Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRefining embeddings with fill-tuning: data-efficient generalised performance improvements for materials foundation models

Feb 19, 2025

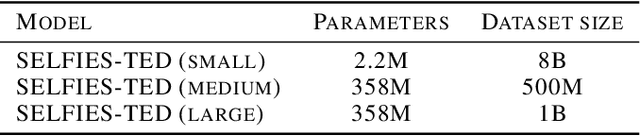

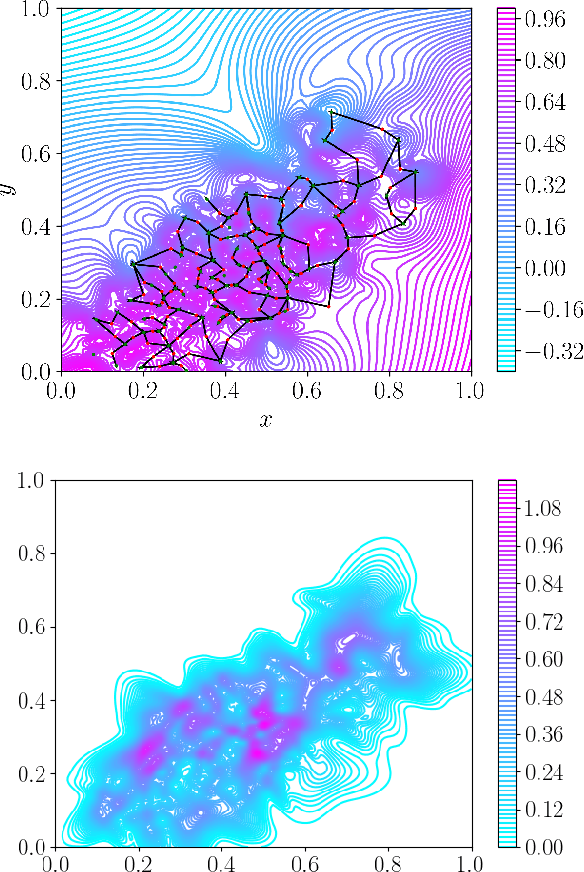

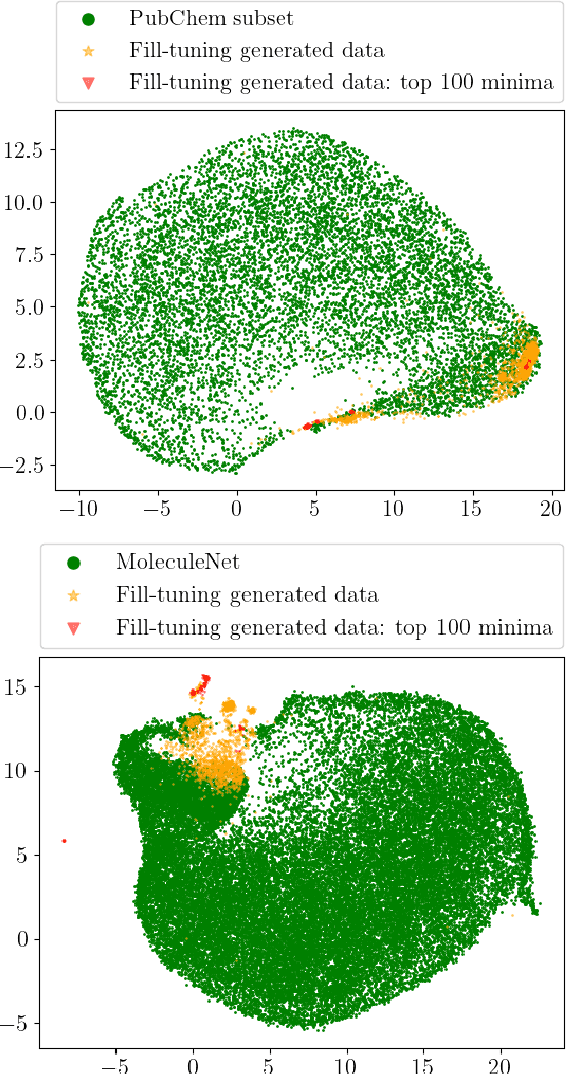

Pretrained foundation models learn embeddings that can be used for a wide range of downstream tasks. These embeddings optimise general performance, and if insufficiently accurate at a specific task the model can be fine-tuned to improve performance. For all current methodologies this operation necessarily degrades performance on all out-of-distribution tasks. In this work we present 'fill-tuning', a novel methodology to generate datasets for continued pretraining of foundation models that are not suited to a particular downstream task, but instead aim to correct poor regions of the embedding. We present the application of roughness analysis to latent space topologies and illustrate how it can be used to propose data that will be most valuable to improving the embedding. We apply fill-tuning to a set of state-of-the-art materials foundation models trained on $O(10^9)$ data points and show model improvement of almost 1% in all downstream tasks with the addition of only 100 data points. This method provides a route to the general improvement of foundation models at the computational cost of fine-tuning.

