Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTowards Realistic Market Simulations: a Generative Adversarial Networks Approach

Paper and Code

Oct 25, 2021

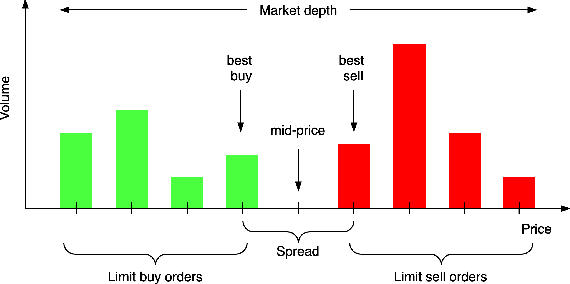

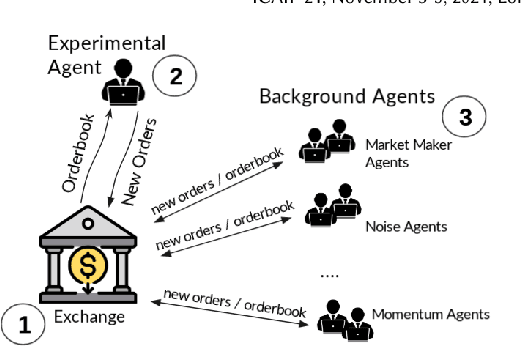

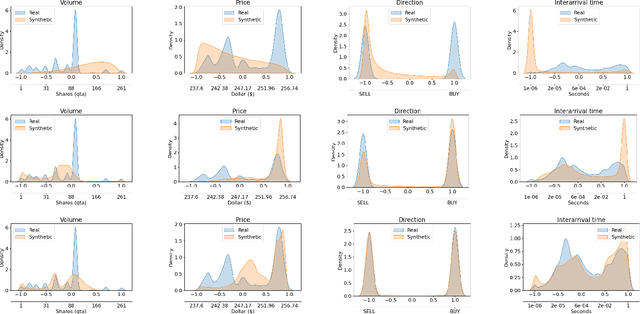

Simulated environments are increasingly used by trading firms and investment banks to evaluate trading strategies before approaching real markets. Backtesting, a widely used approach, consists of simulating experimental strategies while replaying historical market scenarios. Unfortunately, this approach does not capture the market response to the experimental agents' actions. In contrast, multi-agent simulation presents a natural bottom-up approach to emulating agent interaction in financial markets. It allows to set up pools of traders with diverse strategies to mimic the financial market trader population, and test the performance of new experimental strategies. Since individual agent-level historical data is typically proprietary and not available for public use, it is difficult to calibrate multiple market agents to obtain the realism required for testing trading strategies. To addresses this challenge we propose a synthetic market generator based on Conditional Generative Adversarial Networks (CGANs) trained on real aggregate-level historical data. A CGAN-based "world" agent can generate meaningful orders in response to an experimental agent. We integrate our synthetic market generator into ABIDES, an open source simulator of financial markets. By means of extensive simulations we show that our proposal outperforms previous work in terms of stylized facts reflecting market responsiveness and realism.