Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeUNIC-Adapter: Unified Image-instruction Adapter with Multi-modal Transformer for Image Generation

Dec 25, 2024

Recently, text-to-image generation models have achieved remarkable advancements, particularly with diffusion models facilitating high-quality image synthesis from textual descriptions. However, these models often struggle with achieving precise control over pixel-level layouts, object appearances, and global styles when using text prompts alone. To mitigate this issue, previous works introduce conditional images as auxiliary inputs for image generation, enhancing control but typically necessitating specialized models tailored to different types of reference inputs. In this paper, we explore a new approach to unify controllable generation within a single framework. Specifically, we propose the unified image-instruction adapter (UNIC-Adapter) built on the Multi-Modal-Diffusion Transformer architecture, to enable flexible and controllable generation across diverse conditions without the need for multiple specialized models. Our UNIC-Adapter effectively extracts multi-modal instruction information by incorporating both conditional images and task instructions, injecting this information into the image generation process through a cross-attention mechanism enhanced by Rotary Position Embedding. Experimental results across a variety of tasks, including pixel-level spatial control, subject-driven image generation, and style-image-based image synthesis, demonstrate the effectiveness of our UNIC-Adapter in unified controllable image generation.

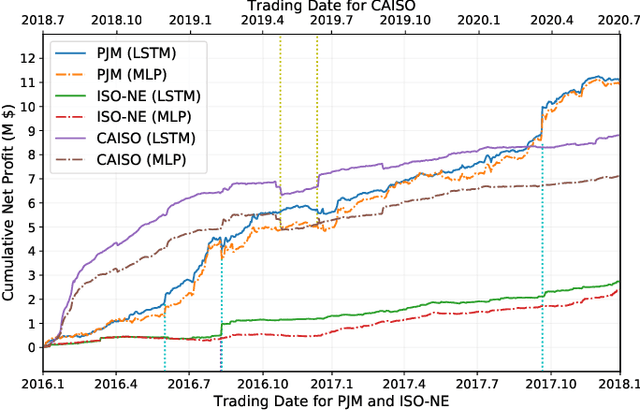

Machine Learning-Driven Virtual Bidding with Electricity Market Efficiency Analysis

Apr 06, 2021

This paper develops a machine learning-driven portfolio optimization framework for virtual bidding in electricity markets considering both risk constraint and price sensitivity. The algorithmic trading strategy is developed from the perspective of a proprietary trading firm to maximize profit. A recurrent neural network-based Locational Marginal Price (LMP) spread forecast model is developed by leveraging the inter-hour dependencies of the market clearing algorithm. The LMP spread sensitivity with respect to net virtual bids is modeled as a monotonic function with the proposed constrained gradient boosting tree. We leverage the proposed algorithmic virtual bid trading strategy to evaluate both the profitability of the virtual bid portfolio and the efficiency of U.S. wholesale electricity markets. The comprehensive empirical analysis on PJM, ISO-NE, and CAISO indicates that the proposed virtual bid portfolio optimization strategy considering the price sensitivity explicitly outperforms the one that neglects the price sensitivity. The Sharpe ratio of virtual bid portfolios for all three electricity markets are much higher than that of the S&P 500 index. It was also shown that the efficiency of CAISO's two-settlement system is lower than that of PJM and ISO-NE.