Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMultivariate Time Series Classification with Hierarchical Variational Graph Pooling

Oct 12, 2020

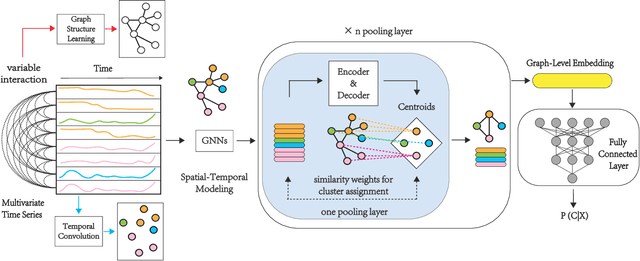

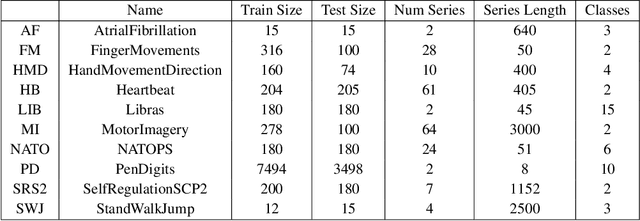

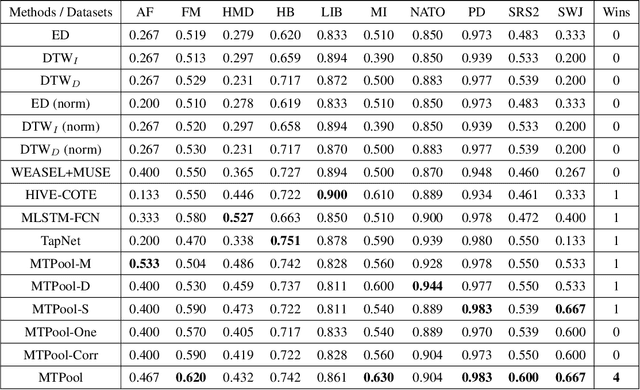

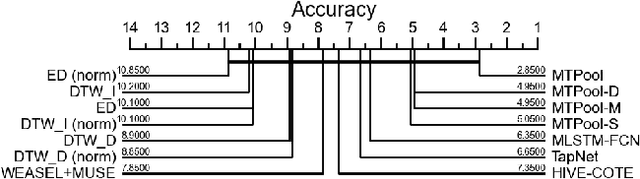

Over the past decade, multivariate time series classification (MTSC) has received great attention with the advance of sensing techniques. Current deep learning methods for MTSC are based on convolutional and recurrent neural network, with the assumption that time series variables have the same effect to each other. Thus they cannot model the pairwise dependencies among variables explicitly. What's more, current spatial-temporal modeling methods based on GNNs are inherently flat and lack the capability of aggregating node information in a hierarchical manner. To address this limitation and attain expressive global representation of MTS, we propose a graph pooling based framework MTPool and view MTSC task as graph classification task. With graph structure learning and temporal convolution, MTS slices are converted to graphs and spatial-temporal features are extracted. Then, we propose a novel graph pooling method, which uses an ``encoder-decoder'' mechanism to generate adaptive centroids for cluster assignments. GNNs and graph pooling layers are used for joint graph representation learning and graph coarsening. With multiple graph pooling layers, the input graphs are hierachically coarsened to one node. Finally, differentiable classifier takes this coarsened one-node graph as input to get the final predicted class. Experiments on 10 benchmark datasets demonstrate MTPool outperforms state-of-the-art methods in MTSC tasks.

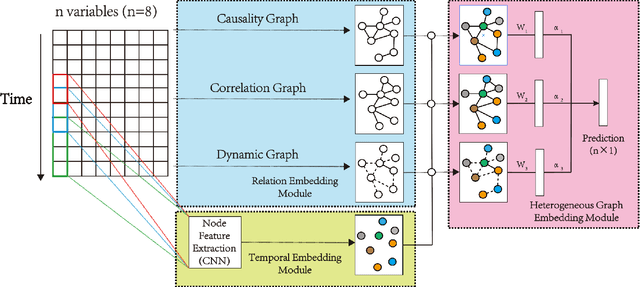

Modeling Complex Spatial Patterns with Temporal Features via Heterogenous Graph Embedding Networks

