Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA first-order method for nonconvex-strongly-concave constrained minimax optimization

Dec 28, 2025In this paper we study a nonconvex-strongly-concave constrained minimax problem. Specifically, we propose a first-order augmented Lagrangian method for solving it, whose subproblems are nonconvex-strongly-concave unconstrained minimax problems and suitably solved by a first-order method developed in this paper that leverages the strong concavity structure. Under suitable assumptions, the proposed method achieves an \emph{operation complexity} of $O(\varepsilon^{-3.5}\log\varepsilon^{-1})$, measured in terms of its fundamental operations, for finding an $\varepsilon$-KKT solution of the constrained minimax problem, which improves the previous best-known operation complexity by a factor of $\varepsilon^{-0.5}$.

Solving bilevel optimization via sequential minimax optimization

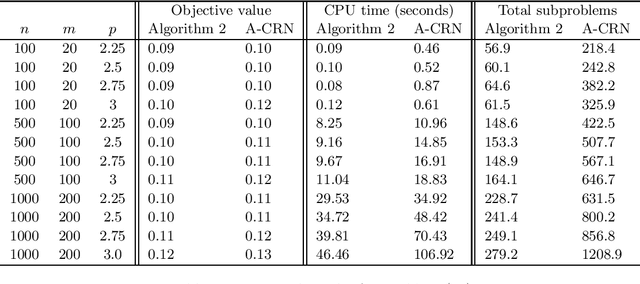

Nov 10, 2025In this paper we propose a sequential minimax optimization (SMO) method for solving a class of constrained bilevel optimization problems in which the lower-level part is a possibly nonsmooth convex optimization problem, while the upper-level part is a possibly nonconvex optimization problem. Specifically, SMO applies a first-order method to solve a sequence of minimax subproblems, which are obtained by employing a hybrid of modified augmented Lagrangian and penalty schemes on the bilevel optimization problems. Under suitable assumptions, we establish an operation complexity of $O(\varepsilon^{-7}\log\varepsilon^{-1})$ and $O(\varepsilon^{-6}\log\varepsilon^{-1})$, measured in terms of fundamental operations, for SMO in finding an $\varepsilon$-KKT solution of the bilevel optimization problems with merely convex and strongly convex lower-level objective functions, respectively. The latter result improves the previous best-known operation complexity by a factor of $\varepsilon^{-1}$. Preliminary numerical results demonstrate significantly superior computational performance compared to the recently developed first-order penalty method.

A first-order method for nonconvex-nonconcave minimax problems under a local Kurdyka-Łojasiewicz condition

Jul 02, 2025We study a class of nonconvex-nonconcave minimax problems in which the inner maximization problem satisfies a local Kurdyka-{\L}ojasiewicz (KL) condition that may vary with the outer minimization variable. In contrast to the global KL or Polyak-{\L}ojasiewicz (PL) conditions commonly assumed in the literature -- which are significantly stronger and often too restrictive in practice -- this local KL condition accommodates a broader range of practical scenarios. However, it also introduces new analytical challenges. In particular, as an optimization algorithm progresses toward a stationary point of the problem, the region over which the KL condition holds may shrink, resulting in a more intricate and potentially ill-conditioned landscape. To address this challenge, we show that the associated maximal function is locally H\"older smooth. Leveraging this key property, we develop an inexact proximal gradient method for solving the minimax problem, where the inexact gradient of the maximal function is computed by applying a proximal gradient method to a KL-structured subproblem. Under mild assumptions, we establish complexity guarantees for computing an approximate stationary point of the minimax problem.

First-order methods for stochastic and finite-sum convex optimization with deterministic constraints

