Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNTIRE 2025 challenge on Text to Image Generation Model Quality Assessment

May 22, 2025This paper reports on the NTIRE 2025 challenge on Text to Image (T2I) generation model quality assessment, which will be held in conjunction with the New Trends in Image Restoration and Enhancement Workshop (NTIRE) at CVPR 2025. The aim of this challenge is to address the fine-grained quality assessment of text-to-image generation models. This challenge evaluates text-to-image models from two aspects: image-text alignment and image structural distortion detection, and is divided into the alignment track and the structural track. The alignment track uses the EvalMuse-40K, which contains around 40K AI-Generated Images (AIGIs) generated by 20 popular generative models. The alignment track has a total of 371 registered participants. A total of 1,883 submissions are received in the development phase, and 507 submissions are received in the test phase. Finally, 12 participating teams submitted their models and fact sheets. The structure track uses the EvalMuse-Structure, which contains 10,000 AI-Generated Images (AIGIs) with corresponding structural distortion mask. A total of 211 participants have registered in the structure track. A total of 1155 submissions are received in the development phase, and 487 submissions are received in the test phase. Finally, 8 participating teams submitted their models and fact sheets. Almost all methods have achieved better results than baseline methods, and the winning methods in both tracks have demonstrated superior prediction performance on T2I model quality assessment.

An Evaluation Framework for Product Images Background Inpainting based on Human Feedback and Product Consistency

Dec 24, 2024

In product advertising applications, the automated inpainting of backgrounds utilizing AI techniques in product images has emerged as a significant task. However, the techniques still suffer from issues such as inappropriate background and inconsistent product in generated product images, and existing approaches for evaluating the quality of generated product images are mostly inconsistent with human feedback causing the evaluation for this task to depend on manual annotation. To relieve the issues above, this paper proposes Human Feedback and Product Consistency (HFPC), which can automatically assess the generated product images based on two modules. Firstly, to solve inappropriate backgrounds, human feedback on 44,000 automated inpainting product images is collected to train a reward model based on multi-modal features extracted from BLIP and comparative learning. Secondly, to filter generated product images containing inconsistent products, a fine-tuned segmentation model is employed to segment the product of the original and generated product images and then compare the differences between the above two. Extensive experiments have demonstrated that HFPC can effectively evaluate the quality of generated product images and significantly reduce the expense of manual annotation. Moreover, HFPC achieves state-of-the-art(96.4% in precision) in comparison to other open-source visual-quality-assessment models. Dataset and code are available at: https://github.com/created-Bi/background_inpainting_products_dataset

Complete Instances Mining for Weakly Supervised Instance Segmentation

Feb 12, 2024

Weakly supervised instance segmentation (WSIS) using only image-level labels is a challenging task due to the difficulty of aligning coarse annotations with the finer task. However, with the advancement of deep neural networks (DNNs), WSIS has garnered significant attention. Following a proposal-based paradigm, we encounter a redundant segmentation problem resulting from a single instance being represented by multiple proposals. For example, we feed a picture of a dog and proposals into the network and expect to output only one proposal containing a dog, but the network outputs multiple proposals. To address this problem, we propose a novel approach for WSIS that focuses on the online refinement of complete instances through the use of MaskIoU heads to predict the integrity scores of proposals and a Complete Instances Mining (CIM) strategy to explicitly model the redundant segmentation problem and generate refined pseudo labels. Our approach allows the network to become aware of multiple instances and complete instances, and we further improve its robustness through the incorporation of an Anti-noise strategy. Empirical evaluations on the PASCAL VOC 2012 and MS COCO datasets demonstrate that our method achieves state-of-the-art performance with a notable margin. Our implementation will be made available at https://github.com/ZechengLi19/CIM.

* 7 pages

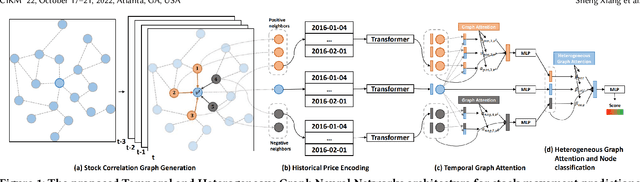

Temporal and Heterogeneous Graph Neural Network for Financial Time Series Prediction

May 09, 2023

The price movement prediction of stock market has been a classical yet challenging problem, with the attention of both economists and computer scientists. In recent years, graph neural network has significantly improved the prediction performance by employing deep learning on company relations. However, existing relation graphs are usually constructed by handcraft human labeling or nature language processing, which are suffering from heavy resource requirement and low accuracy. Besides, they cannot effectively response to the dynamic changes in relation graphs. Therefore, in this paper, we propose a temporal and heterogeneous graph neural network-based (THGNN) approach to learn the dynamic relations among price movements in financial time series. In particular, we first generate the company relation graph for each trading day according to their historic price. Then we leverage a transformer encoder to encode the price movement information into temporal representations. Afterward, we propose a heterogeneous graph attention network to jointly optimize the embeddings of the financial time series data by transformer encoder and infer the probability of target movements. Finally, we conduct extensive experiments on the stock market in the United States and China. The results demonstrate the effectiveness and superior performance of our proposed methods compared with state-of-the-art baselines. Moreover, we also deploy the proposed THGNN in a real-world quantitative algorithm trading system, the accumulated portfolio return obtained by our method significantly outperforms other baselines.