Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

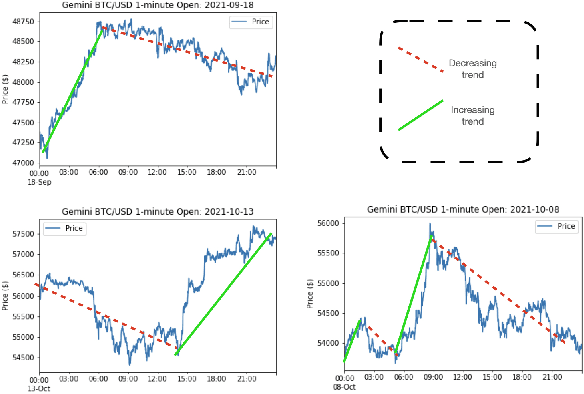

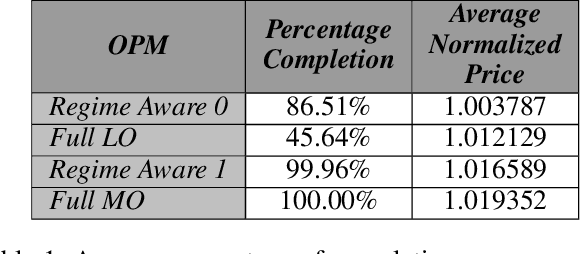

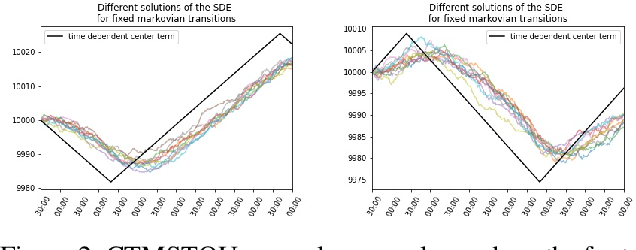

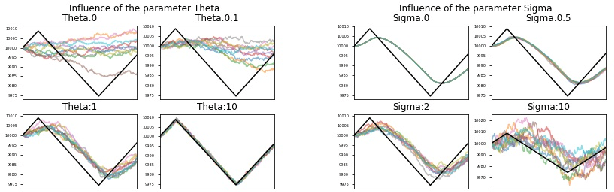

Add to EdgeCTMSTOU driven markets: simulated environment for regime-awareness in trading policies

Feb 03, 2022

Market regimes is a popular topic in quantitative finance even though there is little consensus on the details of how they should be defined. They arise as a feature both in financial market prediction problems and financial market task performing problems. In this work we use discrete event time multi-agent market simulation to freely experiment in a reproducible and understandable environment where regimes can be explicitly switched and enforced. We introduce a novel stochastic process to model the fundamental value perceived by market participants: Continuous-Time Markov Switching Trending Ornstein-Uhlenbeck (CTMSTOU), which facilitates the study of trading policies in regime switching markets. We define the notion of regime-awareness for a trading agent as well and illustrate its importance through the study of different order placement strategies in the context of order execution problems.