Jun 25, 2025In this paper, we study a class of stochastic and finite-sum convex optimization problems with deterministic constraints. Existing methods typically aim to find an $\epsilon$-$expectedly\ feasible\ stochastic\ optimal$ solution, in which the expected constraint violation and expected optimality gap are both within a prescribed tolerance $\epsilon$. However, in many practical applications, constraints must be nearly satisfied with certainty, rendering such solutions potentially unsuitable due to the risk of substantial violations. To address this issue, we propose stochastic first-order methods for finding an $\epsilon$-$surely\ feasible\ stochastic\ optimal$ ($\epsilon$-SFSO) solution, where the constraint violation is deterministically bounded by $\epsilon$ and the expected optimality gap is at most $\epsilon$. Our methods apply an accelerated stochastic gradient (ASG) scheme or a modified variance-reduced ASG scheme $only\ once$ to a sequence of quadratic penalty subproblems with appropriately chosen penalty parameters. We establish first-order oracle complexity bounds for the proposed methods in computing an $\epsilon$-SFSO solution. As a byproduct, we also derive first-order oracle complexity results for sample average approximation method in computing an $\epsilon$-SFSO solution of the stochastic optimization problem using our proposed methods to solve the sample average problem.

Complexity of normalized stochastic first-order methods with momentum under heavy-tailed noise

Jun 12, 2025

In this paper, we propose practical normalized stochastic first-order methods with Polyak momentum, multi-extrapolated momentum, and recursive momentum for solving unconstrained optimization problems. These methods employ dynamically updated algorithmic parameters and do not require explicit knowledge of problem-dependent quantities such as the Lipschitz constant or noise bound. We establish first-order oracle complexity results for finding approximate stochastic stationary points under heavy-tailed noise and weakly average smoothness conditions -- both of which are weaker than the commonly used bounded variance and mean-squared smoothness assumptions. Our complexity bounds either improve upon or match the best-known results in the literature. Numerical experiments are presented to demonstrate the practical effectiveness of the proposed methods.

Nested Stochastic Gradient Descent for (Generalized) Sinkhorn Distance-Regularized Distributionally Robust Optimization

Mar 29, 2025Distributionally robust optimization (DRO) is a powerful technique to train robust models against data distribution shift. This paper aims to solve regularized nonconvex DRO problems, where the uncertainty set is modeled by a so-called generalized Sinkhorn distance and the loss function is nonconvex and possibly unbounded. Such a distance allows to model uncertainty of distributions with different probability supports and divergence functions. For this class of regularized DRO problems, we derive a novel dual formulation taking the form of nested stochastic programming, where the dual variable depends on the data sample. To solve the dual problem, we provide theoretical evidence to design a nested stochastic gradient descent (SGD) algorithm, which leverages stochastic approximation to estimate the nested stochastic gradients. We study the convergence rate of nested SGD and establish polynomial iteration and sample complexities that are independent of the data size and parameter dimension, indicating its potential for solving large-scale DRO problems. We conduct numerical experiments to demonstrate the efficiency and robustness of the proposed algorithm.

Variance-reduced first-order methods for deterministically constrained stochastic nonconvex optimization with strong convergence guarantees

Sep 17, 2024In this paper, we study a class of deterministically constrained stochastic optimization problems. Existing methods typically aim to find an $\epsilon$-stochastic stationary point, where the expected violations of both constraints and first-order stationarity are within a prescribed accuracy $\epsilon$. However, in many practical applications, it is crucial that the constraints be nearly satisfied with certainty, making such an $\epsilon$-stochastic stationary point potentially undesirable due to the risk of significant constraint violations. To address this issue, we propose single-loop variance-reduced stochastic first-order methods, where the stochastic gradient of the stochastic component is computed using either a truncated recursive momentum scheme or a truncated Polyak momentum scheme for variance reduction, while the gradient of the deterministic component is computed exactly. Under the error bound condition with a parameter $\theta \geq 1$ and other suitable assumptions, we establish that the proposed methods achieve a sample complexity and first-order operation complexity of $\widetilde O(\epsilon^{-\max\{4, 2\theta\}})$ for finding a stronger $\epsilon$-stochastic stationary point, where the constraint violation is within $\epsilon$ with certainty, and the expected violation of first-order stationarity is within $\epsilon$. To the best of our knowledge, this is the first work to develop methods with provable complexity guarantees for finding an approximate stochastic stationary point of such problems that nearly satisfies all constraints with certainty.

