Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEvery Image Listens, Every Image Dances: Music-Driven Image Animation

Jan 30, 2025

Image animation has become a promising area in multimodal research, with a focus on generating videos from reference images. While prior work has largely emphasized generic video generation guided by text, music-driven dance video generation remains underexplored. In this paper, we introduce MuseDance, an innovative end-to-end model that animates reference images using both music and text inputs. This dual input enables MuseDance to generate personalized videos that follow text descriptions and synchronize character movements with the music. Unlike existing approaches, MuseDance eliminates the need for complex motion guidance inputs, such as pose or depth sequences, making flexible and creative video generation accessible to users of all expertise levels. To advance research in this field, we present a new multimodal dataset comprising 2,904 dance videos with corresponding background music and text descriptions. Our approach leverages diffusion-based methods to achieve robust generalization, precise control, and temporal consistency, setting a new baseline for the music-driven image animation task.

Online Nonconvex Bilevel Optimization with Bregman Divergences

Sep 16, 2024Bilevel optimization methods are increasingly relevant within machine learning, especially for tasks such as hyperparameter optimization and meta-learning. Compared to the offline setting, online bilevel optimization (OBO) offers a more dynamic framework by accommodating time-varying functions and sequentially arriving data. This study addresses the online nonconvex-strongly convex bilevel optimization problem. In deterministic settings, we introduce a novel online Bregman bilevel optimizer (OBBO) that utilizes adaptive Bregman divergences. We demonstrate that OBBO enhances the known sublinear rates for bilevel local regret through a novel hypergradient error decomposition that adapts to the underlying geometry of the problem. In stochastic contexts, we introduce the first stochastic online bilevel optimizer (SOBBO), which employs a window averaging method for updating outer-level variables using a weighted average of recent stochastic approximations of hypergradients. This approach not only achieves sublinear rates of bilevel local regret but also serves as an effective variance reduction strategy, obviating the need for additional stochastic gradient samples at each timestep. Experiments on online hyperparameter optimization and online meta-learning highlight the superior performance, efficiency, and adaptability of our Bregman-based algorithms compared to established online and offline bilevel benchmarks.

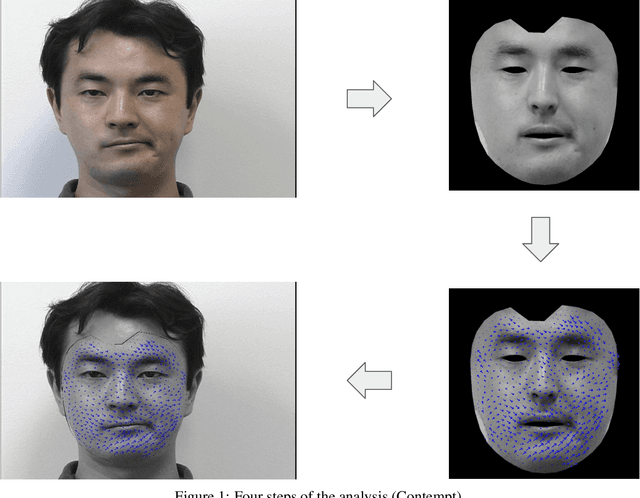

Face-GPS: A Comprehensive Technique for Quantifying Facial Muscle Dynamics in Videos

Jan 11, 2024We introduce a novel method that combines differential geometry, kernels smoothing, and spectral analysis to quantify facial muscle activity from widely accessible video recordings, such as those captured on personal smartphones. Our approach emphasizes practicality and accessibility. It has significant potential for applications in national security and plastic surgery. Additionally, it offers remote diagnosis and monitoring for medical conditions such as stroke, Bell's palsy, and acoustic neuroma. Moreover, it is adept at detecting and classifying emotions, from the overt to the subtle. The proposed face muscle analysis technique is an explainable alternative to deep learning methods and a non-invasive substitute to facial electromyography (fEMG).

MuseChat: A Conversational Music Recommendation System for Videos

Oct 11, 2023

We introduce MuseChat, an innovative dialog-based music recommendation system. This unique platform not only offers interactive user engagement but also suggests music tailored for input videos, so that users can refine and personalize their music selections. In contrast, previous systems predominantly emphasized content compatibility, often overlooking the nuances of users' individual preferences. For example, all the datasets only provide basic music-video pairings or such pairings with textual music descriptions. To address this gap, our research offers three contributions. First, we devise a conversation-synthesis method that simulates a two-turn interaction between a user and a recommendation system, which leverages pre-trained music tags and artist information. In this interaction, users submit a video to the system, which then suggests a suitable music piece with a rationale. Afterwards, users communicate their musical preferences, and the system presents a refined music recommendation with reasoning. Second, we introduce a multi-modal recommendation engine that matches music either by aligning it with visual cues from the video or by harmonizing visual information, feedback from previously recommended music, and the user's textual input. Third, we bridge music representations and textual data with a Large Language Model(Vicuna-7B). This alignment equips MuseChat to deliver music recommendations and their underlying reasoning in a manner resembling human communication. Our evaluations show that MuseChat surpasses existing state-of-the-art models in music retrieval tasks and pioneers the integration of the recommendation process within a natural language framework.

