Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeComputation-Utility-Privacy Tradeoffs in Bayesian Estimation

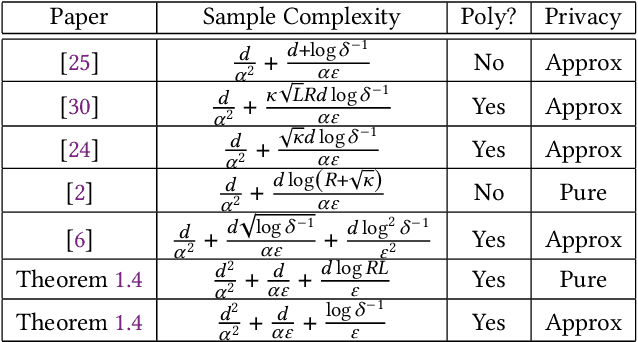

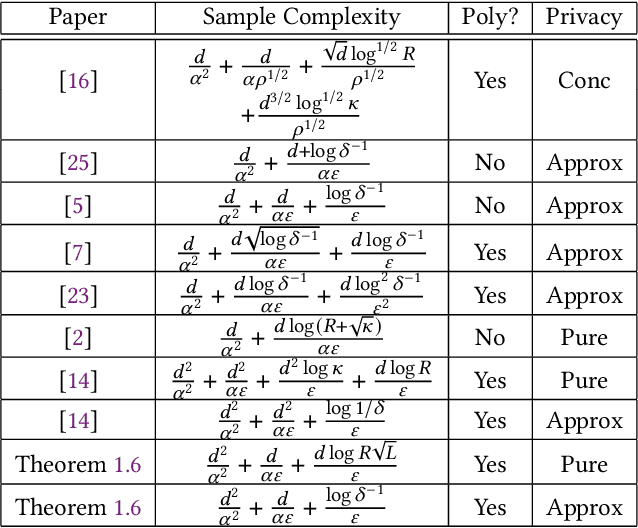

Mar 18, 2026Bayesian methods lie at the heart of modern data science and provide a powerful scaffolding for estimation in data-constrained settings and principled quantification and propagation of uncertainty. Yet in many real-world use cases where these methods are deployed, there is a natural need to preserve the privacy of the individuals whose data is being scrutinized. While a number of works have attempted to approach the problem of differentially private Bayesian estimation through either reasoning about the inherent privacy of the posterior distribution or privatizing off-the-shelf Bayesian methods, these works generally do not come with rigorous utility guarantees beyond low-dimensional settings. In fact, even for the prototypical tasks of Gaussian mean estimation and linear regression, it was unknown how close one could get to the Bayes-optimal error with a private algorithm, even in the simplest case where the unknown parameter comes from a Gaussian prior. In this work, we give the first efficient algorithms for both of these problems that achieve mean-squared error $(1+o(1))\mathrm{OPT}$ and additionally show that both tasks exhibit an intriguing computational-statistical gap. For Bayesian mean estimation, we prove that the excess risk achieved by our method is optimal among all efficient algorithms within the low-degree framework, yet is provably worse than what is achievable by an exponential-time algorithm. For linear regression, we prove a qualitatively similar lower bound. Our algorithms draw upon the privacy-to-robustness framework of arXiv:2212.05015, but with the curious twist that to achieve private Bayes-optimal estimation, we need to design sum-of-squares-based robust estimators for inherently non-robust objects like the empirical mean and OLS estimator. Along the way we also add to the sum-of-squares toolkit a new kind of constraint based on short-flat decompositions.

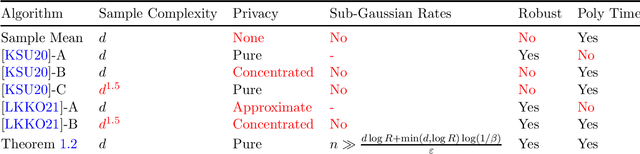

Sample-Optimal Private Regression in Polynomial Time

Mar 31, 2025

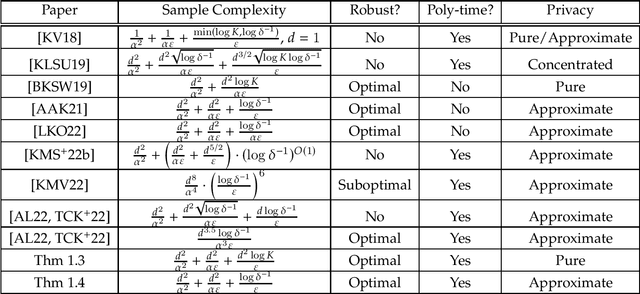

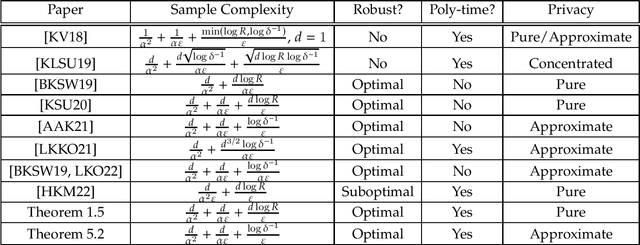

We consider the task of privately obtaining prediction error guarantees in ordinary least-squares regression problems with Gaussian covariates (with unknown covariance structure). We provide the first sample-optimal polynomial time algorithm for this task under both pure and approximate differential privacy. We show that any improvement to the sample complexity of our algorithm would violate either statistical-query or information-theoretic lower bounds. Additionally, our algorithm is robust to a small fraction of arbitrary outliers and achieves optimal error rates as a function of the fraction of outliers. In contrast, all prior efficient algorithms either incurred sample complexities with sub-optimal dimension dependence, scaling with the condition number of the covariates, or obtained a polynomially worse dependence on the privacy parameters. Our technical contributions are two-fold: first, we leverage resilience guarantees of Gaussians within the sum-of-squares framework. As a consequence, we obtain efficient sum-of-squares algorithms for regression with optimal robustness rates and sample complexity. Second, we generalize the recent robustness-to-privacy framework [HKMN23, (arXiv:2212.05015)] to account for the geometry induced by the covariance of the input samples. This framework crucially relies on the robust estimators to be sum-of-squares algorithms, and combining the two steps yields a sample-optimal private regression algorithm. We believe our techniques are of independent interest, and we demonstrate this by obtaining an efficient algorithm for covariance-aware mean estimation, with an optimal dependence on the privacy parameters.

