Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdversaRiskQA: An Adversarial Factuality Benchmark for High-Risk Domains

Jan 21, 2026Hallucination in large language models (LLMs) remains an acute concern, contributing to the spread of misinformation and diminished public trust, particularly in high-risk domains. Among hallucination types, factuality is crucial, as it concerns a model's alignment with established world knowledge. Adversarial factuality, defined as the deliberate insertion of misinformation into prompts with varying levels of expressed confidence, tests a model's ability to detect and resist confidently framed falsehoods. Existing work lacks high-quality, domain-specific resources for assessing model robustness under such adversarial conditions, and no prior research has examined the impact of injected misinformation on long-form text factuality. To address this gap, we introduce AdversaRiskQA, the first verified and reliable benchmark systematically evaluating adversarial factuality across Health, Finance, and Law. The benchmark includes two difficulty levels to test LLMs' defensive capabilities across varying knowledge depths. We propose two automated methods for evaluating the adversarial attack success and long-form factuality. We evaluate six open- and closed-source LLMs from the Qwen, GPT-OSS, and GPT families, measuring misinformation detection rates. Long-form factuality is assessed on Qwen3 (30B) under both baseline and adversarial conditions. Results show that after excluding meaningless responses, Qwen3 (80B) achieves the highest average accuracy, while GPT-5 maintains consistently high accuracy. Performance scales non-linearly with model size, varies by domains, and gaps between difficulty levels narrow as models grow. Long-form evaluation reveals no significant correlation between injected misinformation and the model's factual output. AdversaRiskQA provides a valuable benchmark for pinpointing LLM weaknesses and developing more reliable models for high-stakes applications.

Mitigating Social Desirability Bias in Random Silicon Sampling

Dec 27, 2025Large Language Models (LLMs) are increasingly used to simulate population responses, a method known as ``Silicon Sampling''. However, responses to socially sensitive questions frequently exhibit Social Desirability Bias (SDB), diverging from real human data toward socially acceptable answers. Existing studies on social desirability bias in LLM-based sampling remain limited. In this work, we investigate whether minimal, psychologically grounded prompt wording can mitigate this bias and improve alignment between silicon and human samples. We conducted a study using data from the American National Election Study (ANES) on three LLMs from two model families: the open-source Llama-3.1 series and GPT-4.1-mini. We first replicate a baseline silicon sampling study, confirming the persistent Social Desirability Bias. We then test four prompt-based mitigation methods: \emph{reformulated} (neutral, third-person phrasing), \emph{reverse-coded} (semantic inversion), and two meta-instructions, \emph{priming} and \emph{preamble}, respectively encouraging analytics and sincerity. Alignment with ANES is evaluated using Jensen-Shannon Divergence with bootstrap confidence intervals. Our results demonstrate that reformulated prompts most effectively improve alignment by reducing distribution concentration on socially acceptable answers and achieving distributions closer to ANES. Reverse-coding produced mixed results across eligible items, while the Priming and Preamble encouraged response uniformity and showed no systematic benefit for bias mitigation. Our findings validate the efficacy of prompt-based framing controls in mitigating inherent Social Desirability Bias in LLMs, providing a practical path toward more representative silicon samples.

Beyond Natural Language Plans: Structure-Aware Planning for Query-Focused Table Summarization

Jul 30, 2025Query-focused table summarization requires complex reasoning, often approached through step-by-step natural language (NL) plans. However, NL plans are inherently ambiguous and lack structure, limiting their conversion into executable programs like SQL and hindering scalability, especially for multi-table tasks. To address this, we propose a paradigm shift to structured representations. We introduce a new structured plan, TaSoF, inspired by formalism in traditional multi-agent systems, and a framework, SPaGe, that formalizes the reasoning process in three phases: 1) Structured Planning to generate TaSoF from a query, 2) Graph-based Execution to convert plan steps into SQL and model dependencies via a directed cyclic graph for parallel execution, and 3) Summary Generation to produce query-focused summaries. Our method explicitly captures complex dependencies and improves reliability. Experiments on three public benchmarks show that SPaGe consistently outperforms prior models in both single- and multi-table settings, demonstrating the advantages of structured representations for robust and scalable summarization.