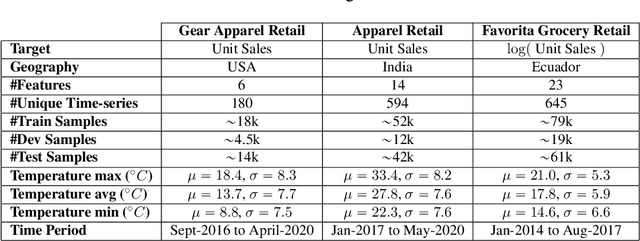

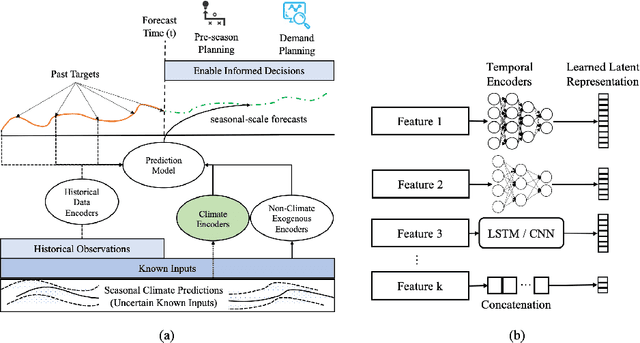

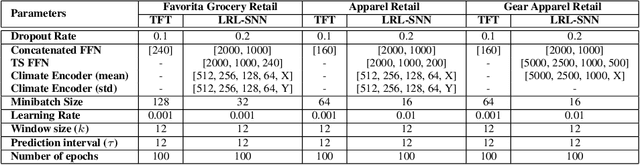

Encoding Seasonal Climate Predictions for Demand Forecasting with Modular Neural Network

Sep 05, 2023

Current time-series forecasting problems use short-term weather attributes as exogenous inputs. However, in specific time-series forecasting solutions (e.g., demand prediction in the supply chain), seasonal climate predictions are crucial to improve its resilience. Representing mid to long-term seasonal climate forecasts is challenging as seasonal climate predictions are uncertain, and encoding spatio-temporal relationship of climate forecasts with demand is complex. We propose a novel modeling framework that efficiently encodes seasonal climate predictions to provide robust and reliable time-series forecasting for supply chain functions. The encoding framework enables effective learning of latent representations -- be it uncertain seasonal climate prediction or other time-series data (e.g., buyer patterns) -- via a modular neural network architecture. Our extensive experiments indicate that learning such representations to model seasonal climate forecast results in an error reduction of approximately 13\% to 17\% across multiple real-world data sets compared to existing demand forecasting methods.

