Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGolden Touchstone: A Comprehensive Bilingual Benchmark for Evaluating Financial Large Language Models

Nov 09, 2024

As large language models become increasingly prevalent in the financial sector, there is a pressing need for a standardized method to comprehensively assess their performance. However, existing finance benchmarks often suffer from limited language and task coverage, as well as challenges such as low-quality datasets and inadequate adaptability for LLM evaluation. To address these limitations, we propose "Golden Touchstone", the first comprehensive bilingual benchmark for financial LLMs, which incorporates representative datasets from both Chinese and English across eight core financial NLP tasks. Developed from extensive open source data collection and industry-specific demands, this benchmark includes a variety of financial tasks aimed at thoroughly assessing models' language understanding and generation capabilities. Through comparative analysis of major models on the benchmark, such as GPT-4o Llama3, FinGPT and FinMA, we reveal their strengths and limitations in processing complex financial information. Additionally, we open-sourced Touchstone-GPT, a financial LLM trained through continual pre-training and financial instruction tuning, which demonstrates strong performance on the bilingual benchmark but still has limitations in specific tasks.This research not only provides the financial large language models with a practical evaluation tool but also guides the development and optimization of future research. The source code for Golden Touchstone and model weight of Touchstone-GPT have been made publicly available at \url{https://github.com/IDEA-FinAI/Golden-Touchstone}, contributing to the ongoing evolution of FinLLMs and fostering further research in this critical area.

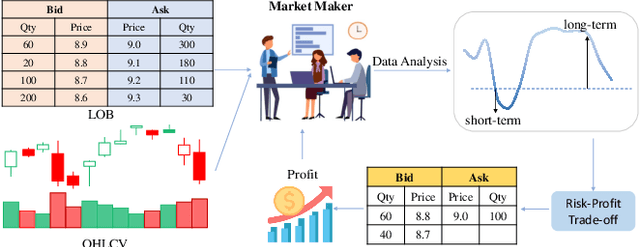

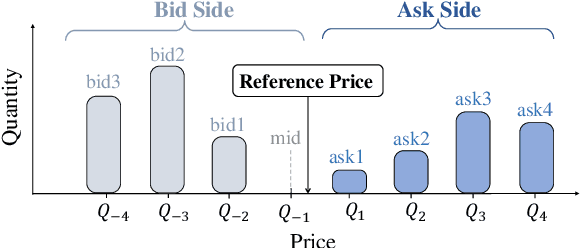

IMM: An Imitative Reinforcement Learning Approach with Predictive Representation Learning for Automatic Market Making

Aug 17, 2023

Market making (MM) has attracted significant attention in financial trading owing to its essential function in ensuring market liquidity. With strong capabilities in sequential decision-making, Reinforcement Learning (RL) technology has achieved remarkable success in quantitative trading. Nonetheless, most existing RL-based MM methods focus on optimizing single-price level strategies which fail at frequent order cancellations and loss of queue priority. Strategies involving multiple price levels align better with actual trading scenarios. However, given the complexity that multi-price level strategies involves a comprehensive trading action space, the challenge of effectively training profitable RL agents for MM persists. Inspired by the efficient workflow of professional human market makers, we propose Imitative Market Maker (IMM), a novel RL framework leveraging both knowledge from suboptimal signal-based experts and direct policy interactions to develop multi-price level MM strategies efficiently. The framework start with introducing effective state and action representations adept at encoding information about multi-price level orders. Furthermore, IMM integrates a representation learning unit capable of capturing both short- and long-term market trends to mitigate adverse selection risk. Subsequently, IMM formulates an expert strategy based on signals and trains the agent through the integration of RL and imitation learning techniques, leading to efficient learning. Extensive experimental results on four real-world market datasets demonstrate that IMM outperforms current RL-based market making strategies in terms of several financial criteria. The findings of the ablation study substantiate the effectiveness of the model components.