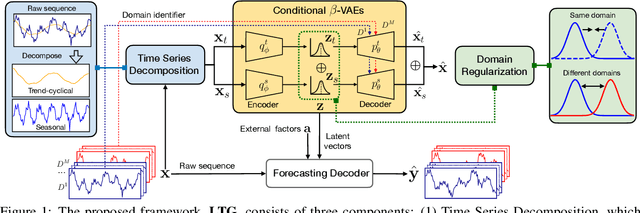

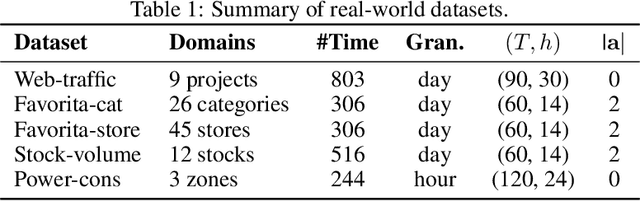

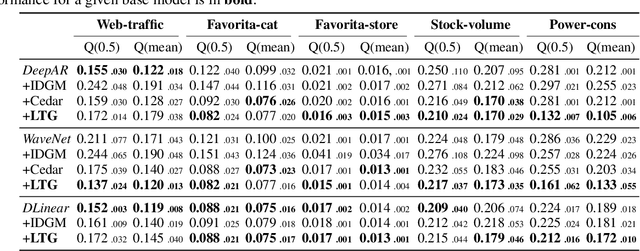

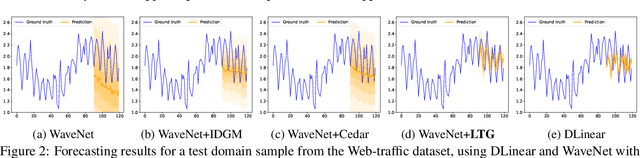

Learning Latent Spaces for Domain Generalization in Time Series Forecasting

Dec 15, 2024

Time series forecasting is vital in many real-world applications, yet developing models that generalize well on unseen relevant domains -- such as forecasting web traffic data on new platforms/websites or estimating e-commerce demand in new regions -- remains underexplored. Existing forecasting models often struggle with domain shifts in time series data, as the temporal patterns involve complex components like trends, seasonality, etc. While some prior work addresses this by matching feature distributions across domains or disentangling domain-shared features using label information, they fail to reveal insights into the latent temporal dependencies, which are critical for identifying common patterns across domains and achieving generalization. We propose a framework for domain generalization in time series forecasting by mining the latent factors that govern temporal dependencies across domains. Our approach uses a decomposition-based architecture with a new Conditional $\beta$-Variational Autoencoder (VAE), wherein time series data is first decomposed into trend-cyclical and seasonal components, each modeled independently through separate $\beta$-VAE modules. The $\beta$-VAE aims to capture disentangled latent factors that control temporal dependencies across domains. We enhance the learning of domain-specific information with a decoder-conditional design and introduce domain regularization to improve the separation of domain-shared and domain-specific latent factors. Our proposed method is flexible and can be applied to various time series forecasting models, enabling effective domain generalization with simplicity and efficiency. We validate its effectiveness on five real-world time series datasets, covering web traffic, e-commerce, finance and power consumption, demonstrating improved generalization performance over state-of-the-art methods.