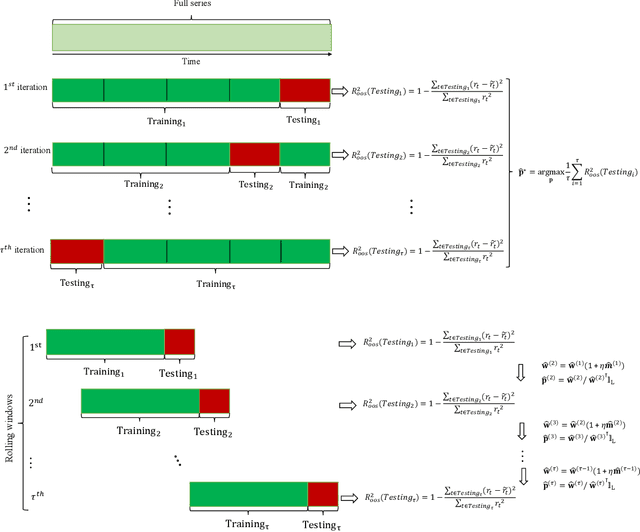

Online Ensemble of Models for Optimal Predictive Performance with Applications to Sector Rotation Strategy

Mar 30, 2023

Asset-specific factors are commonly used to forecast financial returns and quantify asset-specific risk premia. Using various machine learning models, we demonstrate that the information contained in these factors leads to even larger economic gains in terms of forecasts of sector returns and the measurement of sector-specific risk premia. To capitalize on the strong predictive results of individual models for the performance of different sectors, we develop a novel online ensemble algorithm that learns to optimize predictive performance. The algorithm continuously adapts over time to determine the optimal combination of individual models by solely analyzing their most recent prediction performance. This makes it particularly suited for time series problems, rolling window backtesting procedures, and systems of potentially black-box models. We derive the optimal gain function, express the corresponding regret bounds in terms of the out-of-sample R-squared measure, and derive optimal learning rate for the algorithm. Empirically, the new ensemble outperforms both individual machine learning models and their simple averages in providing better measurements of sector risk premia. Moreover, it allows for performance attribution of different factors across various sectors, without conditioning on a specific model. Finally, by utilizing monthly predictions from our ensemble, we develop a sector rotation strategy that significantly outperforms the market. The strategy remains robust against various financial factors, periods of financial distress, and conservative transaction costs. Notably, the strategy's efficacy persists over time, exhibiting consistent improvement throughout an extended backtesting period and yielding substantial profits during the economic turbulence of the COVID-19 pandemic.

Detection of (Hidden) Emotions from Videos using Muscles Movements and Face Manifold Embedding

