Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCTMSTOU driven markets: simulated environment for regime-awareness in trading policies

Paper and Code

Feb 03, 2022

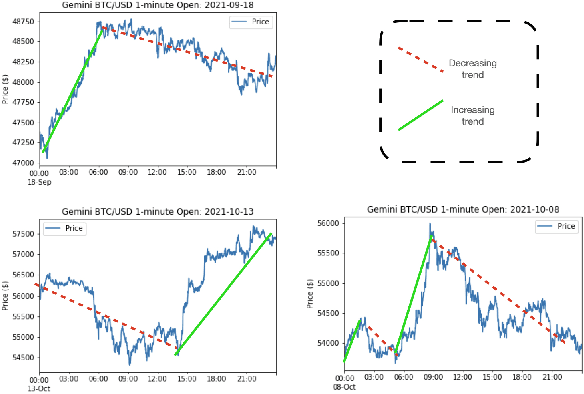

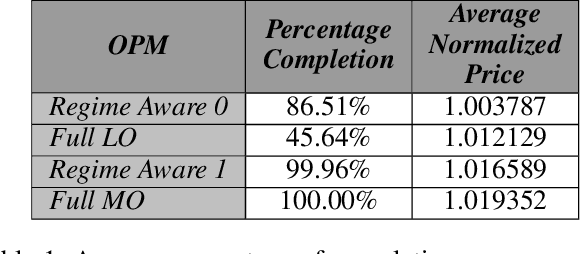

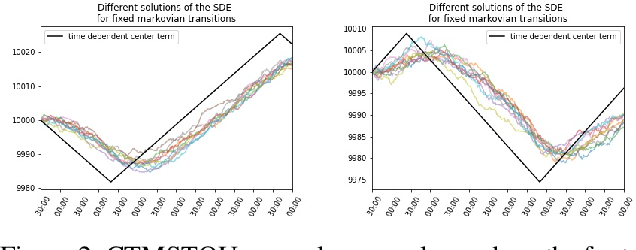

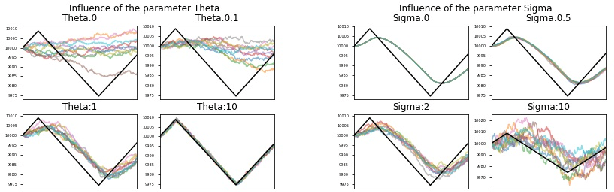

Market regimes is a popular topic in quantitative finance even though there is little consensus on the details of how they should be defined. They arise as a feature both in financial market prediction problems and financial market task performing problems. In this work we use discrete event time multi-agent market simulation to freely experiment in a reproducible and understandable environment where regimes can be explicitly switched and enforced. We introduce a novel stochastic process to model the fundamental value perceived by market participants: Continuous-Time Markov Switching Trending Ornstein-Uhlenbeck (CTMSTOU), which facilitates the study of trading policies in regime switching markets. We define the notion of regime-awareness for a trading agent as well and illustrate its importance through the study of different order placement strategies in the context of order execution problems.