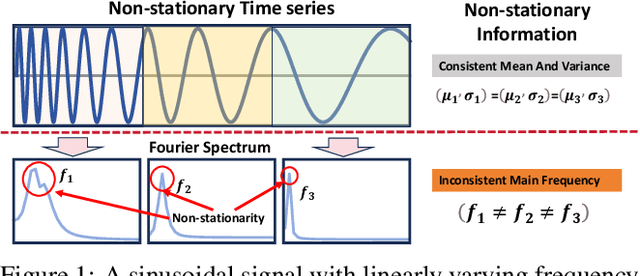

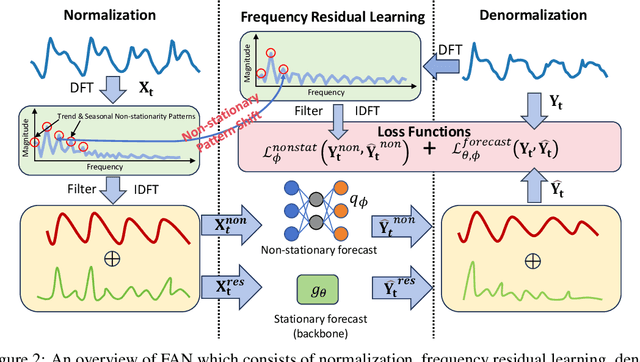

Frequency Adaptive Normalization For Non-stationary Time Series Forecasting

Sep 30, 2024

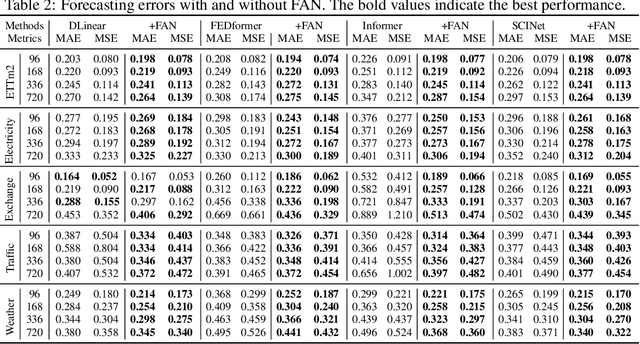

Time series forecasting typically needs to address non-stationary data with evolving trend and seasonal patterns. To address the non-stationarity, reversible instance normalization has been recently proposed to alleviate impacts from the trend with certain statistical measures, e.g., mean and variance. Although they demonstrate improved predictive accuracy, they are limited to expressing basic trends and are incapable of handling seasonal patterns. To address this limitation, this paper proposes a new instance normalization solution, called frequency adaptive normalization (FAN), which extends instance normalization in handling both dynamic trend and seasonal patterns. Specifically, we employ the Fourier transform to identify instance-wise predominant frequent components that cover most non-stationary factors. Furthermore, the discrepancy of those frequency components between inputs and outputs is explicitly modeled as a prediction task with a simple MLP model. FAN is a model-agnostic method that can be applied to arbitrary predictive backbones. We instantiate FAN on four widely used forecasting models as the backbone and evaluate their prediction performance improvements on eight benchmark datasets. FAN demonstrates significant performance advancement, achieving 7.76% ~ 37.90% average improvements in MSE.

