Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConditional Generators for Limit Order Book Environments: Explainability, Challenges, and Robustness

Jun 22, 2023Limit order books are a fundamental and widespread market mechanism. This paper investigates the use of conditional generative models for order book simulation. For developing a trading agent, this approach has drawn recent attention as an alternative to traditional backtesting due to its ability to react to the presence of the trading agent. Using a state-of-the-art CGAN (from Coletta et al. (2022)), we explore its dependence upon input features, which highlights both strengths and weaknesses. To do this, we use "adversarial attacks" on the model's features and its mechanism. We then show how these insights can be used to improve the CGAN, both in terms of its realism and robustness. We finish by laying out a roadmap for future work.

Model-based gym environments for limit order book trading

Sep 16, 2022

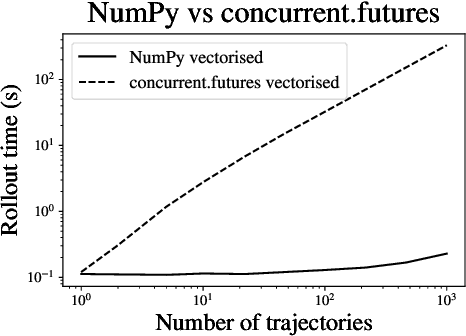

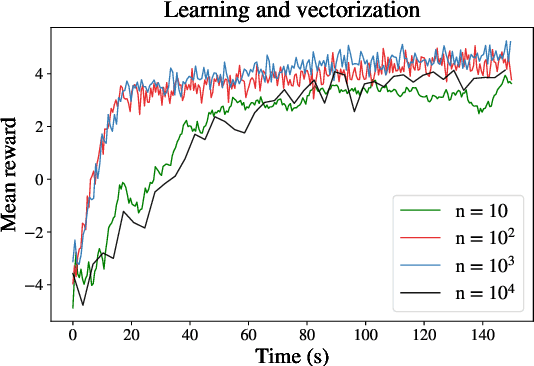

Within the mathematical finance literature there is a rich catalogue of mathematical models for studying algorithmic trading problems -- such as market-making and optimal execution -- in limit order books. This paper introduces \mbtgym, a Python module that provides a suite of gym environments for training reinforcement learning (RL) agents to solve such model-based trading problems. The module is set up in an extensible way to allow the combination of different aspects of different models. It supports highly efficient implementations of vectorized environments to allow faster training of RL agents. In this paper, we motivate the challenge of using RL to solve such model-based limit order book problems in mathematical finance, we explain the design of our gym environment, and then demonstrate its use in solving standard and non-standard problems from the literature. Finally, we lay out a roadmap for further development of our module, which we provide as an open source repository on GitHub so that it can serve as a focal point for RL research in model-based algorithmic trading.

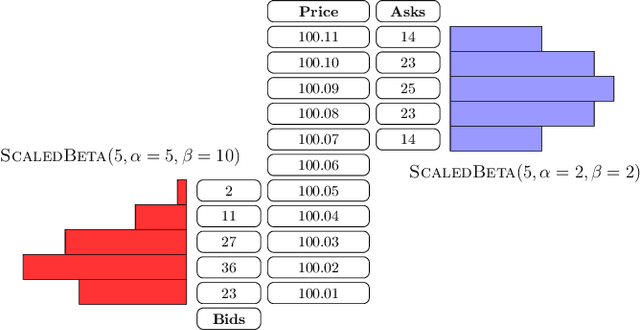

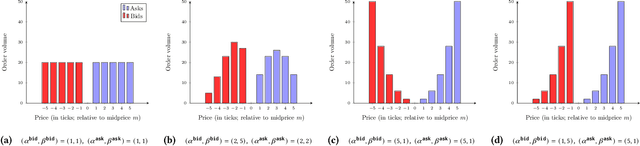

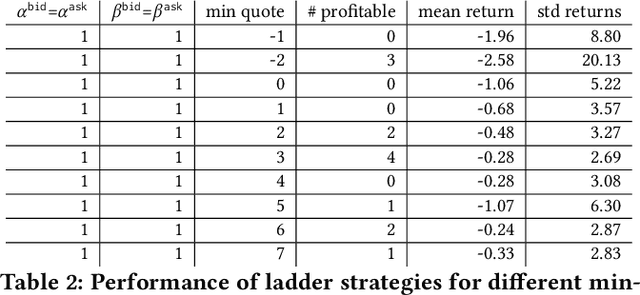

Market Making with Scaled Beta Policies

Jul 09, 2022

This paper introduces a new representation for the actions of a market maker in an order-driven market. This representation uses scaled beta distributions, and generalises three approaches taken in the artificial intelligence for market making literature: single price-level selection, ladder strategies and "market making at the touch". Ladder strategies place uniform volume across an interval of contiguous prices. Scaled beta distribution based policies generalise these, allowing volume to be skewed across the price interval. We demonstrate that this flexibility is useful for inventory management, one of the key challenges faced by a market maker. In this paper, we conduct three main experiments: first, we compare our more flexible beta-based actions with the special case of ladder strategies; then, we investigate the performance of simple fixed distributions; and finally, we devise and evaluate a simple and intuitive dynamic control policy that adjusts actions in a continuous manner depending on the signed inventory that the market maker has acquired. All empirical evaluations use a high-fidelity limit order book simulator based on historical data with 50 levels on each side.