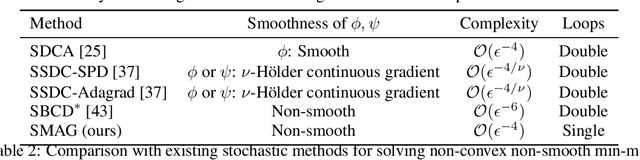

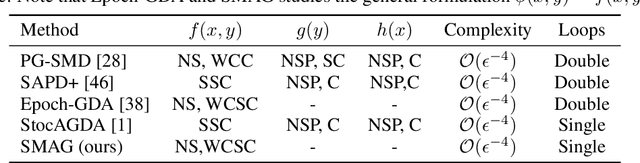

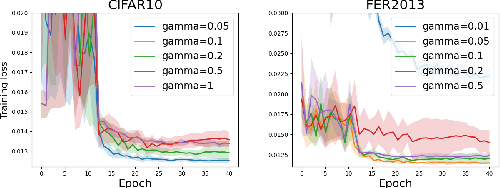

Single-loop Stochastic Algorithms for Difference of Max-Structured Weakly Convex Functions

May 30, 2024

In this paper, we study a class of non-smooth non-convex problems in the form of $\min_{x}[\max_{y\in Y}\phi(x, y) - \max_{z\in Z}\psi(x, z)]$, where both $\Phi(x) = \max_{y\in Y}\phi(x, y)$ and $\Psi(x)=\max_{z\in Z}\psi(x, z)$ are weakly convex functions, and $\phi(x, y), \psi(x, z)$ are strongly concave functions in terms of $y$ and $z$, respectively. It covers two families of problems that have been studied but are missing single-loop stochastic algorithms, i.e., difference of weakly convex functions and weakly convex strongly-concave min-max problems. We propose a stochastic Moreau envelope approximate gradient method dubbed SMAG, the first single-loop algorithm for solving these problems, and provide a state-of-the-art non-asymptotic convergence rate. The key idea of the design is to compute an approximate gradient of the Moreau envelopes of $\Phi, \Psi$ using only one step of stochastic gradient update of the primal and dual variables. Empirically, we conduct experiments on positive-unlabeled (PU) learning and partial area under ROC curve (pAUC) optimization with an adversarial fairness regularizer to validate the effectiveness of our proposed algorithms.

Newton-CG methods for nonconvex unconstrained optimization with Hölder continuous Hessian

Nov 22, 2023

In this paper we consider a nonconvex unconstrained optimization problem minimizing a twice differentiable objective function with H\"older continuous Hessian. Specifically, we first propose a Newton-conjugate gradient (Newton-CG) method for finding an approximate first-order stationary point (FOSP) of this problem, assuming the associated the H\"older parameters are explicitly known. Then we develop a parameter-free Newton-CG method without requiring any prior knowledge of these parameters. To the best of our knowledge, this method is the first parameter-free second-order method achieving the best-known iteration and operation complexity for finding an approximate FOSP of this problem. Furthermore, we propose a Newton-CG method for finding an approximate second-order stationary point (SOSP) of the considered problem with high probability and establish its iteration and operation complexity. Finally, we present preliminary numerical results to demonstrate the superior practical performance of our parameter-free Newton-CG method over a well-known regularized Newton method.

A Newton-CG based barrier-augmented Lagrangian method for general nonconvex conic optimization

Jan 10, 2023In this paper we consider finding an approximate second-order stationary point (SOSP) of general nonconvex conic optimization that minimizes a twice differentiable function subject to nonlinear equality constraints and also a convex conic constraint. In particular, we propose a Newton-conjugate gradient (Newton-CG) based barrier-augmented Lagrangian method for finding an approximate SOSP of this problem. Under some mild assumptions, we show that our method enjoys a total inner iteration complexity of $\widetilde{\cal O}(\epsilon^{-11/2})$ and an operation complexity of $\widetilde{\cal O}(\epsilon^{-11/2}\min\{n,\epsilon^{-5/4}\})$ for finding an $(\epsilon,\sqrt{\epsilon})$-SOSP of general nonconvex conic optimization with high probability. Moreover, under a constraint qualification, these complexity bounds are improved to $\widetilde{\cal O}(\epsilon^{-7/2})$ and $\widetilde{\cal O}(\epsilon^{-7/2}\min\{n,\epsilon^{-3/4}\})$, respectively. To the best of our knowledge, this is the first study on the complexity of finding an approximate SOSP of general nonconvex conic optimization. Preliminary numerical results are presented to demonstrate superiority of the proposed method over first-order methods in terms of solution quality.