Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFedAdaVR: Adaptive Variance Reduction for Robust Federated Learning under Limited Client Participation

Jan 29, 2026Federated learning (FL) encounters substantial challenges due to heterogeneity, leading to gradient noise, client drift, and partial client participation errors, the last of which is the most pervasive but remains insufficiently addressed in current literature. In this paper, we propose FedAdaVR, a novel FL algorithm aimed at solving heterogeneity issues caused by sporadic client participation by incorporating an adaptive optimiser with a variance reduction technique. This method takes advantage of the most recent stored updates from clients, even when they are absent from the current training round, thereby emulating their presence. Furthermore, we propose FedAdaVR-Quant, which stores client updates in quantised form, significantly reducing the memory requirements (by 50%, 75%, and 87.5%) of FedAdaVR while maintaining equivalent model performance. We analyse the convergence behaviour of FedAdaVR under general nonconvex conditions and prove that our proposed algorithm can eliminate partial client participation error. Extensive experiments conducted on multiple datasets, under both independent and identically distributed (IID) and non-IID settings, demonstrate that FedAdaVR consistently outperforms state-of-the-art baseline methods.

DSAEval: Evaluating Data Science Agents on a Wide Range of Real-World Data Science Problems

Jan 20, 2026Recent LLM-based data agents aim to automate data science tasks ranging from data analysis to deep learning. However, the open-ended nature of real-world data science problems, which often span multiple taxonomies and lack standard answers, poses a significant challenge for evaluation. To address this, we introduce DSAEval, a benchmark comprising 641 real-world data science problems grounded in 285 diverse datasets, covering both structured and unstructured data (e.g., vision and text). DSAEval incorporates three distinctive features: (1) Multimodal Environment Perception, which enables agents to interpret observations from multiple modalities including text and vision; (2) Multi-Query Interactions, which mirror the iterative and cumulative nature of real-world data science projects; and (3) Multi-Dimensional Evaluation, which provides a holistic assessment across reasoning, code, and results. We systematically evaluate 11 advanced agentic LLMs using DSAEval. Our results show that Claude-Sonnet-4.5 achieves the strongest overall performance, GPT-5.2 is the most efficient, and MiMo-V2-Flash is the most cost-effective. We further demonstrate that multimodal perception consistently improves performance on vision-related tasks, with gains ranging from 2.04% to 11.30%. Overall, while current data science agents perform well on structured data and routine data anlysis workflows, substantial challenges remain in unstructured domains. Finally, we offer critical insights and outline future research directions to advance the development of data science agents.

FedOAED: Federated On-Device Autoencoder Denoiser for Heterogeneous Data under Limited Client Availability

Dec 19, 2025

Over the last few decades, machine learning (ML) and deep learning (DL) solutions have demonstrated their potential across many applications by leveraging large amounts of high-quality data. However, strict data-sharing regulations such as the General Data Protection Regulation (GDPR) and the Health Insurance Portability and Accountability Act (HIPAA) have prevented many data-driven applications from being realised. Federated Learning (FL), in which raw data never leaves local devices, has shown promise in overcoming these limitations. Although FL has grown rapidly in recent years, it still struggles with heterogeneity, which produces gradient noise, client-drift, and increased variance from partial client participation. In this paper, we propose FedOAED, a novel federated learning algorithm designed to mitigate client-drift arising from multiple local training updates and the variance induced by partial client participation. FedOAED incorporates an on-device autoencoder denoiser on the client side to mitigate client-drift and variance resulting from heterogeneous data under limited client availability. Experiments on multiple vision datasets under Non-IID settings demonstrate that FedOAED consistently outperforms state-of-the-art baselines.

TSPRank: Bridging Pairwise and Listwise Methods with a Bilinear Travelling Salesman Model

Nov 18, 2024

Traditional Learning-To-Rank (LETOR) approaches, including pairwise methods like RankNet and LambdaMART, often fall short by solely focusing on pairwise comparisons, leading to sub-optimal global rankings. Conversely, deep learning based listwise methods, while aiming to optimise entire lists, require complex tuning and yield only marginal improvements over robust pairwise models. To overcome these limitations, we introduce Travelling Salesman Problem Rank (TSPRank), a hybrid pairwise-listwise ranking method. TSPRank reframes the ranking problem as a Travelling Salesman Problem (TSP), a well-known combinatorial optimisation challenge that has been extensively studied for its numerous solution algorithms and applications. This approach enables the modelling of pairwise relationships and leverages combinatorial optimisation to determine the listwise ranking. This approach can be directly integrated as an additional component into embeddings generated by existing backbone models to enhance ranking performance. Our extensive experiments across three backbone models on diverse tasks, including stock ranking, information retrieval, and historical events ordering, demonstrate that TSPRank significantly outperforms both pure pairwise and listwise methods. Our qualitative analysis reveals that TSPRank's main advantage over existing methods is its ability to harness global information better while ranking. TSPRank's robustness and superior performance across different domains highlight its potential as a versatile and effective LETOR solution. The code and preprocessed data are available at https://github.com/waylonli/TSPRank-KDD2025.