Sep 11, 2020

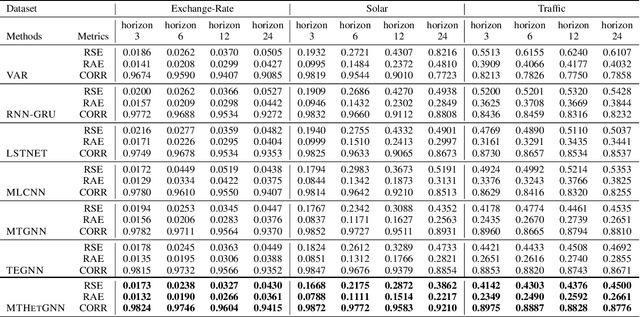

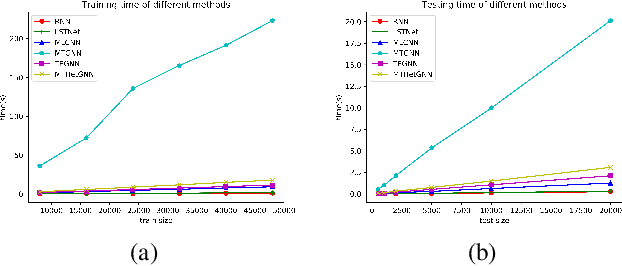

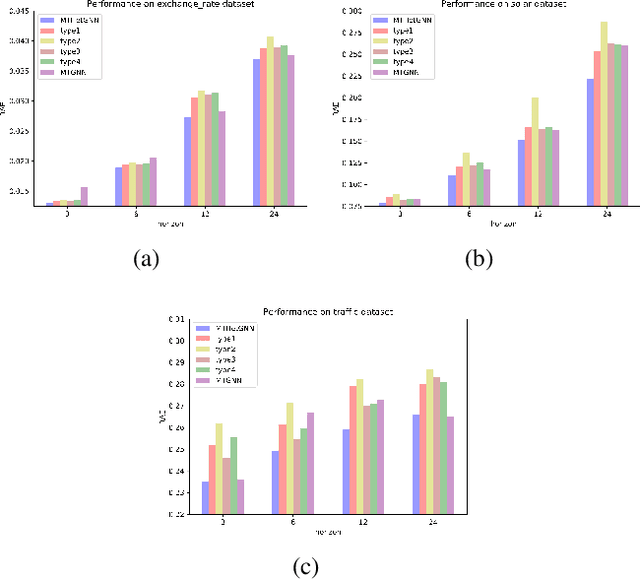

Multivariate time series (MTS) forecasting is an important problem in many fields. Accurate forecasting results can effectively help decision-making. Variables in MTS have rich relations among each other and the value of each variable in MTS depends both on its historical values and on other variables. These rich relations can be static and predictable or dynamic and latent. Existing methods do not incorporate these rich relational information into modeling or only model certain relation among MTS variables. To jointly model rich relations among variables and temporal dependencies within the time series, a novel end-to-end deep learning model, termed Multivariate Time Series Forecasting via Heterogenous Graph Neural Networks (MTHetGNN) is proposed in this paper. To characterize rich relations among variables, a relation embedding module is introduced in our model, where each variable is regarded as a graph node and each type of edge represents a specific relationship among variables or one specific dynamic update strategy to model the latent dependency among variables. In addition, convolutional neural network (CNN) filters with different perception scales are used for time series feature extraction, which is used to generate the feature of each node. Finally, heterogenous graph neural networks are adopted to handle the complex structural information generated by temporal embedding module and relation embedding module. Three benchmark datasets from the real world are used to evaluate the proposed MTHetGNN and the comprehensive experiments show that MTHetGNN achieves state-of-the-art results in MTS forecasting task.