Nov 01, 2022

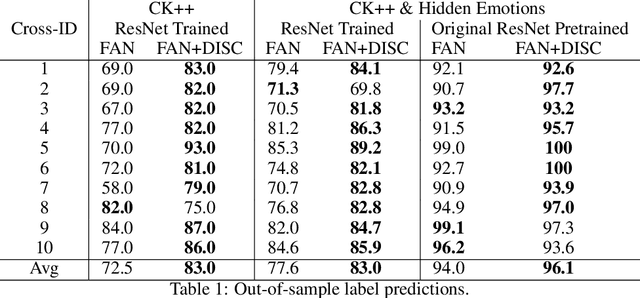

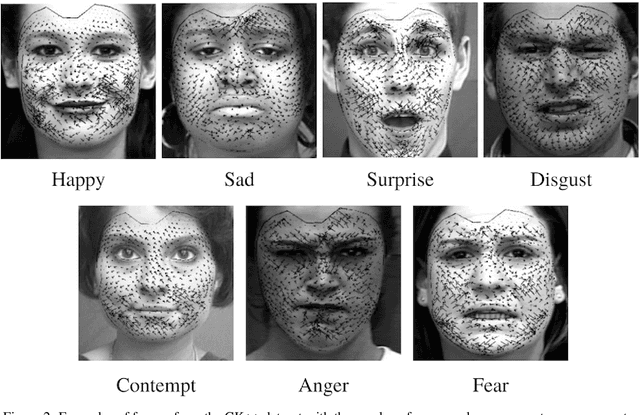

We provide a new non-invasive, easy-to-scale for large amounts of subjects and a remotely accessible method for (hidden) emotion detection from videos of human faces. Our approach combines face manifold detection for accurate location of the face in the video with local face manifold embedding to create a common domain for the measurements of muscle micro-movements that is invariant to the movement of the subject in the video. In the next step, we employ the Digital Image Speckle Correlation (DISC) and the optical flow algorithm to compute the pattern of micro-movements in the face. The corresponding vector field is mapped back to the original space and superimposed on the original frames of the videos. Hence, the resulting videos include additional information about the direction of the movement of the muscles in the face. We take the publicly available CK++ dataset of visible emotions and add to it videos of the same format but with hidden emotions. We process all the videos using our micro-movement detection and use the results to train a state-of-the-art network for emotions classification from videos -- Frame Attention Network (FAN). Although the original FAN model achieves very high out-of-sample performance on the original CK++ videos, it does not perform so well on hidden emotions videos. The performance improves significantly when the model is trained and tested on videos with the vector fields of muscle movements. Intuitively, the corresponding arrows serve as edges in the image that are easily captured by the convolutions filters in the FAN network.

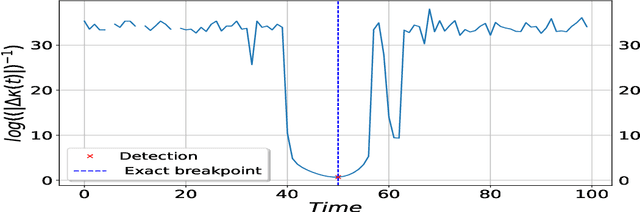

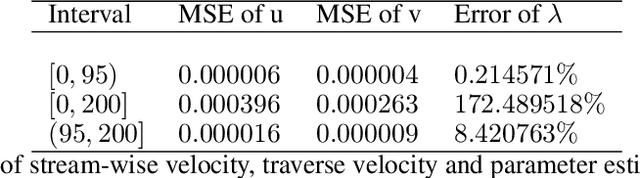

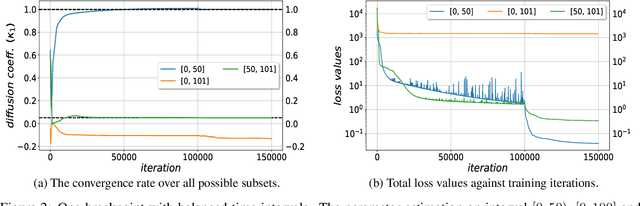

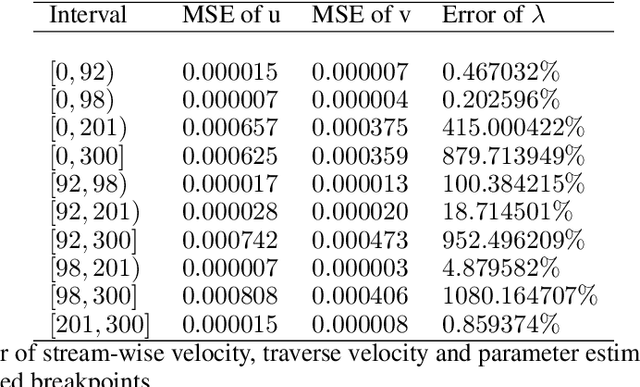

CP-PINNs: Changepoints Detection in PDEs using Physics Informed Neural Networks with Total-Variation Penalty

Aug 18, 2022

We consider the inverse problem for the Partial Differential Equations (PDEs) such that the parameters of the dependency structure can exhibit random changepoints over time. This can arise, for example, when the physical system is either under malicious attack (e.g., hacker attacks on power grids and internet networks) or subject to extreme external conditions (e.g., weather conditions impacting electricity grids or large market movements impacting valuations of derivative contracts). For that purpose, we employ Physics Informed Neural Networks (PINNs) -- universal approximators that can incorporate prior information from any physical law described by a system of PDEs. This prior knowledge acts in the training of the neural network as a regularization that limits the space of admissible solutions and increases the correctness of the function approximation. We show that when the true data generating process exhibits changepoints in the PDE dynamics, this regularization can lead to a complete miss-calibration and a failure of the model. Therefore, we propose an extension of PINNs using a Total-Variation penalty which accommodates (multiple) changepoints in the PDE dynamics. These changepoints can occur at random locations over time, and they are estimated together with the solutions. We propose an additional refinement algorithm that combines changepoints detection with a reduced dynamic programming method that is feasible for the computationally intensive PINNs methods, and we demonstrate the benefits of the proposed model empirically using examples of different equations with changes in the parameters. In case of no changepoints in the data, the proposed model reduces to the original PINNs model. In the presence of changepoints, it leads to improvements in parameter estimation, better model fitting, and a lower training error compared to the original PINNs model.