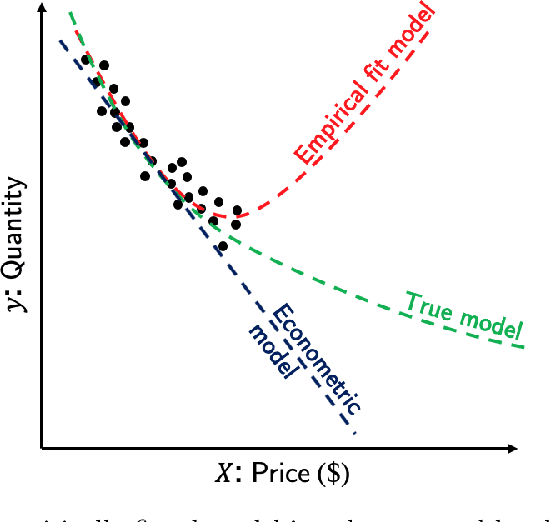

Discrete Choice Analysis with Machine Learning Capabilities

Jan 21, 2021

This paper discusses capabilities that are essential to models applied in policy analysis settings and the limitations of direct applications of off-the-shelf machine learning methodologies to such settings. Traditional econometric methodologies for building discrete choice models for policy analysis involve combining data with modeling assumptions guided by subject-matter considerations. Such considerations are typically most useful in specifying the systematic component of random utility discrete choice models but are typically of limited aid in determining the form of the random component. We identify an area where machine learning paradigms can be leveraged, namely in specifying and systematically selecting the best specification of the random component of the utility equations. We review two recent novel applications where mixed-integer optimization and cross-validation are used to algorithmically select optimal specifications for the random utility components of nested logit and logit mixture models subject to interpretability constraints.

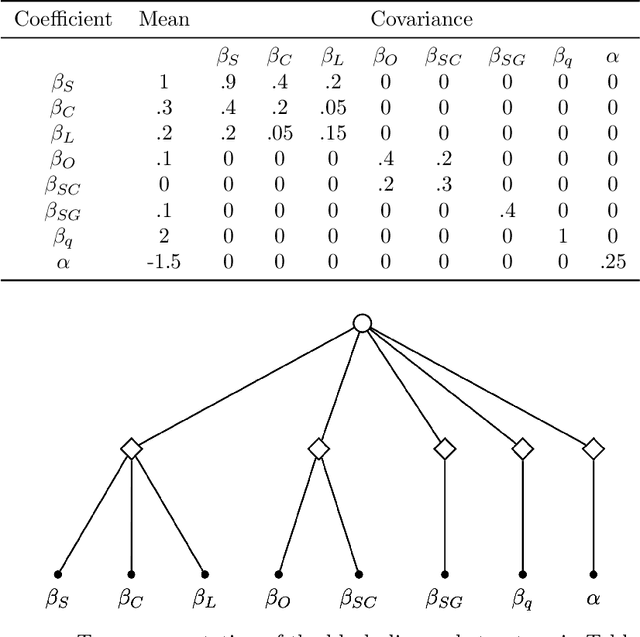

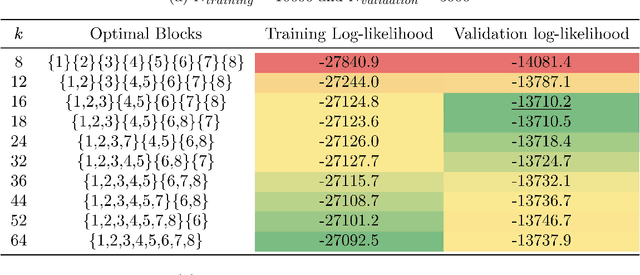

Sparse Covariance Estimation in Logit Mixture Models

Jan 14, 2020

This paper introduces a new data-driven methodology for estimating sparse covariance matrices of the random coefficients in logit mixture models. Researchers typically specify covariance matrices in logit mixture models under one of two extreme assumptions: either an unrestricted full covariance matrix (allowing correlations between all random coefficients), or a restricted diagonal matrix (allowing no correlations at all). Our objective is to find optimal subsets of correlated coefficients for which we estimate covariances. We propose a new estimator, called MISC, that uses a mixed-integer optimization (MIO) program to find an optimal block diagonal structure specification for the covariance matrix, corresponding to subsets of correlated coefficients, for any desired sparsity level using Markov Chain Monte Carlo (MCMC) posterior draws from the unrestricted full covariance matrix. The optimal sparsity level of the covariance matrix is determined using out-of-sample validation. We demonstrate the ability of MISC to correctly recover the true covariance structure from synthetic data. In an empirical illustration using a stated preference survey on modes of transportation, we use MISC to obtain a sparse covariance matrix indicating how preferences for attributes are related to one another.