Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeThe Causal Impact of Credit Lines on Spending Distributions

Dec 16, 2023Consumer credit services offered by e-commerce platforms provide customers with convenient loan access during shopping and have the potential to stimulate sales. To understand the causal impact of credit lines on spending, previous studies have employed causal estimators, based on direct regression (DR), inverse propensity weighting (IPW), and double machine learning (DML) to estimate the treatment effect. However, these estimators do not consider the notion that an individual's spending can be understood and represented as a distribution, which captures the range and pattern of amounts spent across different orders. By disregarding the outcome as a distribution, valuable insights embedded within the outcome distribution might be overlooked. This paper develops a distribution-valued estimator framework that extends existing real-valued DR-, IPW-, and DML-based estimators to distribution-valued estimators within Rubin's causal framework. We establish their consistency and apply them to a real dataset from a large e-commerce platform. Our findings reveal that credit lines positively influence spending across all quantiles; however, as credit lines increase, consumers allocate more to luxuries (higher quantiles) than necessities (lower quantiles).

DeLELSTM: Decomposition-based Linear Explainable LSTM to Capture Instantaneous and Long-term Effects in Time Series

Aug 26, 2023

Time series forecasting is prevalent in various real-world applications. Despite the promising results of deep learning models in time series forecasting, especially the Recurrent Neural Networks (RNNs), the explanations of time series models, which are critical in high-stakes applications, have received little attention. In this paper, we propose a Decomposition-based Linear Explainable LSTM (DeLELSTM) to improve the interpretability of LSTM. Conventionally, the interpretability of RNNs only concentrates on the variable importance and time importance. We additionally distinguish between the instantaneous influence of new coming data and the long-term effects of historical data. Specifically, DeLELSTM consists of two components, i.e., standard LSTM and tensorized LSTM. The tensorized LSTM assigns each variable with a unique hidden state making up a matrix $\mathbf{h}_t$, and the standard LSTM models all the variables with a shared hidden state $\mathbf{H}_t$. By decomposing the $\mathbf{H}_t$ into the linear combination of past information $\mathbf{h}_{t-1}$ and the fresh information $\mathbf{h}_{t}-\mathbf{h}_{t-1}$, we can get the instantaneous influence and the long-term effect of each variable. In addition, the advantage of linear regression also makes the explanation transparent and clear. We demonstrate the effectiveness and interpretability of DeLELSTM on three empirical datasets. Extensive experiments show that the proposed method achieves competitive performance against the baseline methods and provides a reliable explanation relative to domain knowledge.

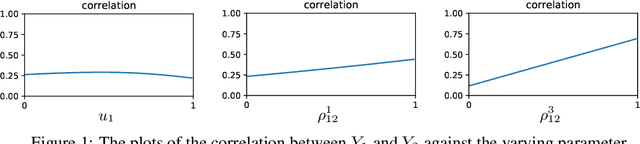

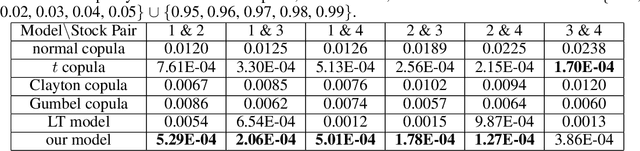

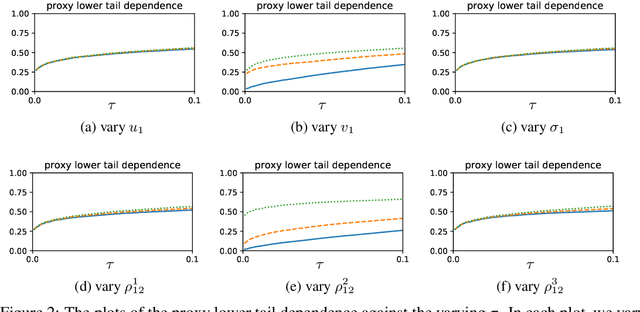

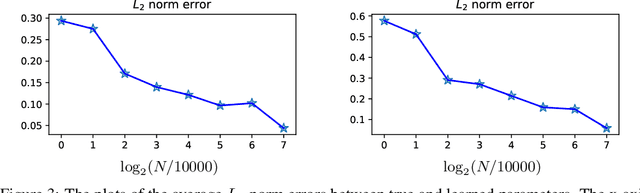

Generative Learning of Heterogeneous Tail Dependence

Nov 26, 2020

We propose a multivariate generative model to capture the complex dependence structure often encountered in business and financial data. Our model features heterogeneous and asymmetric tail dependence between all pairs of individual dimensions while also allowing heterogeneity and asymmetry in the tails of the marginals. A significant merit of our model structure is that it is not prone to error propagation in the parameter estimation process, hence very scalable, as the dimensions of datasets grow large. However, the likelihood methods are infeasible for parameter estimation in our case due to the lack of a closed-form density function. Instead, we devise a novel moment learning algorithm to learn the parameters. To demonstrate the effectiveness of the model and its estimator, we test them on simulated as well as real-world datasets. Results show that this framework gives better finite-sample performance compared to the copula-based benchmarks as well as recent similar models.