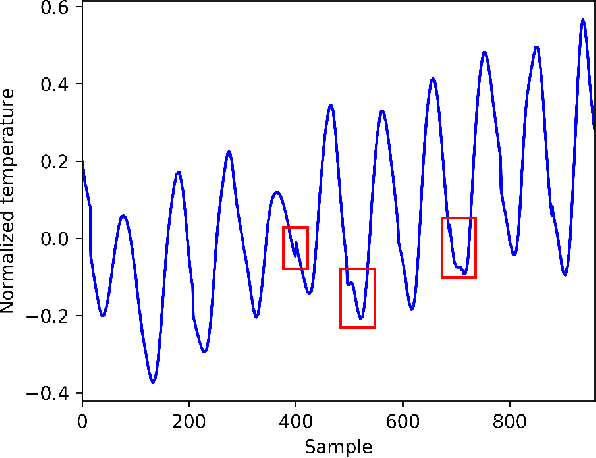

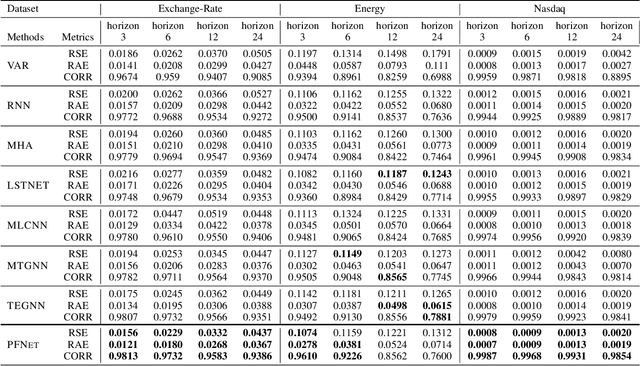

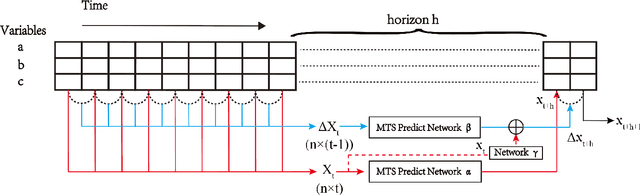

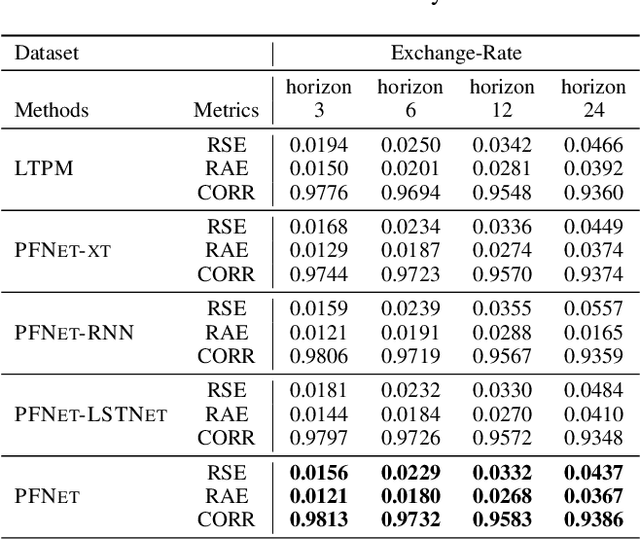

Parallel Extraction of Long-term Trends and Short-term Fluctuation Framework for Multivariate Time Series Forecasting

Sep 07, 2020

Multivariate time series forecasting is widely used in various fields. Reasonable prediction results can assist people in planning and decision-making, generate benefits and avoid risks. Normally, there are two characteristics of time series, that is, long-term trend and short-term fluctuation. For example, stock prices will have a long-term upward trend with the market, but there may be a small decline in the short term. These two characteristics are often relatively independent of each other. However, the existing prediction methods often do not distinguish between them, which reduces the accuracy of the prediction model. In this paper, a MTS forecasting framework that can capture the long-term trends and short-term fluctuations of time series in parallel is proposed. This method uses the original time series and its first difference to characterize long-term trends and short-term fluctuations. Three prediction sub-networks are constructed to predict long-term trends, short-term fluctuations and the final value to be predicted. In the overall optimization goal, the idea of multi-task learning is used for reference, which is to make the prediction results of long-term trends and short-term fluctuations as close to the real values as possible while requiring to approximate the values to be predicted. In this way, the proposed method uses more supervision information and can more accurately capture the changing trend of the time series, thereby improving the forecasting performance.