Sample-Efficient Private Learning of Mixtures of Gaussians

Nov 04, 2024We study the problem of learning mixtures of Gaussians with approximate differential privacy. We prove that roughly $kd^2 + k^{1.5} d^{1.75} + k^2 d$ samples suffice to learn a mixture of $k$ arbitrary $d$-dimensional Gaussians up to low total variation distance, with differential privacy. Our work improves over the previous best result [AAL24b] (which required roughly $k^2 d^4$ samples) and is provably optimal when $d$ is much larger than $k^2$. Moreover, we give the first optimal bound for privately learning mixtures of $k$ univariate (i.e., $1$-dimensional) Gaussians. Importantly, we show that the sample complexity for privately learning mixtures of univariate Gaussians is linear in the number of components $k$, whereas the previous best sample complexity [AAL21] was quadratic in $k$. Our algorithms utilize various techniques, including the inverse sensitivity mechanism [AD20b, AD20a, HKMN23], sample compression for distributions [ABDH+20], and methods for bounding volumes of sumsets.

Private Mean Estimation with Person-Level Differential Privacy

May 30, 2024We study differentially private (DP) mean estimation in the case where each person holds multiple samples. Commonly referred to as the "user-level" setting, DP here requires the usual notion of distributional stability when all of a person's datapoints can be modified. Informally, if $n$ people each have $m$ samples from an unknown $d$-dimensional distribution with bounded $k$-th moments, we show that \[n = \tilde \Theta\left(\frac{d}{\alpha^2 m} + \frac{d }{ \alpha m^{1/2} \varepsilon} + \frac{d}{\alpha^{k/(k-1)} m \varepsilon} + \frac{d}{\varepsilon}\right)\] people are necessary and sufficient to estimate the mean up to distance $\alpha$ in $\ell_2$-norm under $\varepsilon$-differential privacy (and its common relaxations). In the multivariate setting, we give computationally efficient algorithms under approximate DP (with slightly degraded sample complexity) and computationally inefficient algorithms under pure DP, and our nearly matching lower bounds hold for the most permissive case of approximate DP. Our computationally efficient estimators are based on the well known noisy-clipped-mean approach, but the analysis for our setting requires new bounds on the tails of sums of independent, vector-valued, bounded-moments random variables, and a new argument for bounding the bias introduced by clipping.

Robustness Implies Privacy in Statistical Estimation

Dec 09, 2022

We study the relationship between adversarial robustness and differential privacy in high-dimensional algorithmic statistics. We give the first black-box reduction from privacy to robustness which can produce private estimators with optimal tradeoffs among sample complexity, accuracy, and privacy for a wide range of fundamental high-dimensional parameter estimation problems, including mean and covariance estimation. We show that this reduction can be implemented in polynomial time in some important special cases. In particular, using nearly-optimal polynomial-time robust estimators for the mean and covariance of high-dimensional Gaussians which are based on the Sum-of-Squares method, we design the first polynomial-time private estimators for these problems with nearly-optimal samples-accuracy-privacy tradeoffs. Our algorithms are also robust to a constant fraction of adversarially-corrupted samples.

Efficient Mean Estimation with Pure Differential Privacy via a Sum-of-Squares Exponential Mechanism

Nov 25, 2021

We give the first polynomial-time algorithm to estimate the mean of a $d$-variate probability distribution with bounded covariance from $\tilde{O}(d)$ independent samples subject to pure differential privacy. Prior algorithms for this problem either incur exponential running time, require $\Omega(d^{1.5})$ samples, or satisfy only the weaker concentrated or approximate differential privacy conditions. In particular, all prior polynomial-time algorithms require $d^{1+\Omega(1)}$ samples to guarantee small privacy loss with "cryptographically" high probability, $1-2^{-d^{\Omega(1)}}$, while our algorithm retains $\tilde{O}(d)$ sample complexity even in this stringent setting. Our main technique is a new approach to use the powerful Sum of Squares method (SoS) to design differentially private algorithms. SoS proofs to algorithms is a key theme in numerous recent works in high-dimensional algorithmic statistics -- estimators which apparently require exponential running time but whose analysis can be captured by low-degree Sum of Squares proofs can be automatically turned into polynomial-time algorithms with the same provable guarantees. We demonstrate a similar proofs to private algorithms phenomenon: instances of the workhorse exponential mechanism which apparently require exponential time but which can be analyzed with low-degree SoS proofs can be automatically turned into polynomial-time differentially private algorithms. We prove a meta-theorem capturing this phenomenon, which we expect to be of broad use in private algorithm design. Our techniques also draw new connections between differentially private and robust statistics in high dimensions. In particular, viewed through our proofs-to-private-algorithms lens, several well-studied SoS proofs from recent works in algorithmic robust statistics directly yield key components of our differentially private mean estimation algorithm.