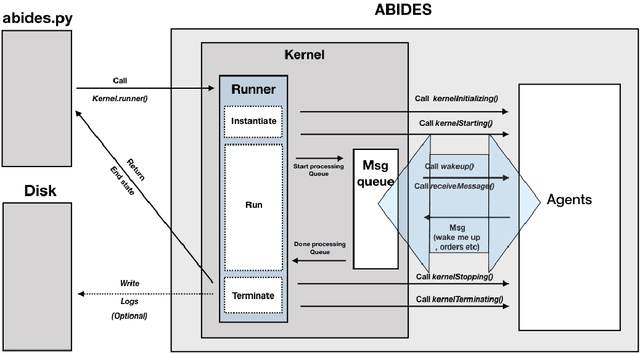

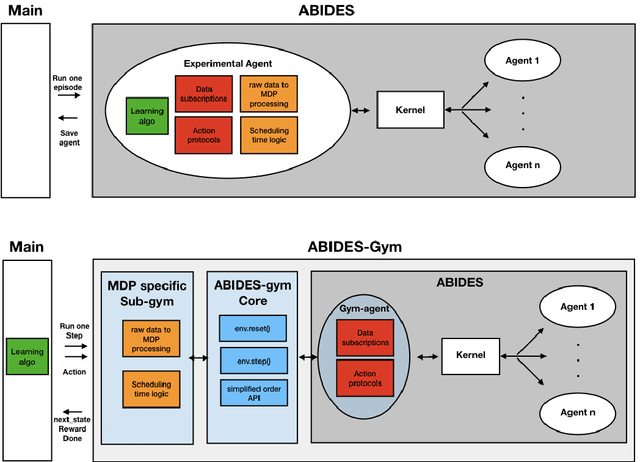

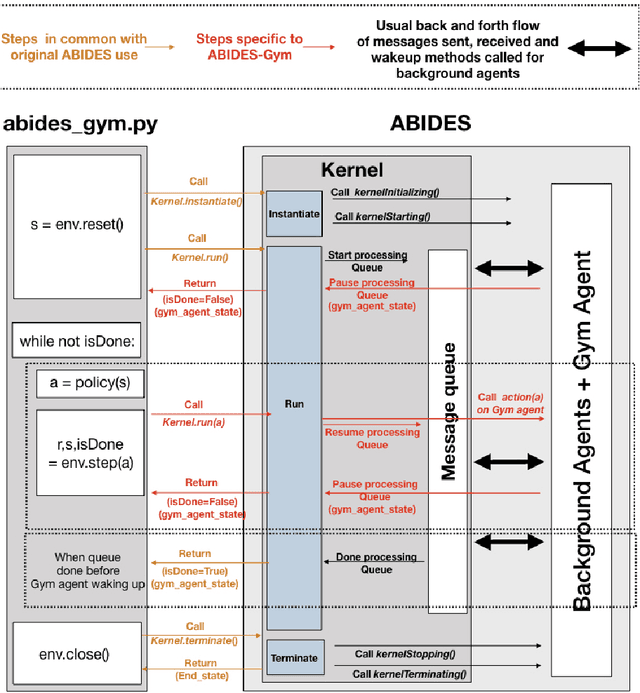

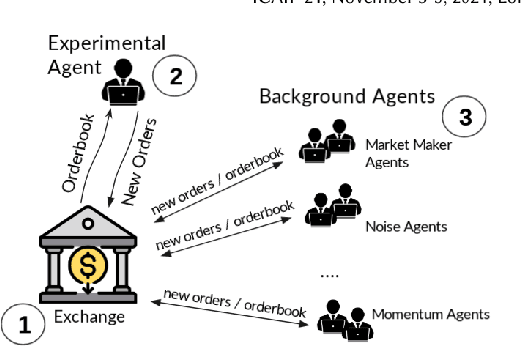

ABIDES-Gym: Gym Environments for Multi-Agent Discrete Event Simulation and Application to Financial Markets

Oct 27, 2021

Model-free Reinforcement Learning (RL) requires the ability to sample trajectories by taking actions in the original problem environment or a simulated version of it. Breakthroughs in the field of RL have been largely facilitated by the development of dedicated open source simulators with easy to use frameworks such as OpenAI Gym and its Atari environments. In this paper we propose to use the OpenAI Gym framework on discrete event time based Discrete Event Multi-Agent Simulation (DEMAS). We introduce a general technique to wrap a DEMAS simulator into the Gym framework. We expose the technique in detail and implement it using the simulator ABIDES as a base. We apply this work by specifically using the markets extension of ABIDES, ABIDES-Markets, and develop two benchmark financial markets OpenAI Gym environments for training daily investor and execution agents. As a result, these two environments describe classic financial problems with a complex interactive market behavior response to the experimental agent's action.

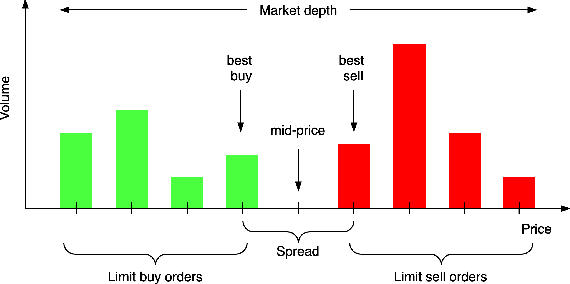

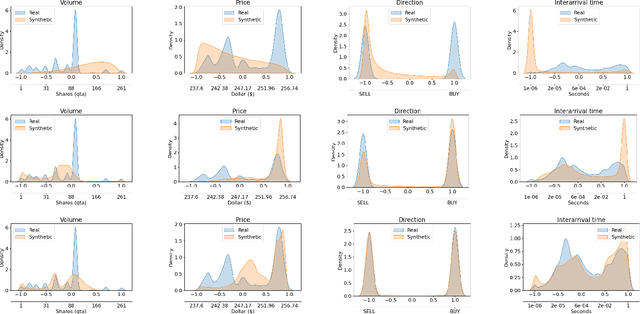

Towards Realistic Market Simulations: a Generative Adversarial Networks Approach

Oct 25, 2021

Simulated environments are increasingly used by trading firms and investment banks to evaluate trading strategies before approaching real markets. Backtesting, a widely used approach, consists of simulating experimental strategies while replaying historical market scenarios. Unfortunately, this approach does not capture the market response to the experimental agents' actions. In contrast, multi-agent simulation presents a natural bottom-up approach to emulating agent interaction in financial markets. It allows to set up pools of traders with diverse strategies to mimic the financial market trader population, and test the performance of new experimental strategies. Since individual agent-level historical data is typically proprietary and not available for public use, it is difficult to calibrate multiple market agents to obtain the realism required for testing trading strategies. To addresses this challenge we propose a synthetic market generator based on Conditional Generative Adversarial Networks (CGANs) trained on real aggregate-level historical data. A CGAN-based "world" agent can generate meaningful orders in response to an experimental agent. We integrate our synthetic market generator into ABIDES, an open source simulator of financial markets. By means of extensive simulations we show that our proposal outperforms previous work in terms of stylized facts reflecting market responsiveness and realism.