Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCOTODE: COntinuous Trajectory neural Ordinary Differential Equations for modelling event sequences

Aug 15, 2024Observation of the underlying actors that generate event sequences reveals that they often evolve continuously. Most modern methods, however, tend to model such processes through at most piecewise-continuous trajectories. To address this, we adopt a way of viewing events not as standalone phenomena but instead as observations of a Gaussian Process, which in turn governs the actor's dynamics. We propose integrating these obtained dynamics, resulting in a continuous-trajectory modification of the widely successful Neural ODE model. Through Gaussian Process theory, we were able to evaluate the uncertainty in an actor's representation, which arises from not observing them between events. This estimate led us to develop a novel, theoretically backed negative feedback mechanism. Empirical studies indicate that our model with Gaussian process interpolation and negative feedback achieves state-of-the-art performance, with improvements up to 20% AUROC against similar architectures.

Continuous-time convolutions model of event sequences

Feb 13, 2023

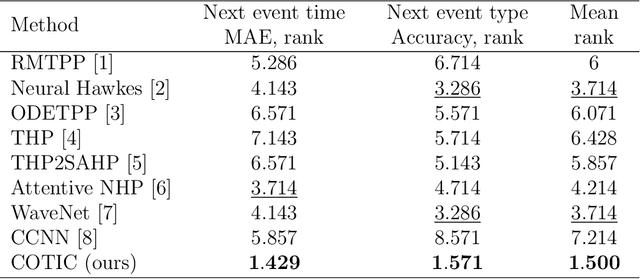

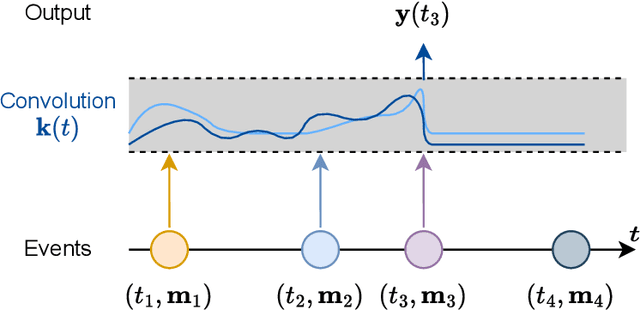

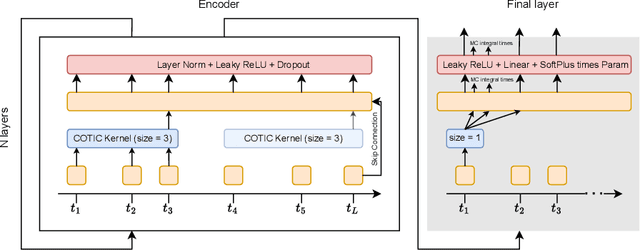

Massive samples of event sequences data occur in various domains, including e-commerce, healthcare, and finance. There are two main challenges regarding inference of such data: computational and methodological. The amount of available data and the length of event sequences per client are typically large, thus it requires long-term modelling. Moreover, this data is often sparse and non-uniform, making classic approaches for time series processing inapplicable. Existing solutions include recurrent and transformer architectures in such cases. To allow continuous time, the authors introduce specific parametric intensity functions defined at each moment on top of existing models. Due to the parametric nature, these intensities represent only a limited class of event sequences. We propose the COTIC method based on a continuous convolution neural network suitable for non-uniform occurrence of events in time. In COTIC, dilations and multi-layer architecture efficiently handle dependencies between events. Furthermore, the model provides general intensity dynamics in continuous time - including self-excitement encountered in practice. The COTIC model outperforms existing approaches on majority of the considered datasets, producing embeddings for an event sequence that can be used to solve downstream tasks - e.g. predicting next event type and return time. The code of the proposed method can be found in the GitHub repository (https://github.com/VladislavZh/COTIC).

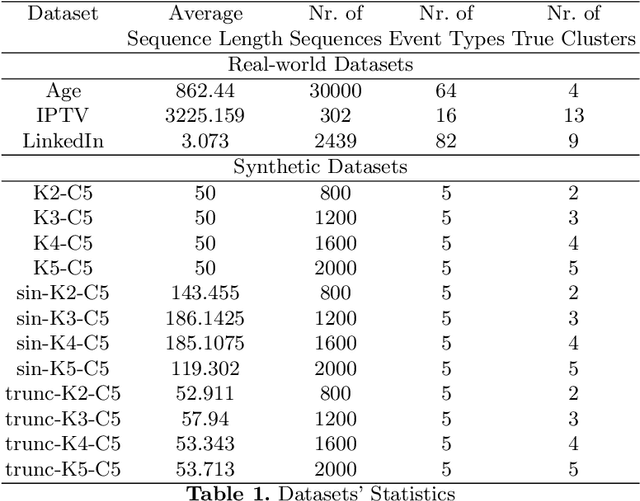

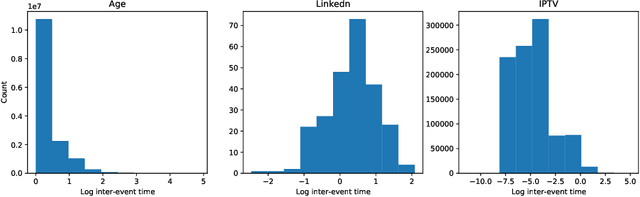

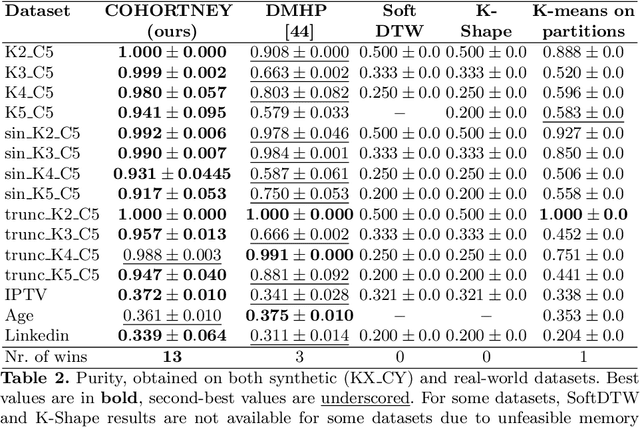

COHORTNEY: Deep Clustering for Heterogeneous Event Sequences

Apr 03, 2021

There is emerging attention towards working with event sequences. In particular, clustering of event sequences is widely applicable in domains such as healthcare, marketing, and finance. Use cases include analysis of visitors to websites, hospitals, or bank transactions. Unlike traditional time series, event sequences tend to be sparse and not equally spaced in time. As a result, they exhibit different properties, which are essential to account for when developing state-of-the-art methods. The community has paid little attention to the specifics of heterogeneous event sequences. Existing research in clustering primarily focuses on classic times series data. It is unclear if proposed methods in the literature generalize well to event sequences. Here we propose COHORTNEY as a novel deep learning method for clustering heterogeneous event sequences. Our contributions include (i) a novel method using a combination of LSTM and the EM algorithm and code implementation; (ii) a comparison of this method to previous research on time series and event sequence clustering; (iii) a performance benchmark of different approaches on a new dataset from the finance industry and fourteen additional datasets. Our results show that COHORTNEY vastly outperforms in speed and cluster quality the state-of-the-art algorithm for clustering event sequences.