Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLess Is More: Generating Time Series with LLaMA-Style Autoregression in Simple Factorized Latent Spaces

Nov 07, 2025Generative models for multivariate time series are essential for data augmentation, simulation, and privacy preservation, yet current state-of-the-art diffusion-based approaches are slow and limited to fixed-length windows. We propose FAR-TS, a simple yet effective framework that combines disentangled factorization with an autoregressive Transformer over a discrete, quantized latent space to generate time series. Each time series is decomposed into a data-adaptive basis that captures static cross-channel correlations and temporal coefficients that are vector-quantized into discrete tokens. A LLaMA-style autoregressive Transformer then models these token sequences, enabling fast and controllable generation of sequences with arbitrary length. Owing to its streamlined design, FAR-TS achieves orders-of-magnitude faster generation than Diffusion-TS while preserving cross-channel correlations and an interpretable latent space, enabling high-quality and flexible time series synthesis.

BPQP: A Differentiable Convex Optimization Framework for Efficient End-to-End Learning

Nov 28, 2024Data-driven decision-making processes increasingly utilize end-to-end learnable deep neural networks to render final decisions. Sometimes, the output of the forward functions in certain layers is determined by the solutions to mathematical optimization problems, leading to the emergence of differentiable optimization layers that permit gradient back-propagation. However, real-world scenarios often involve large-scale datasets and numerous constraints, presenting significant challenges. Current methods for differentiating optimization problems typically rely on implicit differentiation, which necessitates costly computations on the Jacobian matrices, resulting in low efficiency. In this paper, we introduce BPQP, a differentiable convex optimization framework designed for efficient end-to-end learning. To enhance efficiency, we reformulate the backward pass as a simplified and decoupled quadratic programming problem by leveraging the structural properties of the KKT matrix. This reformulation enables the use of first-order optimization algorithms in calculating the backward pass gradients, allowing our framework to potentially utilize any state-of-the-art solver. As solver technologies evolve, BPQP can continuously adapt and improve its efficiency. Extensive experiments on both simulated and real-world datasets demonstrate that BPQP achieves a significant improvement in efficiency--typically an order of magnitude faster in overall execution time compared to other differentiable optimization layers. Our results not only highlight the efficiency gains of BPQP but also underscore its superiority over differentiable optimization layer baselines.

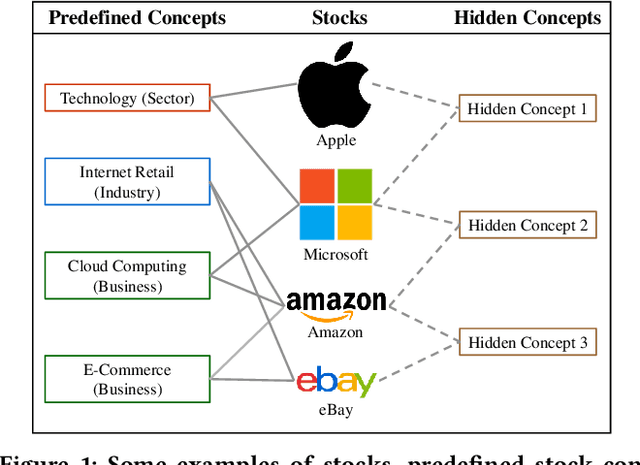

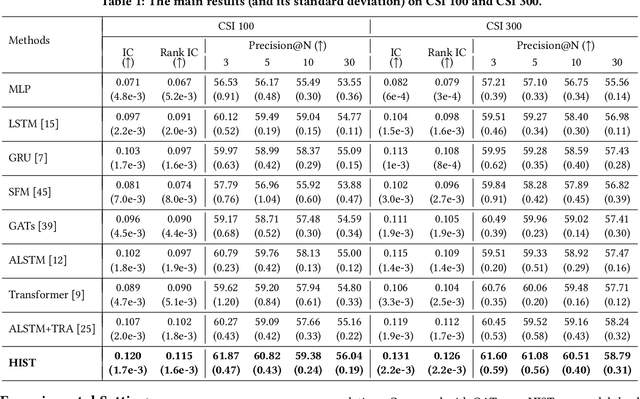

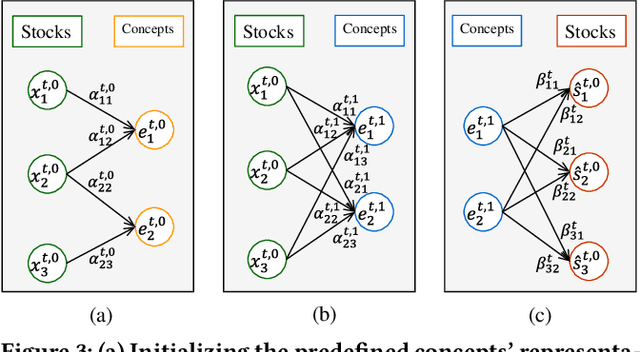

HIST: A Graph-based Framework for Stock Trend Forecasting via Mining Concept-Oriented Shared Information

Oct 26, 2021

Stock trend forecasting, which forecasts stock prices' future trends, plays an essential role in investment. The stocks in a market can share information so that their stock prices are highly correlated. Several methods were recently proposed to mine the shared information through stock concepts (e.g., technology, Internet Retail) extracted from the Web to improve the forecasting results. However, previous work assumes the connections between stocks and concepts are stationary, and neglects the dynamic relevance between stocks and concepts, limiting the forecasting results. Moreover, existing methods overlook the invaluable shared information carried by hidden concepts, which measure stocks' commonness beyond the manually defined stock concepts. To overcome the shortcomings of previous work, we proposed a novel stock trend forecasting framework that can adequately mine the concept-oriented shared information from predefined concepts and hidden concepts. The proposed framework simultaneously utilize the stock's shared information and individual information to improve the stock trend forecasting performance. Experimental results on the real-world tasks demonstrate the efficiency of our framework on stock trend forecasting. The investment simulation shows that our framework can achieve a higher investment return than the baselines.