A Survey on Societal Event Forecasting with Deep Learning

Dec 12, 2021

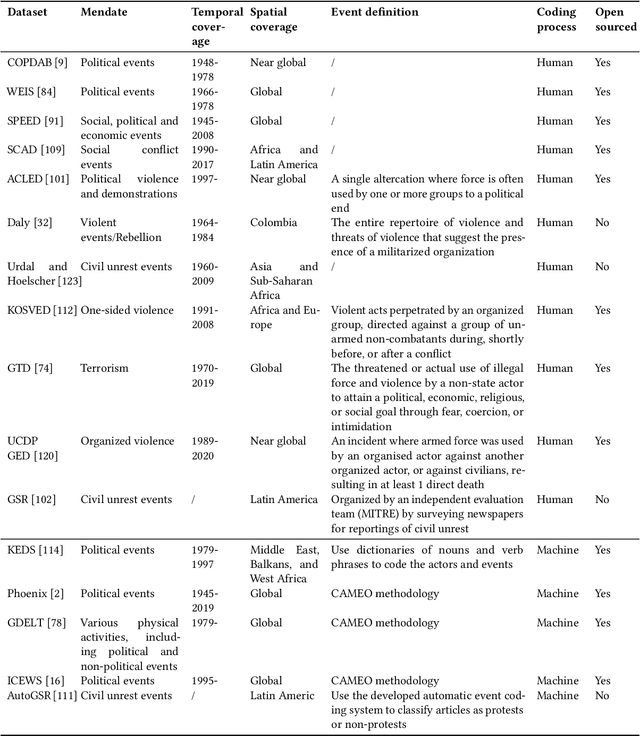

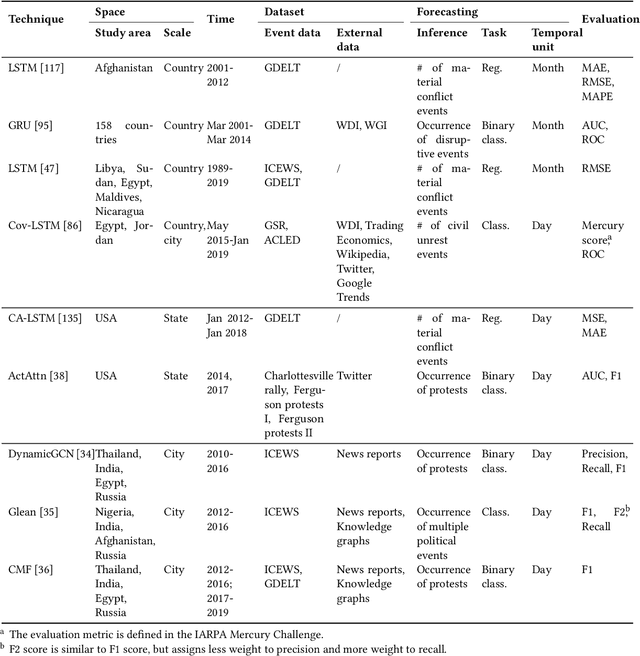

Population-level societal events, such as civil unrest and crime, often have a significant impact on our daily life. Forecasting such events is of great importance for decision-making and resource allocation. Event prediction has traditionally been challenging due to the lack of knowledge regarding the true causes and underlying mechanisms of event occurrence. In recent years, research on event forecasting has made significant progress due to two main reasons: (1) the development of machine learning and deep learning algorithms and (2) the accessibility of public data such as social media, news sources, blogs, economic indicators, and other meta-data sources. The explosive growth of data and the remarkable advancement in software/hardware technologies have led to applications of deep learning techniques in societal event studies. This paper is dedicated to providing a systematic and comprehensive overview of deep learning technologies for societal event predictions. We focus on two domains of societal events: \textit{civil unrest} and \textit{crime}. We first introduce how event forecasting problems are formulated as a machine learning prediction task. Then, we summarize data resources, traditional methods, and recent development of deep learning models for these problems. Finally, we discuss the challenges in societal event forecasting and put forward some promising directions for future research.

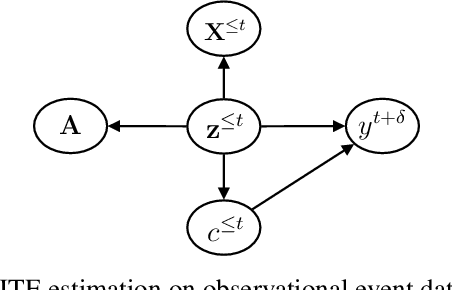

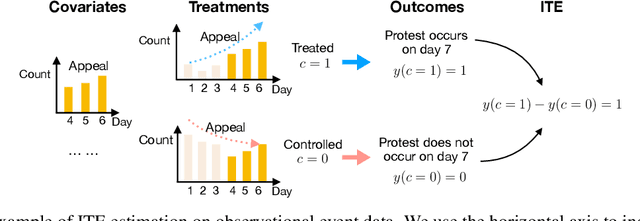

Causal Knowledge Guided Societal Event Forecasting

Dec 10, 2021

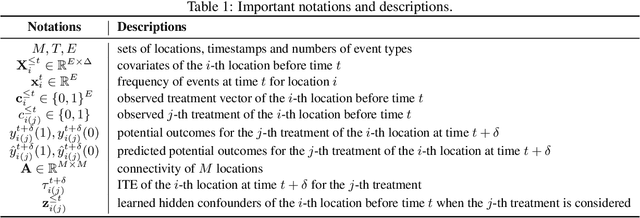

Data-driven societal event forecasting methods exploit relevant historical information to predict future events. These methods rely on historical labeled data and cannot accurately predict events when data are limited or of poor quality. Studying causal effects between events goes beyond correlation analysis and can contribute to a more robust prediction of events. However, incorporating causality analysis in data-driven event forecasting is challenging due to several factors: (i) Events occur in a complex and dynamic social environment. Many unobserved variables, i.e., hidden confounders, affect both potential causes and outcomes. (ii) Given spatiotemporal non-independent and identically distributed (non-IID) data, modeling hidden confounders for accurate causal effect estimation is not trivial. In this work, we introduce a deep learning framework that integrates causal effect estimation into event forecasting. We first study the problem of Individual Treatment Effect (ITE) estimation from observational event data with spatiotemporal attributes and present a novel causal inference model to estimate ITEs. We then incorporate the learned event-related causal information into event prediction as prior knowledge. Two robust learning modules, including a feature reweighting module and an approximate constraint loss, are introduced to enable prior knowledge injection. We evaluate the proposed causal inference model on real-world event datasets and validate the effectiveness of proposed robust learning modules in event prediction by feeding learned causal information into different deep learning methods. Experimental results demonstrate the strengths of the proposed causal inference model for ITE estimation in societal events and showcase the beneficial properties of robust learning modules in societal event forecasting.