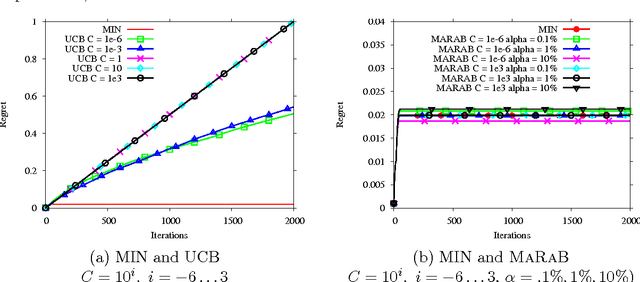

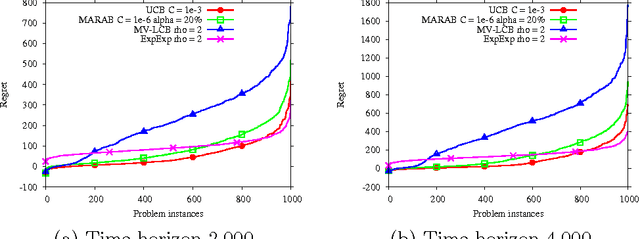

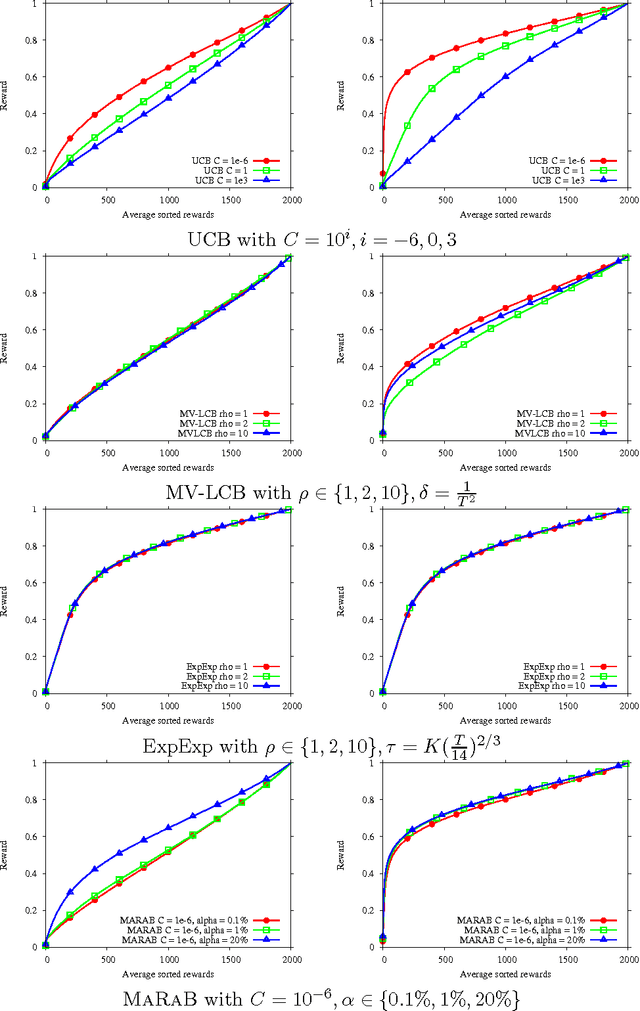

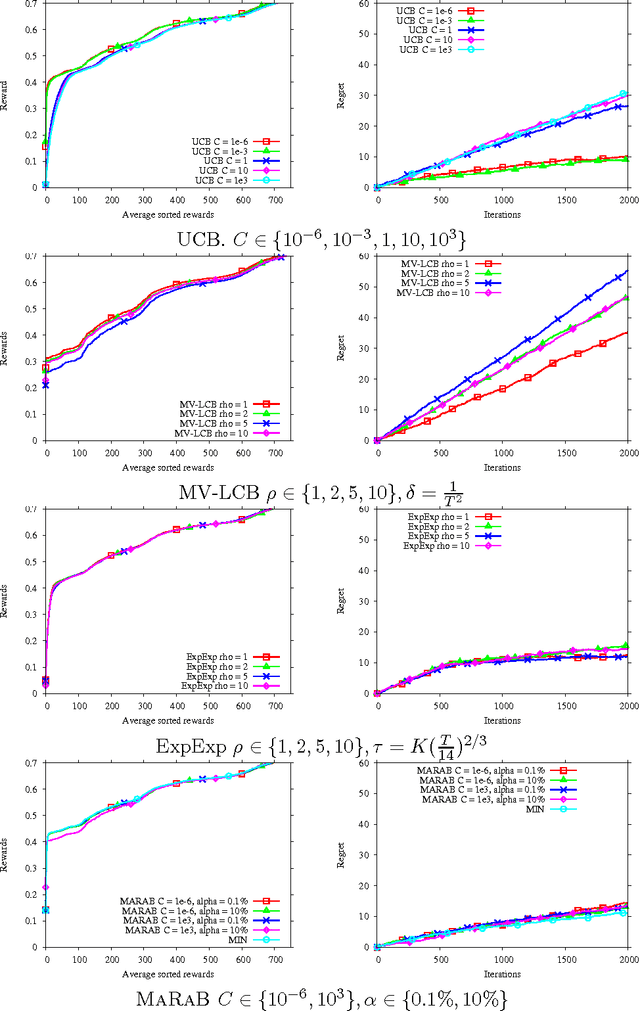

Exploration vs Exploitation vs Safety: Risk-averse Multi-Armed Bandits

Jan 06, 2014

Motivated by applications in energy management, this paper presents the Multi-Armed Risk-Aware Bandit (MARAB) algorithm. With the goal of limiting the exploration of risky arms, MARAB takes as arm quality its conditional value at risk. When the user-supplied risk level goes to 0, the arm quality tends toward the essential infimum of the arm distribution density, and MARAB tends toward the MIN multi-armed bandit algorithm, aimed at the arm with maximal minimal value. As a first contribution, this paper presents a theoretical analysis of the MIN algorithm under mild assumptions, establishing its robustness comparatively to UCB. The analysis is supported by extensive experimental validation of MIN and MARAB compared to UCB and state-of-art risk-aware MAB algorithms on artificial and real-world problems.

* 16 pages