Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeIMM: An Imitative Reinforcement Learning Approach with Predictive Representation Learning for Automatic Market Making

Aug 17, 2023

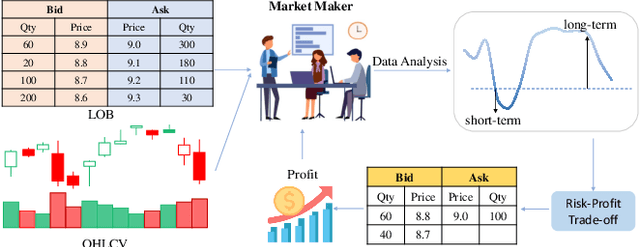

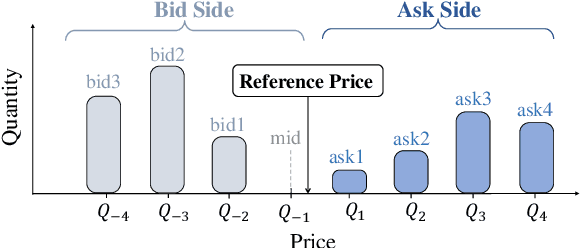

Market making (MM) has attracted significant attention in financial trading owing to its essential function in ensuring market liquidity. With strong capabilities in sequential decision-making, Reinforcement Learning (RL) technology has achieved remarkable success in quantitative trading. Nonetheless, most existing RL-based MM methods focus on optimizing single-price level strategies which fail at frequent order cancellations and loss of queue priority. Strategies involving multiple price levels align better with actual trading scenarios. However, given the complexity that multi-price level strategies involves a comprehensive trading action space, the challenge of effectively training profitable RL agents for MM persists. Inspired by the efficient workflow of professional human market makers, we propose Imitative Market Maker (IMM), a novel RL framework leveraging both knowledge from suboptimal signal-based experts and direct policy interactions to develop multi-price level MM strategies efficiently. The framework start with introducing effective state and action representations adept at encoding information about multi-price level orders. Furthermore, IMM integrates a representation learning unit capable of capturing both short- and long-term market trends to mitigate adverse selection risk. Subsequently, IMM formulates an expert strategy based on signals and trains the agent through the integration of RL and imitation learning techniques, leading to efficient learning. Extensive experimental results on four real-world market datasets demonstrate that IMM outperforms current RL-based market making strategies in terms of several financial criteria. The findings of the ablation study substantiate the effectiveness of the model components.

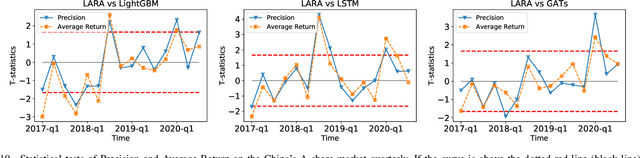

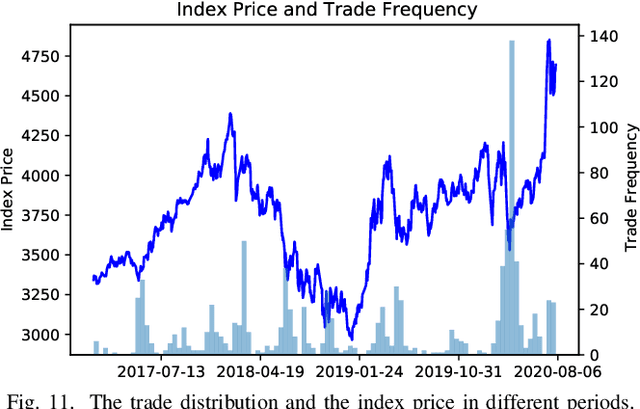

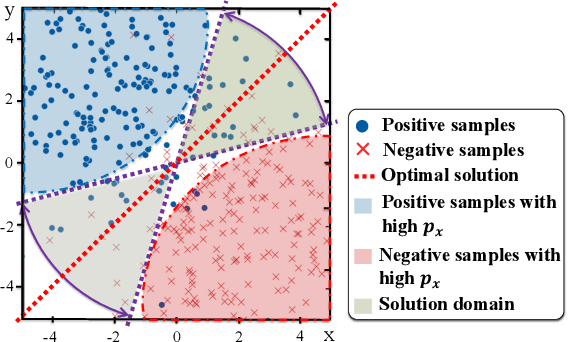

Trade When Opportunity Comes: Price Movement Forecasting via Locality-Aware Attention and Adaptive Refined Labeling

Jul 26, 2021

Price movement forecasting aims at predicting the future trends of financial assets based on the current market conditions and other relevant information. Recently, machine learning(ML) methods have become increasingly popular and achieved promising results for price movement forecasting in both academia and industry. Most existing ML solutions formulate the forecasting problem as a classification(to predict the direction) or a regression(to predict the return) problem in the entire set of training data. However, due to the extremely low signal-to-noise ratio and stochastic nature of financial data, good trading opportunities are extremely scarce. As a result, without careful selection of potentially profitable samples, such ML methods are prone to capture the patterns of noises instead of real signals. To address the above issues, we propose a novel framework-LARA(Locality-Aware Attention and Adaptive Refined Labeling), which contains the following three components: 1)Locality-aware attention automatically extracts the potentially profitable samples by attending to their label information in order to construct a more accurate classifier on these selected samples. 2)Adaptive refined labeling further iteratively refines the labels, alleviating the noise of samples. 3)Equipped with metric learning techniques, Locality-aware attention enjoys task-specific distance metrics and distributes attention on potentially profitable samples in a more effective way. To validate our method, we conduct comprehensive experiments on three real-world financial markets: ETFs, the China's A-share stock market, and the cryptocurrency market. LARA achieves superior performance compared with the time-series analysis methods and a set of machine learning based competitors on the Qlib platform. Extensive ablation studies and experiments demonstrate that LARA indeed captures more reliable trading opportunities.