Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGenerative Learning of Heterogeneous Tail Dependence

Paper and Code

Nov 26, 2020

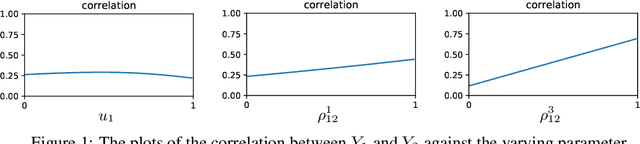

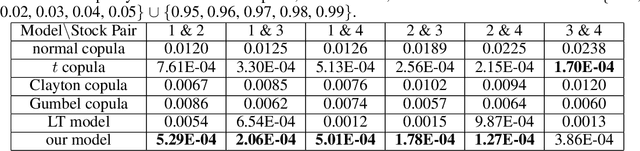

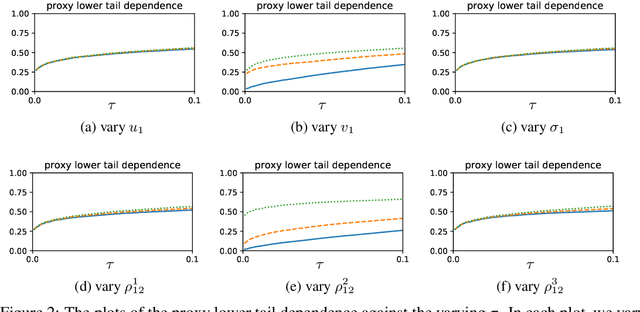

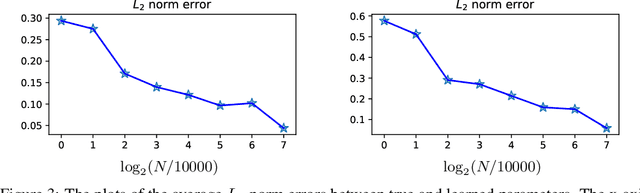

We propose a multivariate generative model to capture the complex dependence structure often encountered in business and financial data. Our model features heterogeneous and asymmetric tail dependence between all pairs of individual dimensions while also allowing heterogeneity and asymmetry in the tails of the marginals. A significant merit of our model structure is that it is not prone to error propagation in the parameter estimation process, hence very scalable, as the dimensions of datasets grow large. However, the likelihood methods are infeasible for parameter estimation in our case due to the lack of a closed-form density function. Instead, we devise a novel moment learning algorithm to learn the parameters. To demonstrate the effectiveness of the model and its estimator, we test them on simulated as well as real-world datasets. Results show that this framework gives better finite-sample performance compared to the copula-based benchmarks as well as recent similar models.