Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeImplicit Language Models are RNNs: Balancing Parallelization and Expressivity

Feb 10, 2025State-space models (SSMs) and transformers dominate the language modeling landscape. However, they are constrained to a lower computational complexity than classical recurrent neural networks (RNNs), limiting their expressivity. In contrast, RNNs lack parallelization during training, raising fundamental questions about the trade off between parallelization and expressivity. We propose implicit SSMs, which iterate a transformation until convergence to a fixed point. Theoretically, we show that implicit SSMs implement the non-linear state-transitions of RNNs. Empirically, we find that only approximate fixed-point convergence suffices, enabling the design of a scalable training curriculum that largely retains parallelization, with full convergence required only for a small subset of tokens. Our approach demonstrates superior state-tracking capabilities on regular languages, surpassing transformers and SSMs. We further scale implicit SSMs to natural language reasoning tasks and pretraining of large-scale language models up to 1.3B parameters on 207B tokens - representing, to our knowledge, the largest implicit model trained to date. Notably, our implicit models outperform their explicit counterparts on standard benchmarks.

Geometry-Aware Instrumental Variable Regression

May 19, 2024Instrumental variable (IV) regression can be approached through its formulation in terms of conditional moment restrictions (CMR). Building on variants of the generalized method of moments, most CMR estimators are implicitly based on approximating the population data distribution via reweightings of the empirical sample. While for large sample sizes, in the independent identically distributed (IID) setting, reweightings can provide sufficient flexibility, they might fail to capture the relevant information in presence of corrupted data or data prone to adversarial attacks. To address these shortcomings, we propose the Sinkhorn Method of Moments, an optimal transport-based IV estimator that takes into account the geometry of the data manifold through data-derivative information. We provide a simple plug-and-play implementation of our method that performs on par with related estimators in standard settings but improves robustness against data corruption and adversarial attacks.

Estimation Beyond Data Reweighting: Kernel Method of Moments

May 18, 2023Moment restrictions and their conditional counterparts emerge in many areas of machine learning and statistics ranging from causal inference to reinforcement learning. Estimators for these tasks, generally called methods of moments, include the prominent generalized method of moments (GMM) which has recently gained attention in causal inference. GMM is a special case of the broader family of empirical likelihood estimators which are based on approximating a population distribution by means of minimizing a $\varphi$-divergence to an empirical distribution. However, the use of $\varphi$-divergences effectively limits the candidate distributions to reweightings of the data samples. We lift this long-standing limitation and provide a method of moments that goes beyond data reweighting. This is achieved by defining an empirical likelihood estimator based on maximum mean discrepancy which we term the kernel method of moments (KMM). We provide a variant of our estimator for conditional moment restrictions and show that it is asymptotically first-order optimal for such problems. Finally, we show that our method achieves competitive performance on several conditional moment restriction tasks.

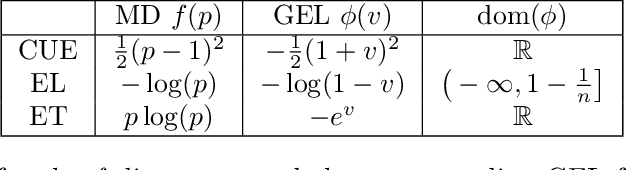

Functional Generalized Empirical Likelihood Estimation for Conditional Moment Restrictions

Jul 11, 2022

Important problems in causal inference, economics, and, more generally, robust machine learning can be expressed as conditional moment restrictions, but estimation becomes challenging as it requires solving a continuum of unconditional moment restrictions. Previous works addressed this problem by extending the generalized method of moments (GMM) to continuum moment restrictions. In contrast, generalized empirical likelihood (GEL) provides a more general framework and has been shown to enjoy favorable small-sample properties compared to GMM-based estimators. To benefit from recent developments in machine learning, we provide a functional reformulation of GEL in which arbitrary models can be leveraged. Motivated by a dual formulation of the resulting infinite dimensional optimization problem, we devise a practical method and explore its asymptotic properties. Finally, we provide kernel- and neural network-based implementations of the estimator, which achieve state-of-the-art empirical performance on two conditional moment restriction problems.