Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFrom Deep Learning to LLMs: A survey of AI in Quantitative Investment

Mar 27, 2025

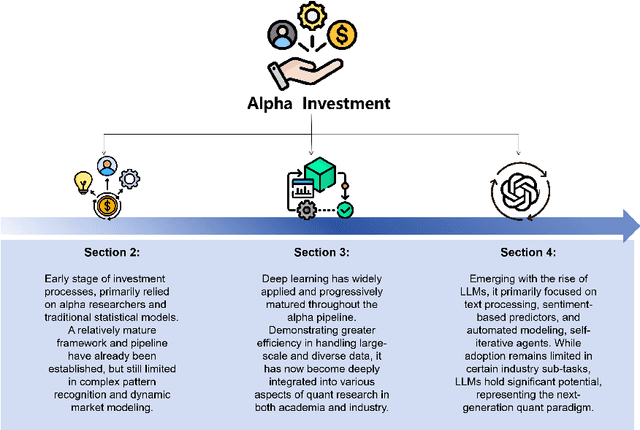

Quantitative investment (quant) is an emerging, technology-driven approach in asset management, increasingy shaped by advancements in artificial intelligence. Recent advances in deep learning and large language models (LLMs) for quant finance have improved predictive modeling and enabled agent-based automation, suggesting a potential paradigm shift in this field. In this survey, taking alpha strategy as a representative example, we explore how AI contributes to the quantitative investment pipeline. We first examine the early stage of quant research, centered on human-crafted features and traditional statistical models with an established alpha pipeline. We then discuss the rise of deep learning, which enabled scalable modeling across the entire pipeline from data processing to order execution. Building on this, we highlight the emerging role of LLMs in extending AI beyond prediction, empowering autonomous agents to process unstructured data, generate alphas, and support self-iterative workflows.

Unveiling the Potential of Sentiment: Can Large Language Models Predict Chinese Stock Price Movements?

Jun 25, 2023The rapid advancement of Large Language Models (LLMs) has led to extensive discourse regarding their potential to boost the return of quantitative stock trading strategies. This discourse primarily revolves around harnessing the remarkable comprehension capabilities of LLMs to extract sentiment factors which facilitate informed and high-frequency investment portfolio adjustments. To ensure successful implementations of these LLMs into the analysis of Chinese financial texts and the subsequent trading strategy development within the Chinese stock market, we provide a rigorous and encompassing benchmark as well as a standardized back-testing framework aiming at objectively assessing the efficacy of various types of LLMs in the specialized domain of sentiment factor extraction from Chinese news text data. To illustrate how our benchmark works, we reference three distinctive models: 1) the generative LLM (ChatGPT), 2) the Chinese language-specific pre-trained LLM (Erlangshen-RoBERTa), and 3) the financial domain-specific fine-tuned LLM classifier(Chinese FinBERT). We apply them directly to the task of sentiment factor extraction from large volumes of Chinese news summary texts. We then proceed to building quantitative trading strategies and running back-tests under realistic trading scenarios based on the derived sentiment factors and evaluate their performances with our benchmark. By constructing such a comparative analysis, we invoke the question of what constitutes the most important element for improving a LLM's performance on extracting sentiment factors. And by ensuring that the LLMs are evaluated on the same benchmark, following the same standardized experimental procedures that are designed with sufficient expertise in quantitative trading, we make the first stride toward answering such a question.

A Comparative Evaluation of Predominant Deep Learning Quantified Stock Trading Strategies

Apr 06, 2021

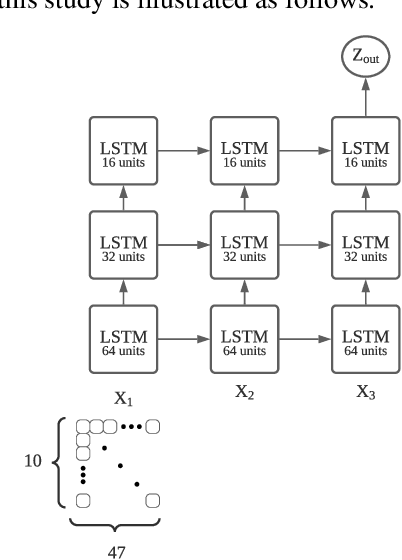

This study first reconstructs three deep learning powered stock trading models and their associated strategies that are representative of distinct approaches to the problem and established upon different aspects of the many theories evolved around deep learning. It then seeks to compare the performance of these strategies from different perspectives through trading simulations ran on three scenarios when the benchmarks are kept at historical low points for extended periods of time. The results show that in extremely adverse market climates, investment portfolios managed by deep learning powered algorithms are able to avert accumulated losses by generating return sequences that shift the constantly negative CSI 300 benchmark return upward. Among the three, the LSTM model's strategy yields the best performance when the benchmark sustains continued loss.