Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRough Transformers: Lightweight Continuous-Time Sequence Modelling with Path Signatures

May 31, 2024Time-series data in real-world settings typically exhibit long-range dependencies and are observed at non-uniform intervals. In these settings, traditional sequence-based recurrent models struggle. To overcome this, researchers often replace recurrent architectures with Neural ODE-based models to account for irregularly sampled data and use Transformer-based architectures to account for long-range dependencies. Despite the success of these two approaches, both incur very high computational costs for input sequences of even moderate length. To address this challenge, we introduce the Rough Transformer, a variation of the Transformer model that operates on continuous-time representations of input sequences and incurs significantly lower computational costs. In particular, we propose \textit{multi-view signature attention}, which uses path signatures to augment vanilla attention and to capture both local and global (multi-scale) dependencies in the input data, while remaining robust to changes in the sequence length and sampling frequency and yielding improved spatial processing. We find that, on a variety of time-series-related tasks, Rough Transformers consistently outperform their vanilla attention counterparts while obtaining the representational benefits of Neural ODE-based models, all at a fraction of the computational time and memory resources.

Rough Transformers for Continuous and Efficient Time-Series Modelling

Mar 15, 2024Time-series data in real-world medical settings typically exhibit long-range dependencies and are observed at non-uniform intervals. In such contexts, traditional sequence-based recurrent models struggle. To overcome this, researchers replace recurrent architectures with Neural ODE-based models to model irregularly sampled data and use Transformer-based architectures to account for long-range dependencies. Despite the success of these two approaches, both incur very high computational costs for input sequences of moderate lengths and greater. To mitigate this, we introduce the Rough Transformer, a variation of the Transformer model which operates on continuous-time representations of input sequences and incurs significantly reduced computational costs, critical for addressing long-range dependencies common in medical contexts. In particular, we propose multi-view signature attention, which uses path signatures to augment vanilla attention and to capture both local and global dependencies in input data, while remaining robust to changes in the sequence length and sampling frequency. We find that Rough Transformers consistently outperform their vanilla attention counterparts while obtaining the benefits of Neural ODE-based models using a fraction of the computational time and memory resources on synthetic and real-world time-series tasks.

Interpretable Spectral Variational AutoEncoder (ISVAE) for time series clustering

Oct 18, 2023The best encoding is the one that is interpretable in nature. In this work, we introduce a novel model that incorporates an interpretable bottleneck-termed the Filter Bank (FB)-at the outset of a Variational Autoencoder (VAE). This arrangement compels the VAE to attend on the most informative segments of the input signal, fostering the learning of a novel encoding ${f_0}$ which boasts enhanced interpretability and clusterability over traditional latent spaces. By deliberately constraining the VAE with this FB, we intentionally constrict its capacity to access broad input domain information, promoting the development of an encoding that is discernible, separable, and of reduced dimensionality. The evolutionary learning trajectory of ${f_0}$ further manifests as a dynamic hierarchical tree, offering profound insights into cluster similarities. Additionally, for handling intricate data configurations, we propose a tailored decoder structure that is symmetrically aligned with FB's architecture. Empirical evaluations highlight the superior efficacy of ISVAE, which compares favorably to state-of-the-art results in clustering metrics across real-world datasets.

Sleep Activity Recognition and Characterization from Multi-Source Passively Sensed Data

Jan 17, 2023

Sleep constitutes a key indicator of human health, performance, and quality of life. Sleep deprivation has long been related to the onset, development, and worsening of several mental and metabolic disorders, constituting an essential marker for preventing, evaluating, and treating different health conditions. Sleep Activity Recognition methods can provide indicators to assess, monitor, and characterize subjects' sleep-wake cycles and detect behavioral changes. In this work, we propose a general method that continuously operates on passively sensed data from smartphones to characterize sleep and identify significant sleep episodes. Thanks to their ubiquity, these devices constitute an excellent alternative data source to profile subjects' biorhythms in a continuous, objective, and non-invasive manner, in contrast to traditional sleep assessment methods that usually rely on intrusive and subjective procedures. A Heterogeneous Hidden Markov Model is used to model a discrete latent variable process associated with the Sleep Activity Recognition task in a self-supervised way. We validate our results against sleep metrics reported by tested wearables, proving the effectiveness of the proposed approach and advocating its use to assess sleep without more reliable sources.

