based on single-policy concentrability -- the gold standard in offline reinforcement learning. $\chi$PO's simplicity and strong guarantees make it the first practical and general-purpose offline alignment algorithm that is provably robust to overoptimization.

Reinforcement Learning in Low-Rank MDPs with Density Features

Feb 04, 2023MDPs with low-rank transitions -- that is, the transition matrix can be factored into the product of two matrices, left and right -- is a highly representative structure that enables tractable learning. The left matrix enables expressive function approximation for value-based learning and has been studied extensively. In this work, we instead investigate sample-efficient learning with density features, i.e., the right matrix, which induce powerful models for state-occupancy distributions. This setting not only sheds light on leveraging unsupervised learning in RL, but also enables plug-in solutions for convex RL. In the offline setting, we propose an algorithm for off-policy estimation of occupancies that can handle non-exploratory data. Using this as a subroutine, we further devise an online algorithm that constructs exploratory data distributions in a level-by-level manner. As a central technical challenge, the additive error of occupancy estimation is incompatible with the multiplicative definition of data coverage. In the absence of strong assumptions like reachability, this incompatibility easily leads to exponential error blow-up, which we overcome via novel technical tools. Our results also readily extend to the representation learning setting, when the density features are unknown and must be learned from an exponentially large candidate set.

Beyond the Return: Off-policy Function Estimation under User-specified Error-measuring Distributions

Oct 27, 2022Off-policy evaluation often refers to two related tasks: estimating the expected return of a policy and estimating its value function (or other functions of interest, such as density ratios). While recent works on marginalized importance sampling (MIS) show that the former can enjoy provable guarantees under realizable function approximation, the latter is only known to be feasible under much stronger assumptions such as prohibitively expressive discriminators. In this work, we provide guarantees for off-policy function estimation under only realizability, by imposing proper regularization on the MIS objectives. Compared to commonly used regularization in MIS, our regularizer is much more flexible and can account for an arbitrary user-specified distribution, under which the learned function will be close to the groundtruth. We provide exact characterization of the optimal dual solution that needs to be realized by the discriminator class, which determines the data-coverage assumption in the case of value-function learning. As another surprising observation, the regularizer can be altered to relax the data-coverage requirement, and completely eliminate it in the ideal case with strong side information.

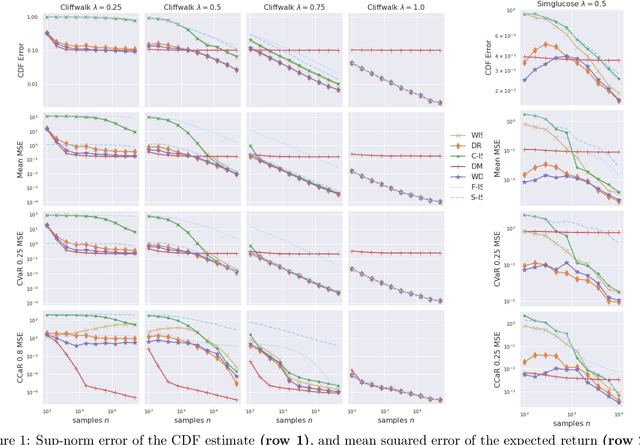

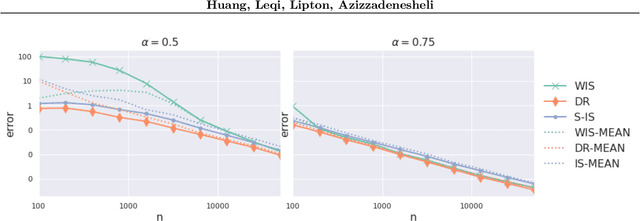

Off-Policy Risk Assessment in Markov Decision Processes

Sep 21, 2022

Addressing such diverse ends as safety alignment with human preferences, and the efficiency of learning, a growing line of reinforcement learning research focuses on risk functionals that depend on the entire distribution of returns. Recent work on \emph{off-policy risk assessment} (OPRA) for contextual bandits introduced consistent estimators for the target policy's CDF of returns along with finite sample guarantees that extend to (and hold simultaneously over) all risk. In this paper, we lift OPRA to Markov decision processes (MDPs), where importance sampling (IS) CDF estimators suffer high variance on longer trajectories due to small effective sample size. To mitigate these problems, we incorporate model-based estimation to develop the first doubly robust (DR) estimator for the CDF of returns in MDPs. This estimator enjoys significantly less variance and, when the model is well specified, achieves the Cramer-Rao variance lower bound. Moreover, for many risk functionals, the downstream estimates enjoy both lower bias and lower variance. Additionally, we derive the first minimax lower bounds for off-policy CDF and risk estimation, which match our error bounds up to a constant factor. Finally, we demonstrate the precision of our DR CDF estimates experimentally on several different environments.

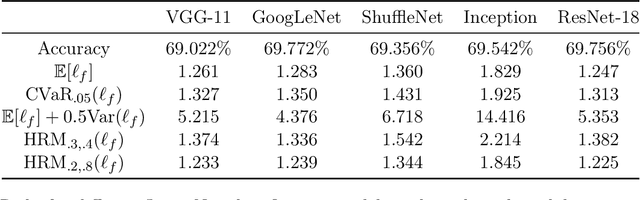

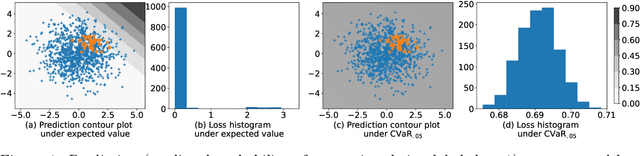

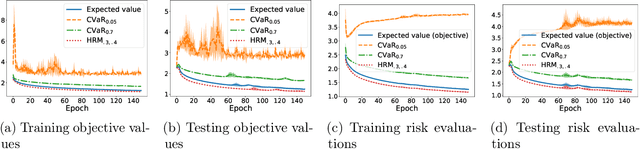

Supervised Learning with General Risk Functionals

Jun 27, 2022

Standard uniform convergence results bound the generalization gap of the expected loss over a hypothesis class. The emergence of risk-sensitive learning requires generalization guarantees for functionals of the loss distribution beyond the expectation. While prior works specialize in uniform convergence of particular functionals, our work provides uniform convergence for a general class of H\"older risk functionals for which the closeness in the Cumulative Distribution Function (CDF) entails closeness in risk. We establish the first uniform convergence results for estimating the CDF of the loss distribution, yielding guarantees that hold simultaneously both over all H\"older risk functionals and over all hypotheses. Thus licensed to perform empirical risk minimization, we develop practical gradient-based methods for minimizing distortion risks (widely studied subset of H\"older risks that subsumes the spectral risks, including the mean, conditional value at risk, cumulative prospect theory risks, and others) and provide convergence guarantees. In experiments, we demonstrate the efficacy of our learning procedure, both in settings where uniform convergence results hold and in high-dimensional settings with deep networks.