Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeRisk: An Effective Deep Learning Framework for Credit Risk Prediction over Real-World Financial Data

Aug 07, 2023

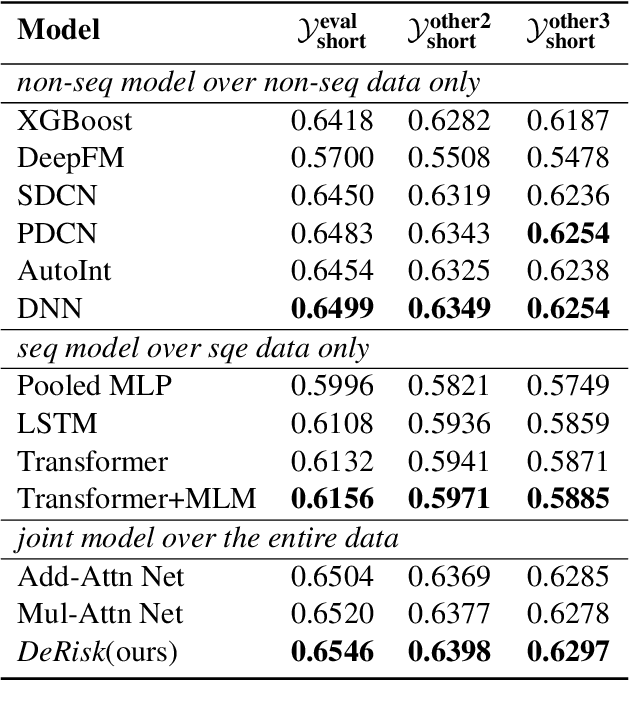

Despite the tremendous advances achieved over the past years by deep learning techniques, the latest risk prediction models for industrial applications still rely on highly handtuned stage-wised statistical learning tools, such as gradient boosting and random forest methods. Different from images or languages, real-world financial data are high-dimensional, sparse, noisy and extremely imbalanced, which makes deep neural network models particularly challenging to train and fragile in practice. In this work, we propose DeRisk, an effective deep learning risk prediction framework for credit risk prediction on real-world financial data. DeRisk is the first deep risk prediction model that outperforms statistical learning approaches deployed in our company's production system. We also perform extensive ablation studies on our method to present the most critical factors for the empirical success of DeRisk.