Heterogeneous Hidden Markov Models for Sleep Activity Recognition from Multi-Source Passively Sensed Data

Nov 08, 2022Psychiatric patients' passive activity monitoring is crucial to detect behavioural shifts in real-time, comprising a tool that helps clinicians supervise patients' evolution over time and enhance the associated treatments' outcomes. Frequently, sleep disturbances and mental health deterioration are closely related, as mental health condition worsening regularly entails shifts in the patients' circadian rhythms. Therefore, Sleep Activity Recognition constitutes a behavioural marker to portray patients' activity cycles and to detect behavioural changes among them. Moreover, mobile passively sensed data captured from smartphones, thanks to these devices' ubiquity, constitute an excellent alternative to profile patients' biorhythm. In this work, we aim to identify major sleep episodes based on passively sensed data. To do so, a Heterogeneous Hidden Markov Model is proposed to model a discrete latent variable process associated with the Sleep Activity Recognition task in a self-supervised way. We validate our results against sleep metrics reported by clinically tested wearables, proving the effectiveness of the proposed approach.

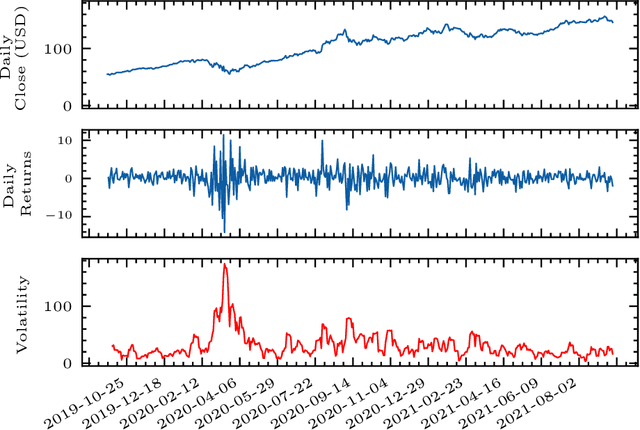

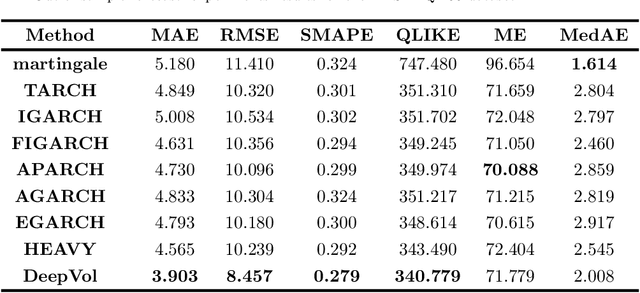

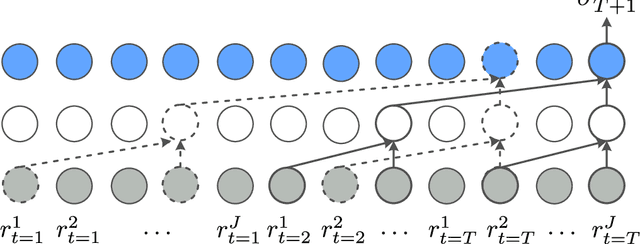

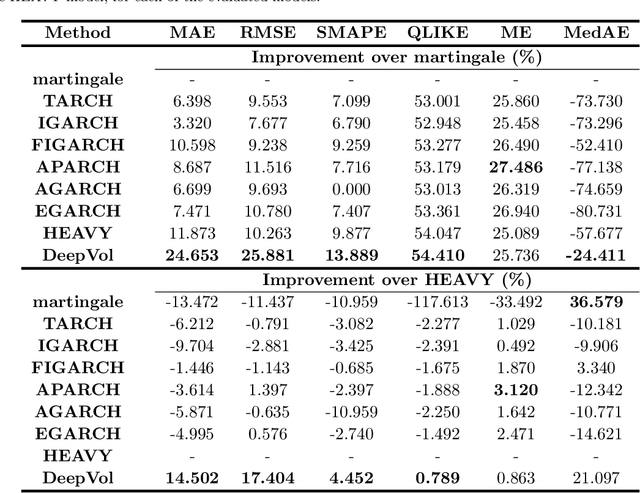

DeepVol: Volatility Forecasting from High-Frequency Data with Dilated Causal Convolutions

Sep 23, 2022

Volatility forecasts play a central role among equity risk measures. Besides traditional statistical models, modern forecasting techniques, based on machine learning, can readily be employed when treating volatility as a univariate, daily time-series. However, econometric studies have shown that increasing the number of daily observations with high-frequency intraday data helps to improve predictions. In this work, we propose DeepVol, a model based on Dilated Causal Convolutions to forecast day-ahead volatility by using high-frequency data. We show that the dilated convolutional filters are ideally suited to extract relevant information from intraday financial data, thereby naturally mimicking (via a data-driven approach) the econometric models which incorporate realised measures of volatility into the forecast. This allows us to take advantage of the abundance of intraday observations, helping us to avoid the limitations of models that use daily data, such as model misspecification or manually designed handcrafted features, whose devise involves optimising the trade-off between accuracy and computational efficiency and makes models prone to lack of adaptation into changing circumstances. In our analysis, we use two years of intraday data from NASDAQ-100 to evaluate DeepVol's performance. The reported empirical results suggest that the proposed deep learning-based approach learns global features from high-frequency data, achieving more accurate predictions than traditional methodologies, yielding to more appropriate risk measures.

