Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFrom Deep Learning to LLMs: A survey of AI in Quantitative Investment

Paper and Code

Mar 27, 2025

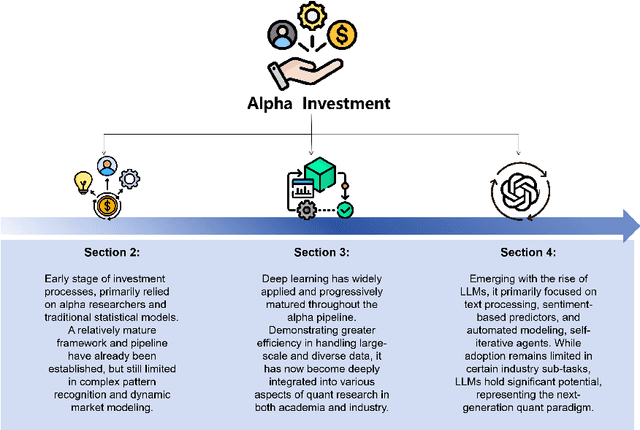

Quantitative investment (quant) is an emerging, technology-driven approach in asset management, increasingy shaped by advancements in artificial intelligence. Recent advances in deep learning and large language models (LLMs) for quant finance have improved predictive modeling and enabled agent-based automation, suggesting a potential paradigm shift in this field. In this survey, taking alpha strategy as a representative example, we explore how AI contributes to the quantitative investment pipeline. We first examine the early stage of quant research, centered on human-crafted features and traditional statistical models with an established alpha pipeline. We then discuss the rise of deep learning, which enabled scalable modeling across the entire pipeline from data processing to order execution. Building on this, we highlight the emerging role of LLMs in extending AI beyond prediction, empowering autonomous agents to process unstructured data, generate alphas, and support self-iterative workflows.