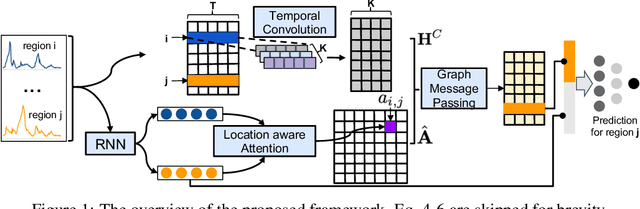

Graph Message Passing with Cross-location Attentions for Long-term ILI Prediction

Dec 29, 2019

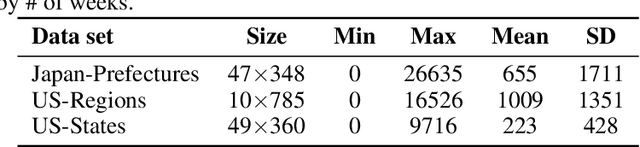

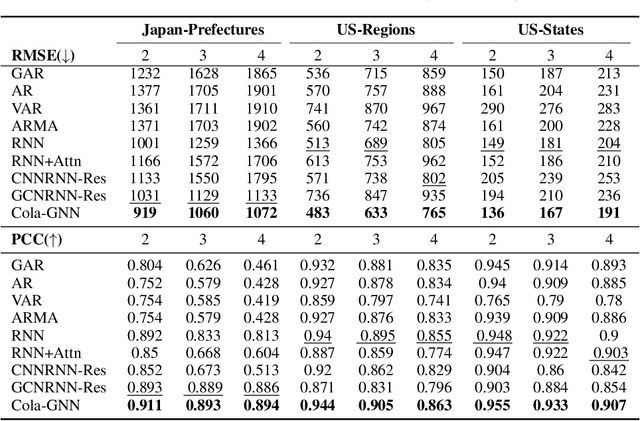

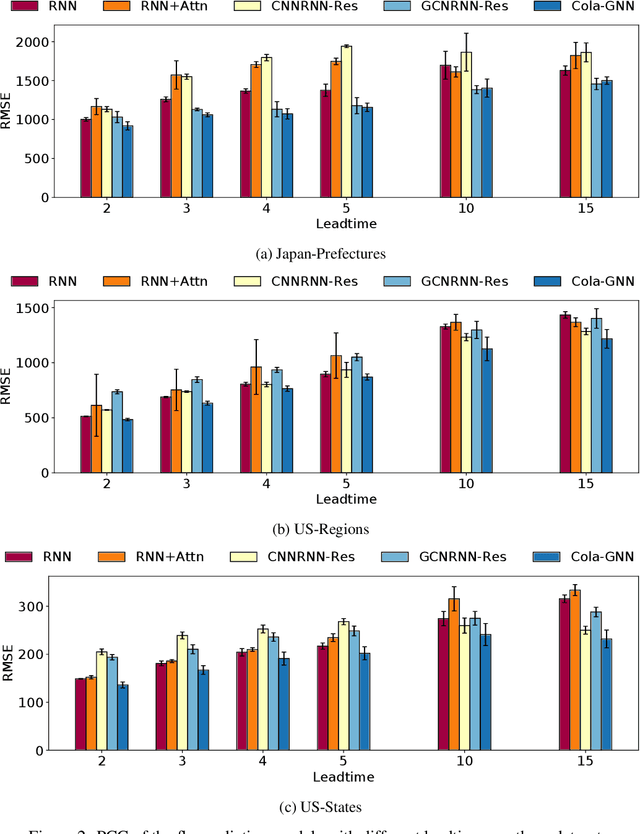

Forecasting influenza-like illness (ILI) is of prime importance to epidemiologists and health-care providers. Early prediction of epidemic outbreaks plays a pivotal role in disease intervention and control. Most existing work has either limited long-term prediction performance or lacks a comprehensive ability to capture spatio-temporal dependencies in data. Accurate and early disease forecasting models would markedly improve both epidemic prevention and managing the onset of an epidemic. In this paper, we design a cross-location attention based graph neural network (Cola-GNN) for learning time series embeddings and location aware attentions. We propose a graph message passing framework to combine learned feature embeddings and an attention matrix to model disease propagation over time. We compare the proposed method with state-of-the-art statistical approaches and deep learning models on real-world epidemic-related datasets from United States and Japan. The proposed method shows strong predictive performance and leads to interpretable results for long-term epidemic predictions.