PyHHMM: A Python Library for Heterogeneous Hidden Markov Models

Jan 12, 2022We introduce PyHHMM, an object-oriented open-source Python implementation of Heterogeneous-Hidden Markov Models (HHMMs). In addition to HMM's basic core functionalities, such as different initialization algorithms and classical observations models, i.e., continuous and multinoulli, PyHHMM distinctively emphasizes features not supported in similar available frameworks: a heterogeneous observation model, missing data inference, different model order selection criterias, and semi-supervised training. These characteristics result in a feature-rich implementation for researchers working with sequential data. PyHHMM relies on the numpy, scipy, scikit-learn, and seaborn Python packages, and is distributed under the Apache-2.0 License. PyHHMM's source code is publicly available on Github (https://github.com/fmorenopino/HeterogeneousHMM) to facilitate adoptions and future contributions. A detailed documentation (https://pyhhmm.readthedocs.io/en/latest), which covers examples of use and models' theoretical explanation, is available. The package can be installed through the Python Package Index (PyPI), via 'pip install pyhhmm'.

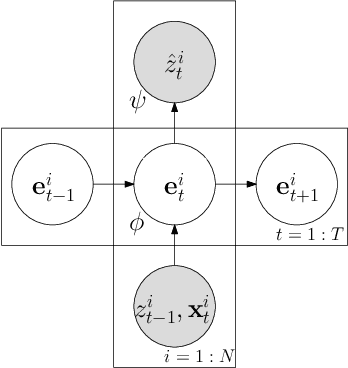

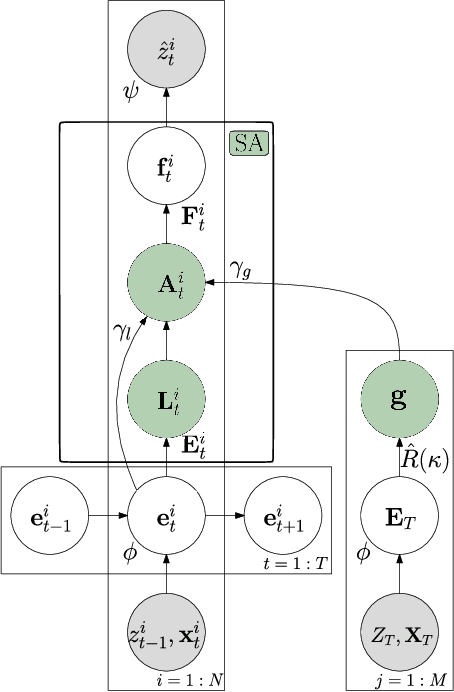

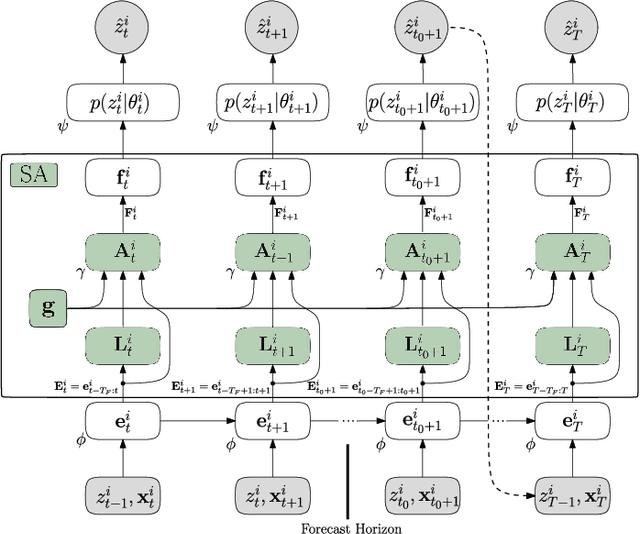

Deep Autoregressive Models with Spectral Attention

Jul 13, 2021

Time series forecasting is an important problem across many domains, playing a crucial role in multiple real-world applications. In this paper, we propose a forecasting architecture that combines deep autoregressive models with a Spectral Attention (SA) module, which merges global and local frequency domain information in the model's embedded space. By characterizing in the spectral domain the embedding of the time series as occurrences of a random process, our method can identify global trends and seasonality patterns. Two spectral attention models, global and local to the time series, integrate this information within the forecast and perform spectral filtering to remove time series's noise. The proposed architecture has a number of useful properties: it can be effectively incorporated into well-know forecast architectures, requiring a low number of parameters and producing interpretable results that improve forecasting accuracy. We test the Spectral Attention Autoregressive Model (SAAM) on several well-know forecast datasets, consistently demonstrating that our model compares favorably to state-of-the-art approaches.